decided at the conclusion of its meeting today to keep the target range for the federal funds rate unchanged at 4.25%-4.50%. After cutting rates by 100 bps between September and December of last year, the Committee has now been on hold for three consecutive policy meetings. The decision to keep policy unchanged was unanimously supported by all 12 voting members of the FOMC.){kind=link}

Summary

- The widely expected decision by the FOMC to keep rates on hold at today’s policy meeting was universally supported by all 12 voting members of the Committee.

- In its post-meeting statement, the FOMC noted that “uncertainty around the economic outlook has increased further” (emphasis ours). The statement included the previously used sentence that “the Committee is attentive to the risks to both sides of its dual mandate” but then added “and judges that the risks of higher unemployment and higher inflation have risen.”

- The sharp rise in the effective tariff rate likely will cause both inflation and the unemployment rate to rise in coming months. Hence, there may be some tension in terms of the Fed’s dual mandate (i.e., “price stability” and “full employment”) in coming months.

- The best course of action for the FOMC may simply be to wait for more clarity about trade policy and its implications for the U.S. economy. Indeed, Chair Powell seemed to indicate as such during his post-meeting press conference.

Tariffs Have Caused Uncertainty to Increase Further

As universally expected, the Federal Open Market Committee (FOMC) decided at the conclusion of its meeting today to keep the target range for the federal funds rate unchanged at 4.25%-4.50%. After cutting rates by 100 bps between September and December of last year, the Committee has now been on hold for three consecutive policy meetings. The decision to keep policy unchanged was unanimously supported by all 12 voting members of the FOMC.

As is typical for the third FOMC gathering of the year, the Federal Reserve did not release a Summary of Economic Projections (SEP), which summarizes the FOMC’s macroeconomic forecasts, after the conclusion of today’s meeting. So if the Committee wanted to give any guidance as to its intentions going forward, it would need to do so via the post-meeting statement. In that regard, the statement was very much noncommittal. At the time of the last FOMC meeting on March 19, President Trump had not yet announced his “Liberation Day” tariffs, which were widely seen as being higher than expected. The March 19 statement noted that “uncertainty around the economic outlook has increased.” Although the president has paused his “reciprocal” tariffs until July, today’s statement added “further” to the end of the last sentence. Additionally, statements from the last few FOMC meetings have noted that “the Committee is attentive to the risks to both sides of its dual mandate.” Today’s statement included that sentence but added “and judges that the risks of higher unemployment and higher inflation have risen.”

