- ECB members disagree about the rates outlook

- Key data releases including the June CPI figures

- A soft inflation report is unlikely to result in a dovish July ECB meeting

- Political risks keep the euro under pressure

The ECB hawks are clearly upset

It has been three weeks since the first ECB rate cut, and the situation feels very different to a traditional monetary policy easing cycle. Under normal conditions, every meeting would be considered a “live” one with most ECB members happily singing the same tune. However, this is not the case at this juncture.

The main message from the June 6 ECB gathering was that President Lagarde et al made the first crucial step, but they need to see a plethora of data confirming the disinflation process in order to cut rates again. This statement captures the sentiment in the ECB hawks’ ranks. They feel that they were pinned in the corner and hence forced to agree on a rate cut in June without really being convinced of the need for such an action.

However, they voted in favour of the rate move as backing down from a barrage of dovish comments, mostly from ECB doves, would have dealt another very serious blow to ECB’s credibility. Thursday’s release of the ECB meeting minutes could shed more light on the difficult behind-the-door discussions.

The barrier for another rate cut is higher now

The end product of this growing dichotomy is that the barrier for the next rate cut is much higher now. A month of weak data will not lead to a cut as the hawks want strong evidence that inflation is slowing down, especially in the services sector. Therefore, they appear determined to block any rate cut discussions until September when the new ECB staff projections will be ready. As such, the July meeting is not expected to produce a surprise.

The doves, though, remain committed to further ease monetary policy. Comments from ECB members Rehn and Knot about three rate cuts being reasonable in 2024 means that the debate during the next ECB meetings, starting with the July 18 one, could be described as hostile with President Lagarde facing her toughest challenge yet.

Maybe the ECB forum on Central Banking held in Sintra, Portugal on July 1-3 could help mend some of the ECB members’ differences. In addition, with the far-right parties faring well in the recent European elections, the ECB will probably draw even more criticisms than praise going forward. Hence, it is imperative for the next ECB actions to be extremely well thought-out and have the unanimous backing of the entire ECB council.

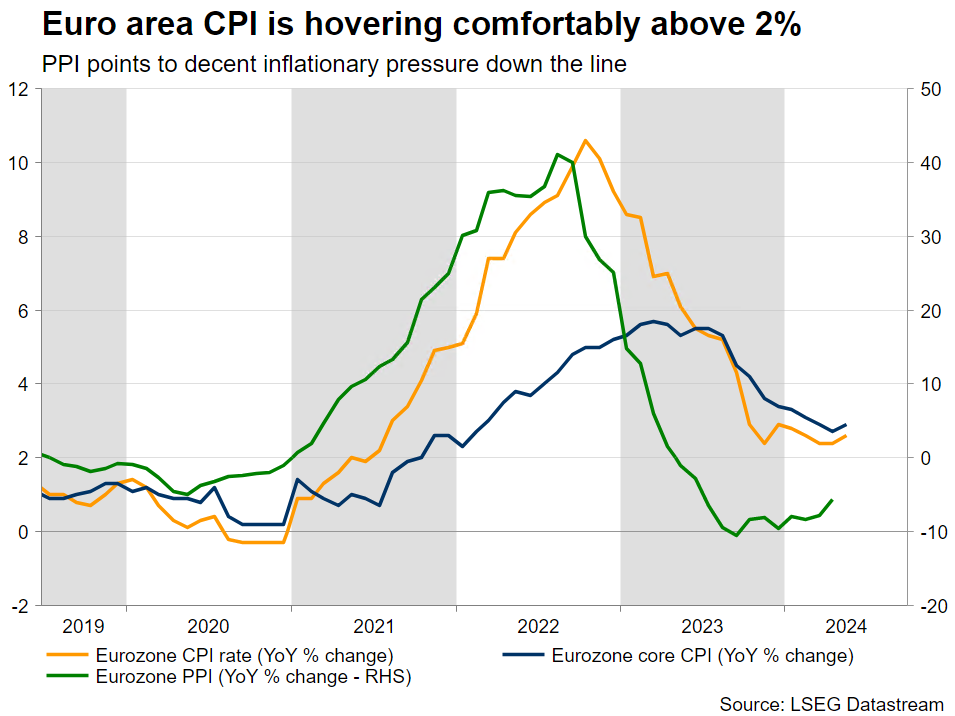

All eyes on the CPI report

At the end of the day, ECB members agree that the data will determine the ECB’s next steps. With the market most likely digesting the result of the first round of the French parliamentary election held this weekend, which could potentially unsettle even more the fragile European political scene, next week’s calendar starts on a high note.

The preliminary inflation report from Germany will be published on Monday with the Eurozone aggregate figures following on Tuesday. The final PMI surveys will also be released during the week with a decent chance of an upward revision in the German figures, but not in the French numbers as the local economy remains numb ahead of the parliamentary elections.

