Summary

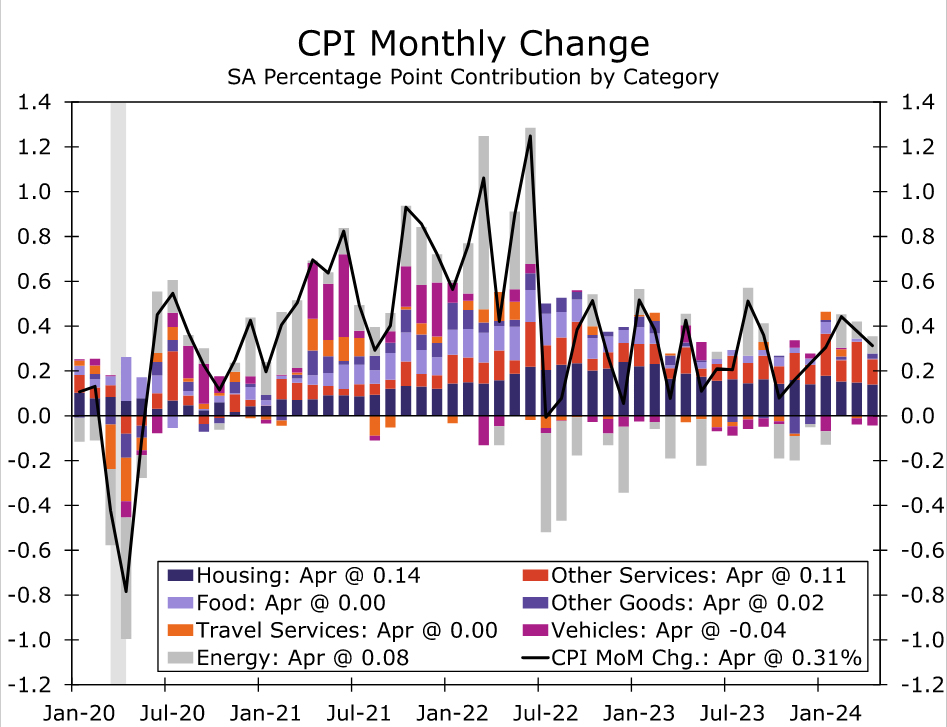

The first CPI report of Q2 should be seen as welcome news by the FOMC. The headline CPI rose 0.3% in April, a tenth below consensus expectations, while the core CPI also increased 0.3%, in line with expectations but a downshift from the pace registered in Q1. Flat food prices and a decline in energy services prices helped to partially offset a jump in gasoline prices in the headline index. Excluding food and energy, more deflation for vehicles prices and a moderation in price growth for medical care services, motor vehicle insurance and motor vehicle maintenance contributed to the slowdown in core CPI.

Based on the April CPI and PPI data, we estimate the core PCE deflator increased 0.25% month-over-month in April. If realized, this would bring the three-month annualized and year-over-year rates to 3.4% and 2.8%, respectively. On balance, the April inflation data should help restore some confidence at the Fed that price growth is continuing to moderate through the month-to-month noise. That said, we think it will take more than just one solid CPI report to induce the first rate cut. We believe it will take at least a few more benign inflation readings for the FOMC to feel sufficiently confident to begin lowering the fed funds rate. We continue to look for the first rate cut from the FOMC to come at its September meeting, but any additional bumps in the road would likely push that timing back, absent a marked deterioration in the labor market.