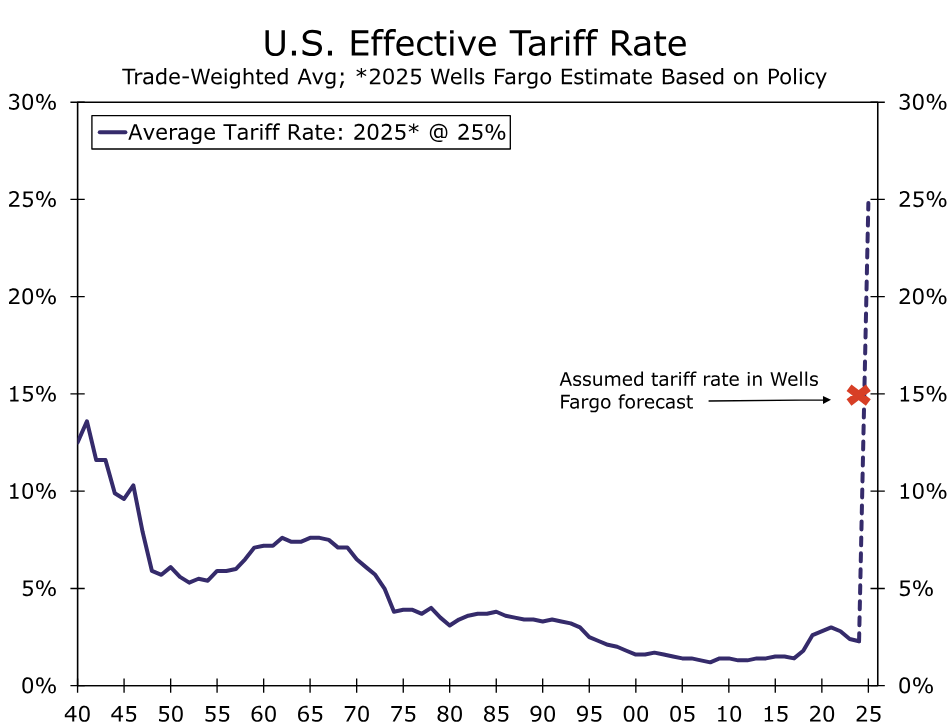

At present, a 10% universal tariff applies to most goods imported from most countries with a 145% tariff applied to most goods from China. We estimate these levies yield an effective tariff rate of roughly 25%, the highest rate in over a century (Figure 1). As we discussed in a report we published soon after “Liberation Day,” tariffs of that magnitude would lead to a meaningful rise in inflation and sharp downturn in real GDP later this year. (Unemployment would rise as the economy weakens). We think the effective tariff rate will recede somewhat as the Trump Administration reaches trade deals with some trading partners. But we think a return to the 2% effective tariff rate of 2024 is highly unlikely. For purposes of our last forecast, which we published on April 8 and which can be found here, we assume the effective tariff rate will fall to 15%.

FOMC Likely On Hold Until It Gets More Clarity

Nevertheless, the rise in the effective tariff rate relative to earlier this year likely will cause inflation to move higher and the unemployment rate to increase in coming months. On one hand, the FOMC would want to ease policy as the jobless rate rises. On the other hand, however, rising inflation would induce Fed policymakers to refrain from easing policy, if not tighten it. In other words, there may be some tension in terms of the Fed’s dual mandate (i.e., “price stability” and “full employment”) in coming months. The best course of action for the FOMC may simply be to wait for more clarity about trade policy and its implications for the U.S. economy. Indeed, Chair Powell reiterated during his press conference that “we don’t think we need to be in a hurry to adjust rates.” Given the underlying solid nature of the economy, which the FOMC noted in its post-meeting statement, Powell said that “the costs of waiting are fairly low.”

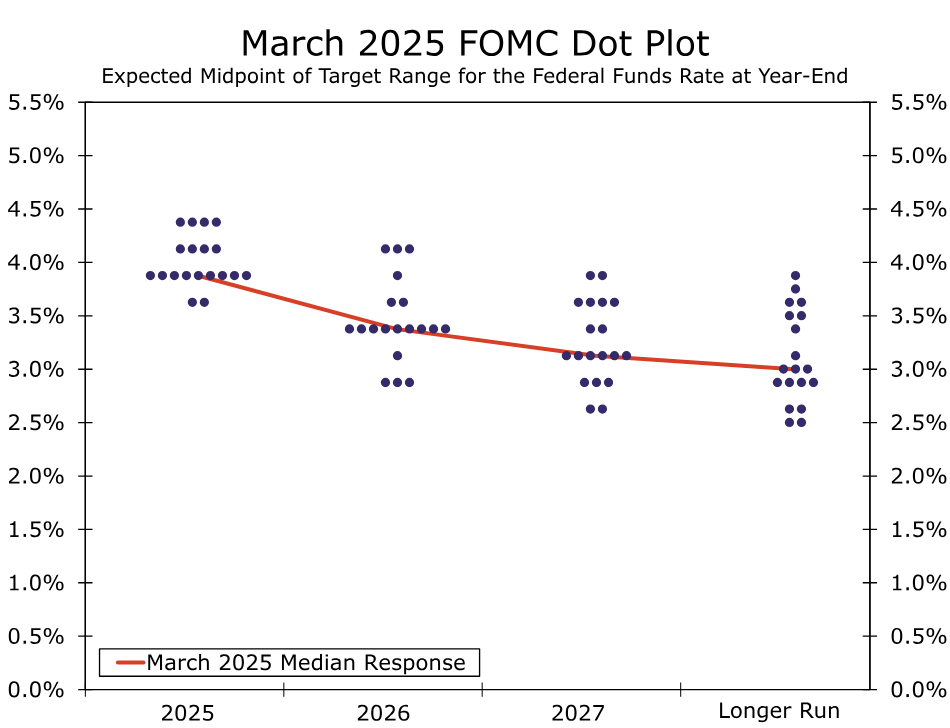

As noted previously, our latest forecast was published about a month ago. That forecast looked for the FOMC to begin an easing cycle with a 25 bps rate cut at its next policy meeting on June 18. We readily acknowledge, however, that the risks to that forecast now seemed skewed toward a later start to our expected easing cycle than June. That forecast also looked for 125 bps of rate cuts by the end of the year, which now appears to be a bit aggressive. We will be publishing a new forecast tomorrow (May 8) in which we still see the FOMC eventually easing policy this year. Furthermore, we think the Committee will cut rates by more than 50 bps, which the median FOMC respondent foresaw in the March “dot plot” (Figure 2). Our new forecast will be sent to email recipients early tomorrow morning (May 8) and posted to our website by the end of the day.