{kind=link}

Summary

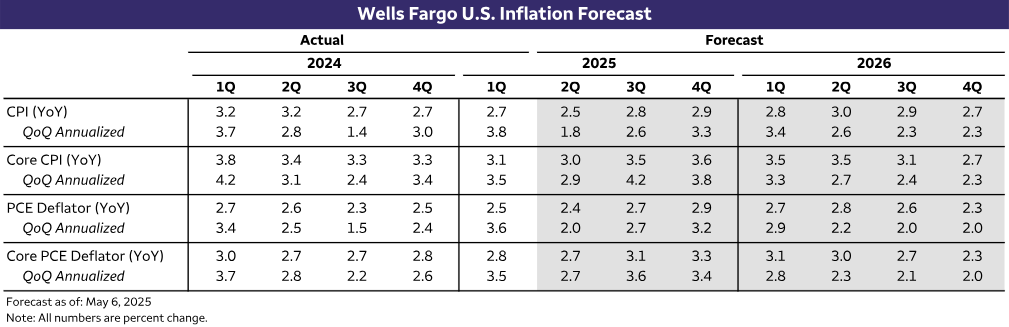

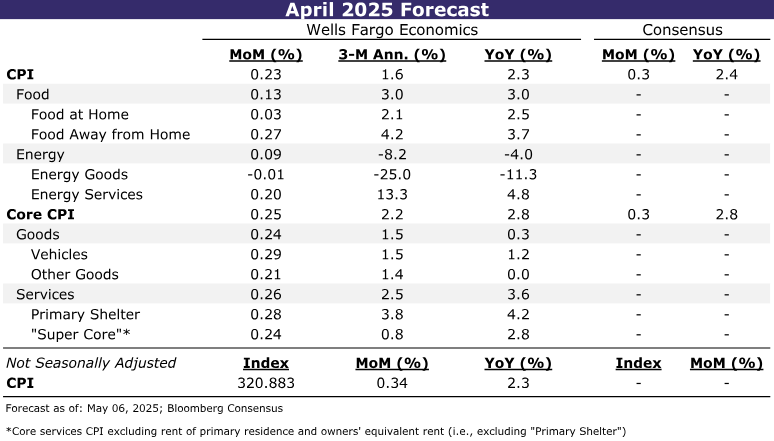

After an unexpected slide in March, the monthly change in the CPI in April is likely to rebound to its six-month trend. We look for the headline CPI to rise 0.2% in April, leading the year-ago rate to dip to a four-year low of 2.3%. We would not be shocked to see a 0.3% rise if some volatile components bounce back more than expected. Excluding food and energy, we forecast the core CPI to rise 0.25%, keeping the annual rate unchanged at 2.8%. Preemptive inventory building and fears of consumer pushback should keep the anticipated acceleration in consumer prices at bay until at least May. Yet beneath the surface, the subsiding trend in core services inflation will be juxtaposed with core goods inflation that is incrementally strengthening.

Sticker Shock on Hold

The March CPI report delivered the best of both worlds. There were few signs of tariffs igniting a widespread pickup in goods prices, while the downward trend in services inflation intensified. A repeat of March’s quiescent figures will be hard to come by in April. After slipping 0.1% in March, we estimate headline CPI rebounded 0.23% last month. Core CPI similarly looks set to bounce back from what was the smallest gain in four years (0.06%) with a 0.25% increase in April.