Tamer Inflation Reading to Start Q2

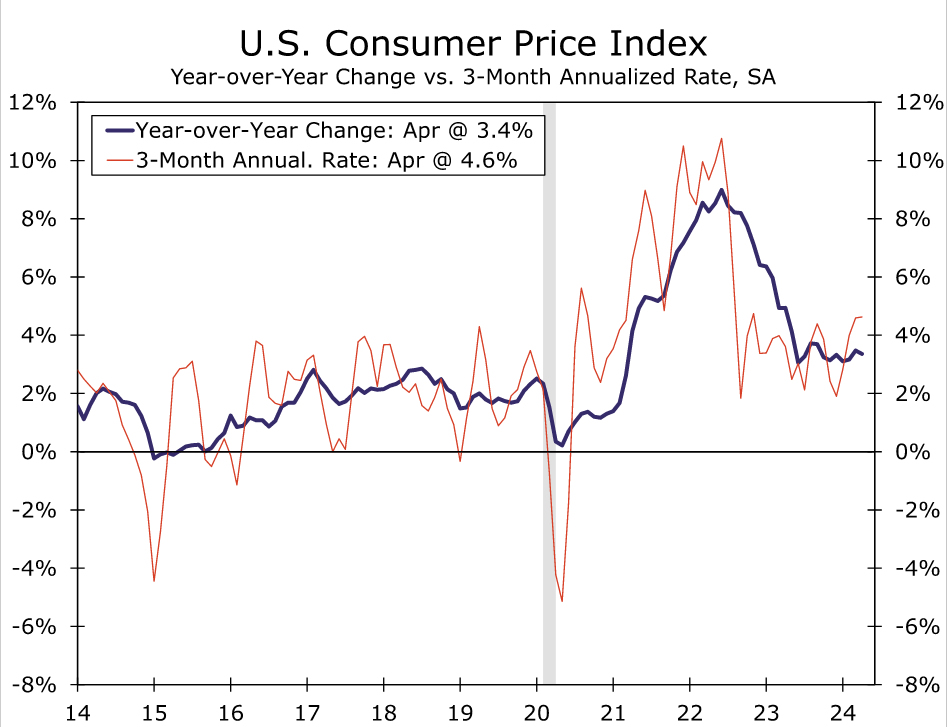

Consumer price inflation in April came in a touch softer than expected, rising 0.3% in the month against a consensus forecast for 0.4% (chart). Food prices were flat over the month as a 0.2% decline in grocery store prices was offset by a 0.3% increase in prices for food consumed away from home. Energy prices rose 1.1% in April, led by a 2.8% increase in gasoline prices. Prices at the pump climbed steadily over the past few months and have contributed to the leveling off in headline CPI inflation. A recent dip in oil prices and the early read on the May data suggest some giveback is coming in next month’s CPI report. Elsewhere, energy services prices declined 0.7% on the back of a sizable 2.9% drop in utility gas services. Compared to one year ago, the CPI has risen 3.4%, a tick down from the 3.5% registered in March but still modestly above the post-pandemic low of 3.0% hit back in June 2023 (chart).

