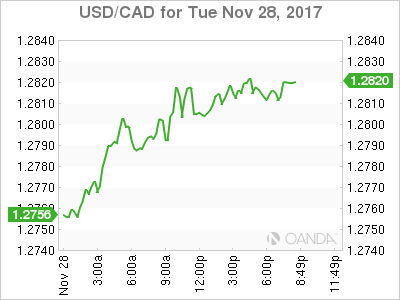

The Canadian dollar depreciated on Tuesday with the US dollar gaining on confident consumers and improving housing prices in the United States. Canadian producer prices rose 1.0 percent in October thanks to auto prices being sensitive to a currency fluctuations. Raw materials rose 3.8 percent as energy prices keep rising. Despite the rise in inflation indicators the loonie could not gain a foothold against the USD. The Bank of Canada (BoC) presented its Financial System Review and Governor Poloz held a press conference to discuss the findings of the economic assessment.

In the last review six months ago the central bank had struck notes of concerns regarding high levels of household debt and rising house prices. Now with two rate hikes between them and new regulation in place to avoid a housing bubble the BoC was seen as optimistic, but gone were the hawkish undertones of the summer. The Canadian central bank remains concerned with household debt as it exposes borrowers to higher rates but that could be offset by a strong jobs component with growing wages. Poloz said that the risks were unchanged, but the policy changes in housing finance are a step in the right direction. The BoC is not expected to make another adjustment to the Canadian benchmark rate until 2018 as there are improvements in the indicators, but the jury is still out on the price fo crude and the fate of NAFTA.

Trade relations between the US and Canada just got thornier after the latter just initiated a WTO case against the US for the duties it imposed on Canadian lumber. This follows the NAFTA challenge issued in early November. The renegotiation of the 23 year old trade agreement have not gone to plan and in some best case scenarios the deal would be close to being wrapped up before the end of the year. The reality is that the negotiating teams are far apart, specially the US Trade representatives who are pushing an America First agenda that leaves little room to compromise.

The USD/CAD gained 0.36 percent on Tuesday. The currency pair is trading at 1.2815 after Fed Chair nominee went before the US Senate to testify. He remains a hawk in the style of Janet Yellen and talking about the December rate hike. The rise of consumer confidence as reported by the Conference Board is now at a 17 year high, which bodes well for tomorrow’s release of the second estimate of third quarter gross domestic product (GDP) data. The Bank of Canada (BoC) Financial System Review and the word form Governor Poloz could not offset the strong US data and the loonie depreciated.

The Bank of Canada (BoC) hiked twice in 2017, but that only put the Canadian benchmark rate back to 1 percent where it was when Governor Poloz cut the rate twice to boost the economy ahead of the fall of oil prices. The loonie will face more pressure as the Fed continues its monetary policy tightening pace, while the BoC will be more cautious as it monitors rising household debt.

Job numbers will be released in Canada on Friday, December 1. Statistics Canada will publish the monthly GDP figures as well as the employment report both at 8:30 am EST. GDP is expected to have shrunk by 0.1 percent and there is some anxiety on the job front as the first ADP job report for Canada showed a loss of 5,700 in October. The US GDP for the third quarter is expected to have improved between the first and second estimates, and if the Canadian economy continues to show signs of cooling it will put more pressure not the CAD ahead of the December monetary policy meetings of both central banks.

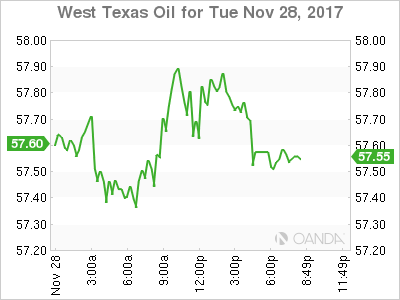

Oil prices recovered some ground in the last 24 hours. West Texas Intermediate is trading at $57.73 awaiting the news to come out of the Organization of the Petroleum Exporting Countries (OPEC) meeting in Vienna. The price of oil has already priced in an extension as multiple comments from OPEC and non-OPEC members have pointed to increasing the deadline past March 2018. The main remaining issue is how long will the agreement be extended by. The consensus at this point is for a 9 month extension with a meeting at the six month mark to review.

Earlier today a committee made up by OPEC and non-OPEC members recommended the extension until the end of 2018, with the option of a review in June. Comments from energy Ministers have been supportive, but the duration of the deal is still up for debate in the next couple of days.

US production has increased and with the Keystone pipeline restarted operations, but still at reduced capacity. Disruptions in North America due to weather and forest fires has kept production lower than otherwise expected with the OPEC doing the heavy lifting on price stability. The market will be watching for developments in Vienna as the floor of energy pricing has been put in place by the OPEC production cut, and once it reaches its end crude prices will be vulnerable if global demand for energy has not recovered at the same rate as production.

Market events to watch this week:

Wednesday, November 29

- All Day All OPEC Meetings

- 8:30am USD Prelim GDP q/q

- 10:30am USD Crude Oil Inventories

- 7:00pm NZD ANZ Business Confidence

- 7:30pm AUD Private Capital Expenditure q/q

Thursday, November 30

- 8:30am USD Unemployment Claims

Friday, December 1

- 4:30am GBP Manufacturing PMI

- 8:30am CAD Employment Change

- 8:30am CAD GDP m/m

- 10:00am USD ISM Manufacturing PMI

*All times EDT