The market is currently expecting both the eurozone headline and core inflation rates to ease to 2.5% and 2.8% year-on-year respectively. The initial inflation prints from France, Italy and Spain point to a small possibility of an upside surprise to Tuesday’s prints. However, even in this case, the ECB doves will quickly try to dismiss the report. Chief Economist and Executive Board members Philip Lane has already been on the wires downgrading the importance of the monthly inflation reports, particularly when they are deemed to contain more noise than signaling power.

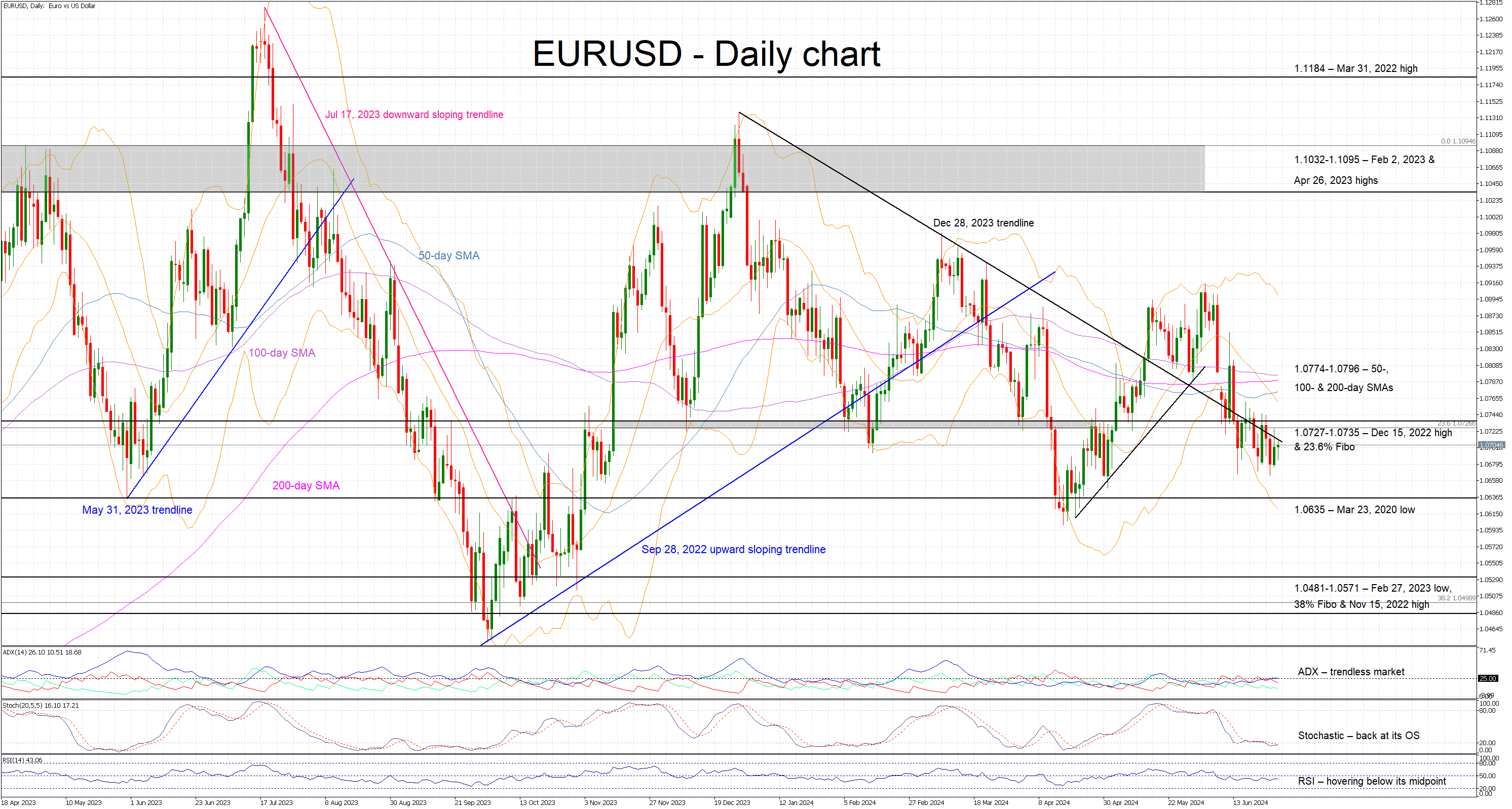

Euro remains under pressure as political risks linger

The euro remains on the backfoot against the US dollar as eurozone political risks linger and because the US continues to enjoy strong economic data that gradually push out the date of the first Fed rate cut. The outcome of the French elections could set the tone for next week, but the inflation report could quickly dictate the market moves.

A strong CPI report could help the euro reclaim the 1.0735 level and then tentatively open the door to a move towards the busier 1.0774-1.0796 area. On the flip side, a weak set of CPI prints might not increase the chances of a July ECB rate cut but it could add to the already negative market sentiment for the euro. A retest of the early April low at 1.0600 could reignite discussions about euro/dollar parity.

{kind=link}