Markets

With Japanese and US markets closed, Europe stood on its own to look for direction after Friday’s yield decline in the wake of weaker than expected US payrolls and services ISM. US markets again considering two potential Fed rate cuts (Sept +/- 90% discounted, 2nd in December +/- 80% discounted) gives European investors some additional comfort on an early ECB rate cut (June almost fully discounted). Economic data were few. Still, a material upward revision of the French (services) PMI also filtered through into the EMU measure (EMU composite PMI upwardly revised from 51.4 to 51.7, best level in almost a year). Aside from better activity, the survey also signaled stronger inflationary pressures in April than in March, with both increases in input costs and output charges quickening and printing above historical series averages. However, with both headline and core EMU inflation in April having declined to the mid 2% area, this probably won’t prevent the ECB withdrawing some policy tightening before summer. This analysis of growing confidence of inflation moving toward 2% was confirmed by press comments of ECB Chief economist Lane this weekend. German yields are easing between 2.1 bps (2-y) and 3.7 bps (10-y). The German 2-y yield is testing intermediate support near 2.90%. The 10-y yield in last week’s move dropped back below the 2.50% barrier. US yields initially build on Friday’s easing momentum but declines are currently limited between 1-2 bps. The prospect/hope of some global central bank easing sooner or later this year, continues to provide some support for global equities. The EuroStoxx50 gains 0.6%. The S&P500 opens 0.35% stronger. Fed Powell’s rather soft assessment and Friday’s weaker data also discouraged dollar USD bulls. DXY struggles not to fall below the 105 barrier. EUR/USD remains well bid (1.0775) with first resistance at 1.0807 (38% retracement end-December/mid-April) within reach. USD/JPY is the exception to the rule with the pair rebounding north to currently trade in the 153.70 area. Even if the Fed were to start some gradually easing later this year, the interest rate gap between the Fed and the BOJ remains too wide to provide any lasting support the Japanese currency. The cat-and-mouse game of (verbal and/or real) interventions between Japanese officials and the market probably is far from over if the BOJ stays silent on the timing of further/protracted policy normalization. Later today, markets will keep an eye at the Fed’s Senior loan Officer Opinion Survey on bank lending. The report fur sure will contain some interesting features on how policy tightening has filtered through into the US economy, but it seldom had lasting market impact.

News & Views

The European Commission in a statement today announced to end a 6-year dispute with Poland over backsliding on democratic principles and the rule of law under the previous PiS government that came to power in 2015. EC president Von der Leyen said that the so-called Article 7 procedure can be closed following a plan that the pro-EU prime minister Tusk in February had presented. The plan back then also triggered the release of several billions locked-up cohesion funds. And last month the EU paid out the first instalment of EU recovery funds to Poland (€6.3bn), making today’s decision largely a formal one. The Polish zloty did frontrun the European-Polish détente a long time ago (since Tusk’s electoral victory), leading to a stoic response on the news today. EUR/PLN eases a few ticks towards 4.32.

John Swinney is poised to become Scotland’s first minister this week after being appointed leader of the Scottish National Party. Swinney’s predecessor Yousaf announced his resignation end of last month ahead of a no confidence vote he was about to lose. It was also week after collapsing the coalition with the Scottish Greens as Yousaf sought to move Scottish political needle from left to center again and face off a rising challenge from Scottish Labour in the upcoming general elections. Swinney is a veteran who led the party in the early 2000s and will face a vote in parliament as early as Tuesday. The SNP holds 63 seats compared with the 65 needed for a majority. Swinney thus needs to secure votes or abstentions from outside his party. The Scottish Greens hold seven seats and are willing to support Swinney provided he continues to pursue progressive policies.

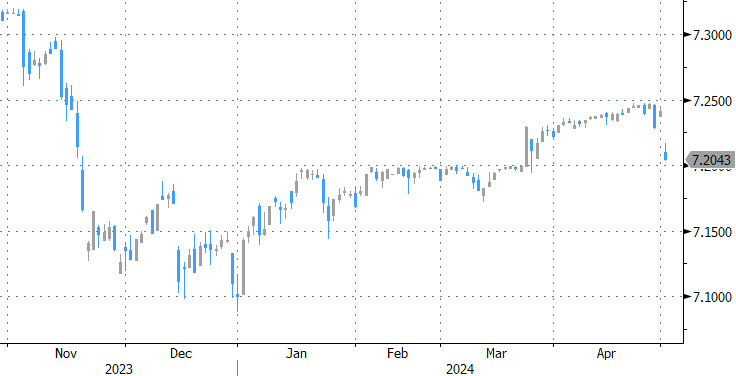

Graphs

German 10-y yield eases back below 2.50% as hopes on global easing resurface post Friday’s US data.

USD-DXY TW index struggles to hold 105 barrier as global monetary conditions ease.

USD/CNY: yuan strengthens after May holidays on weaker dollar and hope for Chinese activity to improve.

EuroStoxx 50 tries to escape ST downtrend channel.

gives European investors some additional comfort on an early ECB rate cut (June almost fully discounted).){kind=link}