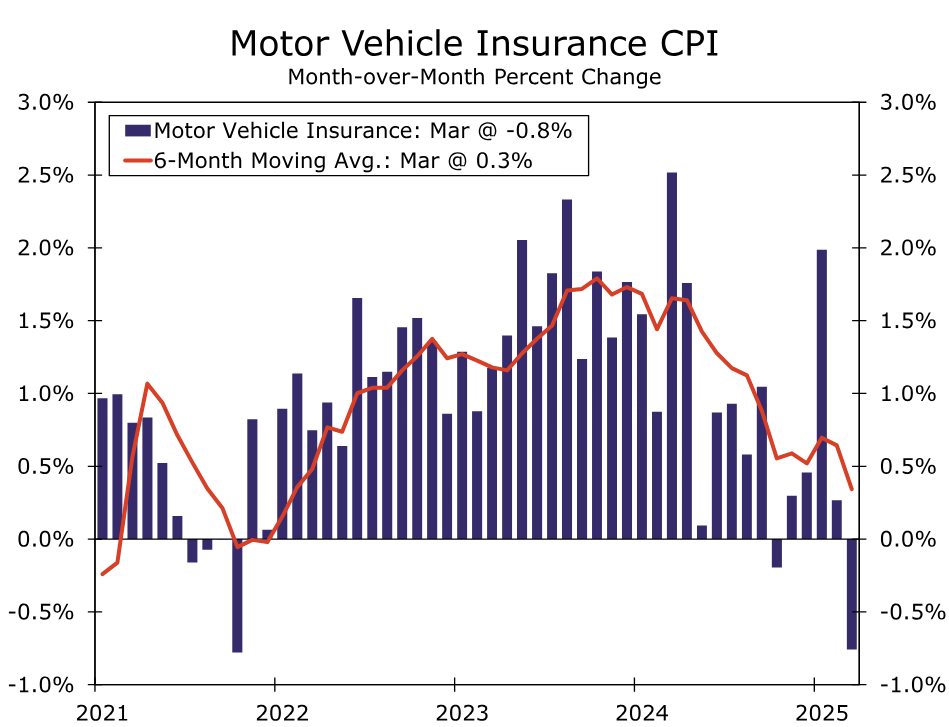

Our expectation for a rebound in April can be traced to the drivers of March’s tame reading, which centered on some of the more dynamic components of the CPI. Amid the flurry of federal government cost-cutting efforts and looming “Liberation Day” announcement of tariffs, concerns about the economy sent oil prices, airline fares and hotel prices sharply lower (Figure 1). Seasonal factors exacerbated the weakness, but seasonals will not be so friendly in April. We look for energy goods prices to be flat on the month and for travel-related services prices to decline less sharply (-0.4% in April versus -3.8% in March). Vehicle and insurance prices also look set for a rebound. Auto tariffs likely led auto dealers to hold a firmer line on pricing, while March’s 0.8% decline in motor vehicle insurance prices overstated the underlying trend (Figure 2).

At the same time, give-back in pricing of categories that saw outsized increases in March should keep a lid on services inflation in April. We anticipate primary shelter inflation to have eased in April after an above-trend reading in March, and we also look for a smaller increase in medical care services after hospital prices saw the largest gain in more than a year in the last report.

