.){kind=link}

- We expect the Fed to maintain its monetary policy unchanged in the June meeting, in line with consensus and market pricing.

- We expect this year’s GDP growth estimate to be revised down reflecting the impact from post-Liberation Day tariffs. Core inflation forecasts will also be likely adjusted slightly higher. 2026-27 forecasts will be less affected.

- We still expect the Fed to cut rates twice in 2025 in line with March dots, followed by three more cuts in 2026. We do not expect strong forward guidance from Powell, but see risks skewed towards modestly dovish market reaction.

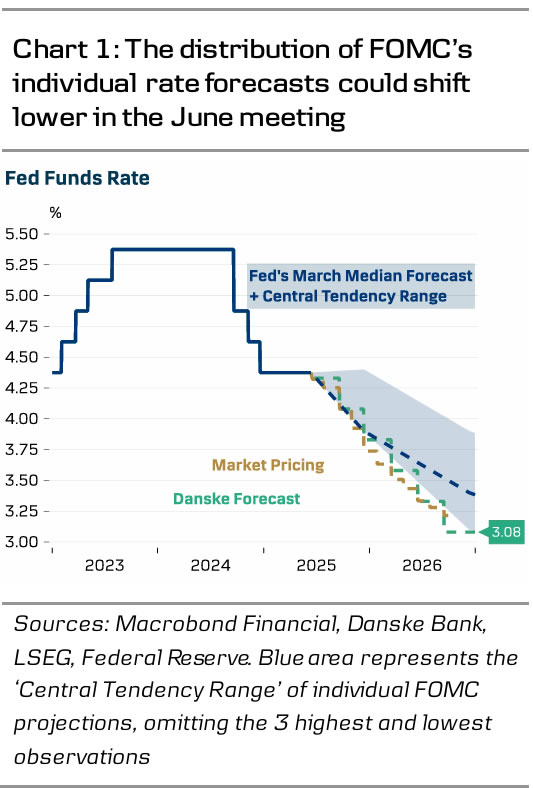

FOMC participants have remained mostly on the sidelines since the May meeting. Some have sounded open to the idea of cutting 1-2 more times during rest of 2025, but most have carefully avoided influencing financial conditions amid the tariff uncertainty. Current market pricing is just slightly below the Fed’s March median ‘dots’ for 2025-26 despite the significant market volatility observed ever since (chart 1).

We expect a sizable downward revision to FOMC’s median 2025 GDP forecast in the updated Summary of Economic Projections (SEP), reflecting the post-Liberation tariff impact. On a comparable Q4/Q4 basis, our forecast is only +0.9% for 2025 (consensus 1.0%, March SEP: 1.7%) and +1.8% for 2026 (consensus 1.7%, March SEP 1.8%).

Core PCE forecast could shift a bit higher for 2025. Lower energy prices might counteract some of the tariff impact for the headline PCE, although the latest jolt of geopolitical uncertainty blurs the outlook. We expect unemployment rate forecast to remain steady, as tighter supply from immigration is counteracting the demand-effect from slowing hiring.

We will keep a close eye on the Fed’s assessment on the balance of risks. Back in March, FOMC participants reported that inflation risks had become increasingly skewed to the topside, but that GDP and unemployment risks were better balanced. In May, Powell verbally stated that both growth and inflation uncertainty had increased, but he avoided specifying which risk felt more pressing at the time.

Since May, incoming data has signalled that firms’ increased tariff payments are on track to reach roughly USD190-200bn per year (or around 0.6% of GDP, see RtM USD, 27 May). Wage growth hovers just above 4% per year (according to Atlanta Fed) but realized inflation surprised to the downside in May across both goods and services (see Global Inflation Watch, 11 June). As firms are not yet passing through the rising costs to selling prices, the trade war is putting pressure on margins, which could tilt the Fed to feel more concerned about the labour market. Whether price hikes are delayed simply as a choice amid uncertainty, or due to lack of pricing power, remains to be seen.

We still think risks are skewed towards more, rather than less cuts, and we maintain our terminal rate forecast at 3.00-3.25% – somewhat below current market pricing. While we expect Powell to follow his colleagues’ recent footsteps and carefully avoid strong forward guidance, risks could be tilted towards lower rates and further USD weakness if Powell gives a clearer signal that resuming rate cuts is not a question of if but when.