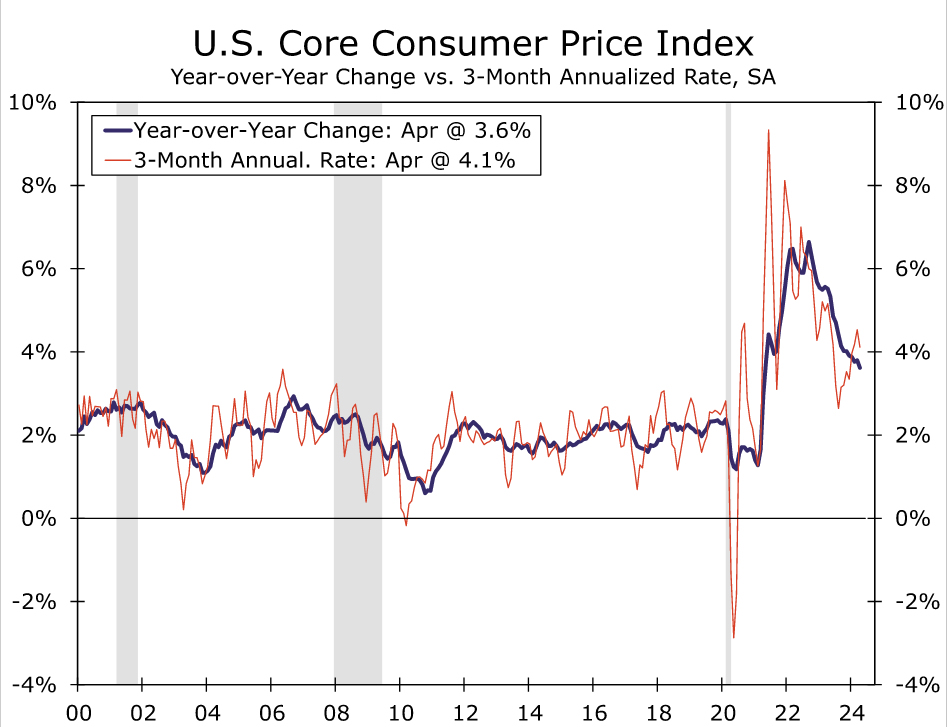

Excluding food and energy, price growth moderated in April. After three straight 0.4% gains, core CPI rose 0.3% (0.29% before rounding). On a year-ago basis, core prices are up 3.6%, the smallest increase in three years (chart).

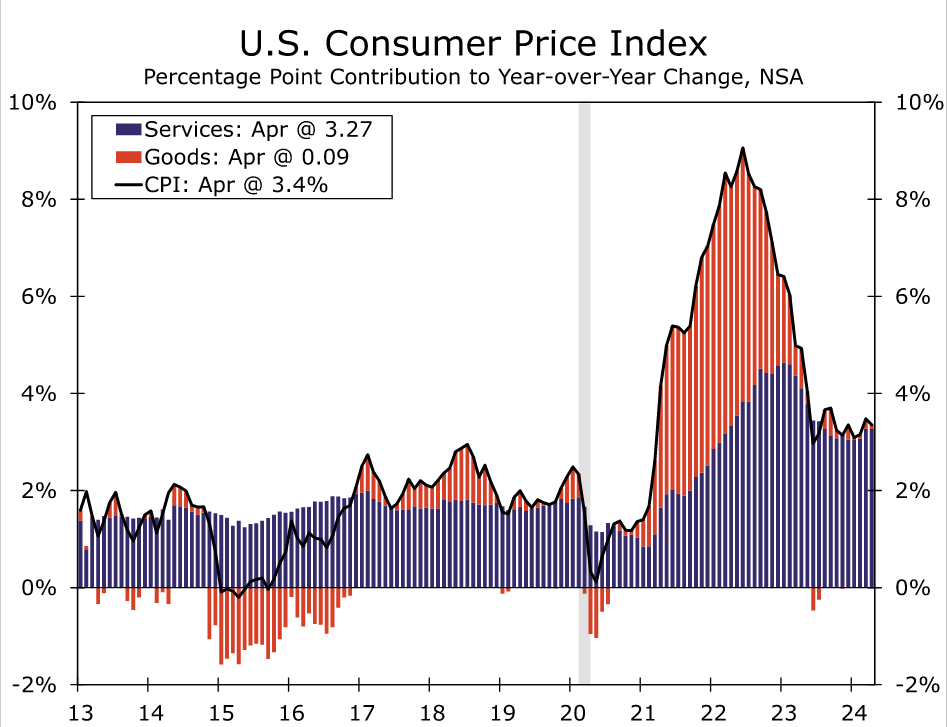

Core goods prices continued to decline in April, falling 0.1%. Notably, the drop was driven almost entirely by new and used autos (down 0.4% and 1.4%, respectively). “Other” core goods prices rose 0.5%, which was the largest increase since August 2022 and a sign that the disinflationary impulse from the goods sector is dissipating as the tailwind from healing supply chains and elevated inventories fades. Over the past year, core goods prices have fallen 1.2%, while total goods inflation (i.e., including food and energy) is up a benign 0.3%. Whether measured on a core or total basis, the sharp slowdown in goods inflation has accounted for the bulk of the decline in inflation since its peak in the summer of 2022 (chart).