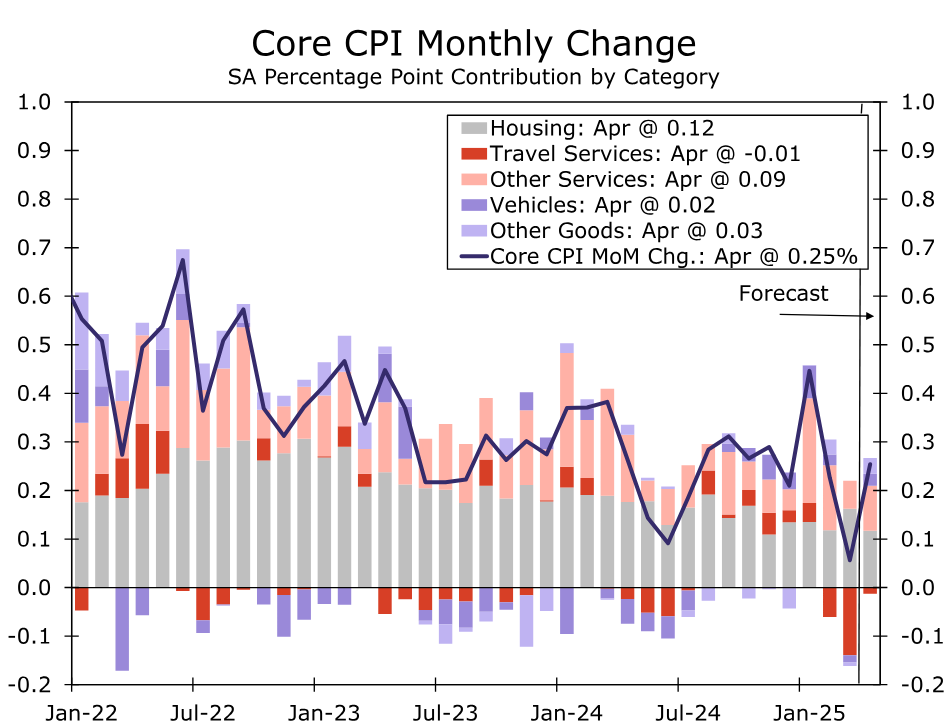

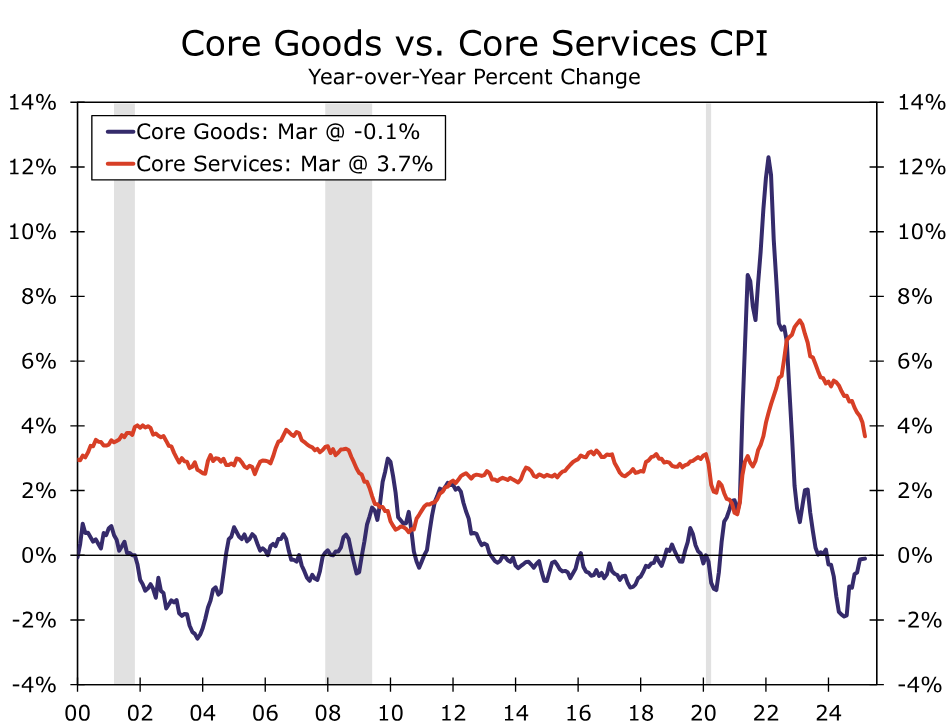

In contrast to the subsiding trend in core services, core goods inflation continues to strengthen. The announcement of sweeping increases to import duties at the start of the month stands to send the pickup in goods inflation into overdrive, although we do not expect April to be a light-switch moment. The pull-forward of imports, efforts not to alienate customers and general confusion over policy changes are likely to result in a more incremental strengthening in goods prices. We have penciled in a 0.24% increase in core goods prices for April (including the largest monthly gain in non-vehicle goods prices in more than two years) but expect the monthly pace to be double that by the summer if current trade policy remains in place. The gap between core goods and services inflation should continue to narrow as result (Figure 3).

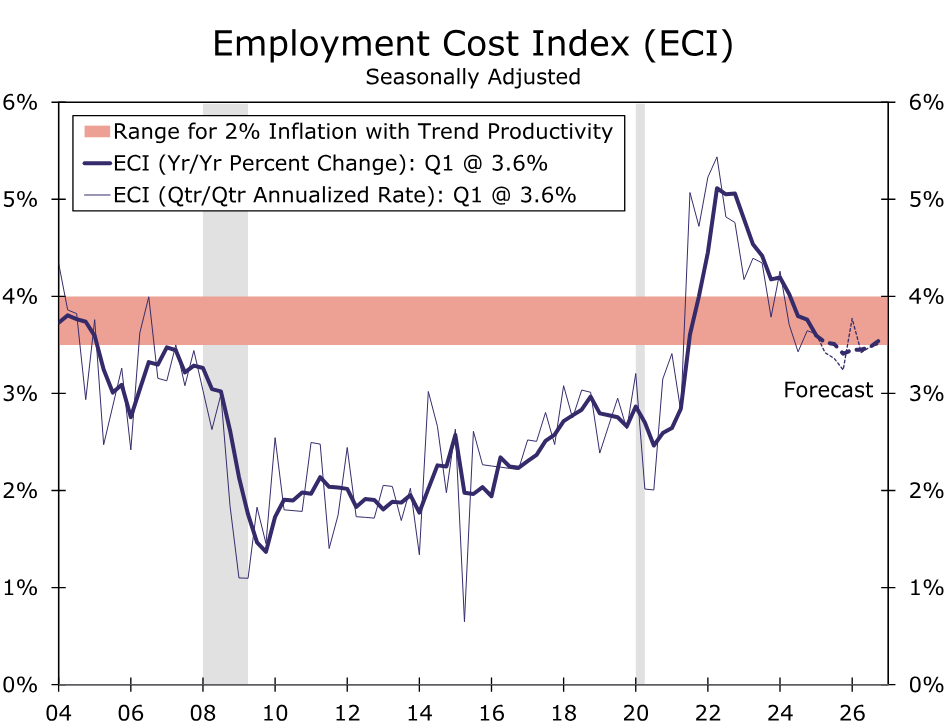

Stepping back, April’s monthly gain in headline CPI should push the year-over-rate rate down to a four-year low of 2.3%. The downward trend in core inflation is also likely to appear intact, with the year-ago rate unchanged at 2.8%. But with tariffs no longer merely a threat but a reality, we view it as only a matter of time before higher import costs filter through to consumer prices. We expect the inflationary impulse of tariffs to ramp up in the coming months, leading the core CPI back up to 3.6% by the fourth quarter (Table). Unlike the most recent price shock of the pandemic, trade changes are not occurring in combination with a positive shock to consumer demand and a historic scramble for workers. The less-flush position of households, slower growth in labor compensation costs and lower energy and transportation costs amid the weaker growth backdrop should help to mitigate the tariff-related rise in inflation (Figure 4). But that may be cold comfort to consumers, businesses and the Fed, as ground is lost in the nearly five-year battle to quell inflation.