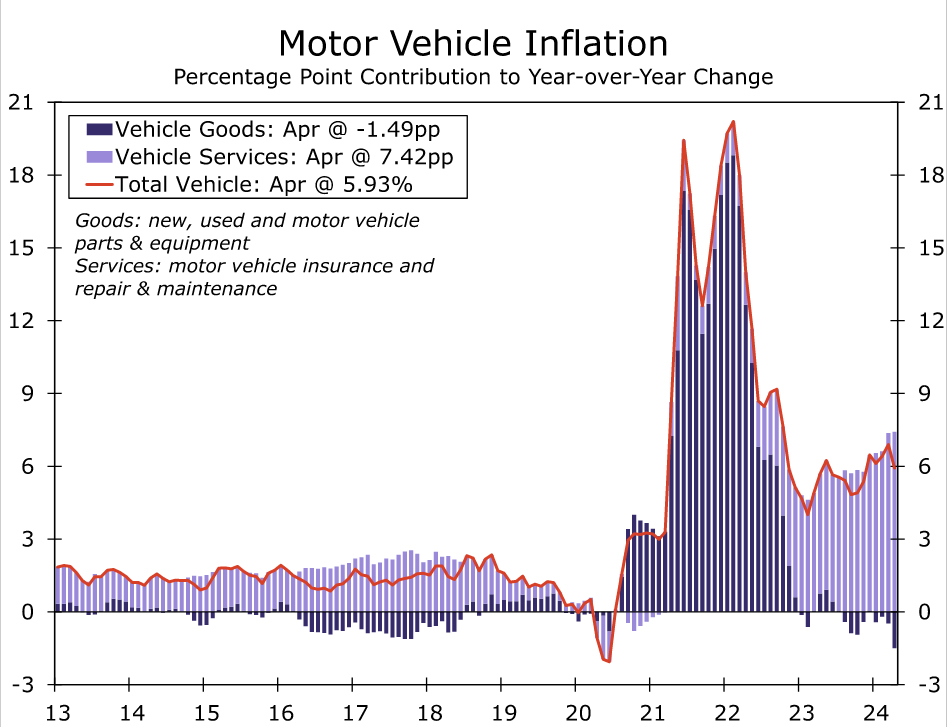

With goods inflation having returned to a pace similar to before COVID, the onus of further disinflation lies increasingly on services. Prices for services ex-energy have risen 5.3% over the past year compared to an average annual rate of 2.8% from 2015-2019. The April CPI showed inflation in the service sector easing once again, albeit at a still-painfully-slow pace. Core services prices rose 0.4% in April, returning to its Q4-23 pace. Primary shelter inflation eased somewhat further, with both owners’ equivalent rent and rent of primary residences moderating to a monthly increase of 0.41%. Excluding primary shelter, services inflation cooled more materially in April, with the “super core” up 0.4% after a 0.7% gain March. Contributing to the moderation was slower growth for medical services (+0.4%) and motor vehicle insurance and maintenance. Total transportation services are up 11.2% over the past year, largely due to the 22.6% jump in vehicle insurance. However, with vehicle prices having come off their peak, we expect to see related-services price growth start to cool in the months ahead (chart).

Taking into account today’s CPI data and the April Producer Price Index report, we estimate the core PCE deflator, the Fed’s preferred inflation gauge, rose 0.25% in April. If realized, the core PCE index would subside from a three-month annualized rate of 4.4% in March to 3.4% in April. Relative to one year ago, we expect the core PCE deflator to remain at 2.8%. The smaller sequential increase in core PCE in April would be a step in the right direction for the Fed to regain some confidence that inflation is subsiding, but we believe it will take at least few more benign inflation readings for the FOMC to feel sufficiently confident to begin lowering the fed funds rate. We continue to look for the first rate cut from the FOMC to come at its September meeting, but any additional bumps in the road would likely push that timing back, absent a marked deterioration in the labor market.

{kind=link}