Wednesday November 29: Five things the markets are talking about

Global equities continue to find support as investor optimism over U.S tax reform trumps concerns about North Korea’s latest missile launch.

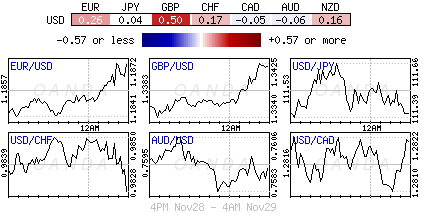

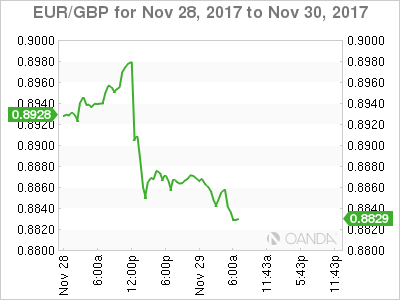

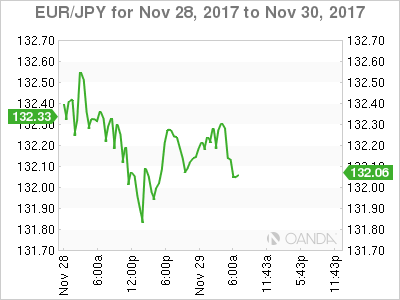

In FX, the pound (£1.3422) has jumped to a two-month high as Brexit negotiators seem to have agreed to an outline divorce deal worth around €50B. The ‘mighty’ dollar remains on the back foot, while the EUR (€1.1864) advances as data from Germany’s regions showed inflation and consumer confidence accelerating.

Note: The U.S Senate tax bill is headed for a marathon debate later this week after the budget committee voted yesterday along party lines to send the Republican plan to the floor.

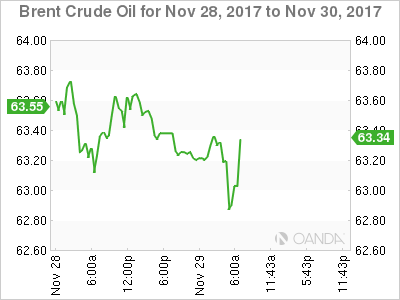

In commodities, crude oil prices fall for a third consecutive day as U.S inventory data expanded ahead of tomorrows OPEC meeting to decide on prolonging supply cuts past the end of March, 2018. However, there is ‘radio silence’ from non-OPEC member Russia, which could be a stumbling block to a potential new agreement.

Also yesterday, new Fed Chair nominee, Jerome Powell, has assured the market of a “steady, responsible hand” and the case for a December rate hike “is coming together.”

This morning, the second print of Q3 U.S GDP is expected to be revised a tad higher (+3.3% vs. +3%) on the back of stronger consumer spending and inventory accumulation.

1. Stocks find strong support

In Japan, stocks rallied overnight as banks and financial shares tracked Wall street higher, shrugging off another N. Korean missile launch. The Nikkei share average ended +0.5% higher, while the broader Topix advanced +0.8%.

Note: Global financial and securities shares are taking the sector lead, supported mostly by new Fed Chair nominee Powell’s defending the need to potentially lighten regulation on the financial sector.

Down-under, Australia’s S&P/ASX 200 Index rose +0.5%, while S. Korea’s Kospi index dropped less than -0.1%.

In Hong Kong, shares ended the session lower despite other regional gains, with investors’ risk appetite curbed by N. Korea’s latest missile test. The Hang Seng index was down -0.19%, while the Hang Seng China Enterprises index fell -0.49%.

In China, stocks ended firmer, strengthened by a surge in property shares and resources firms. The Shanghai Composite index was up +0.13%, while the blue-chip CSI300 index was down -0.05%, with its financial sector sub-index higher by +0.77%.

In Europe, regional indices trade mostly higher across the board with the exception of the FTSE 100, which trades a tad lower on talk of a Brexit divorce bill, having been preliminary agreed upon between the U.K and E.U.

In the U.S, stocks look set to open little changed.

Indices: Stoxx600 +0.6% at 389.3, FTSE -0.5% at 7422, DAX +0.7% at 13148, CAC-40 +0.5% at 5417, IBEX-35 +1.2% at 10267, FTSE MIB +0.6% at 22417, SMI +0.1% at 9330 S&P 500 Futures flat.

2. Oil falls on uncertainty over OPEC deal, gold higher

Oil prices are under pressure as doubts set in about Russia’s willingness to substantially extend a deal to curb global output.

Ahead of the U.S open, Brent crude futures are down -34c at +$63.27 a barrel, while U.S light crude has fallen -31c to +$57.68 a barrel.

Note: Oil prices have rallied by about +40% since the middle of the year, supported by a deal between the OPEC and non-OPEC members, such as Russia, to reduce crude oil production by -1.8m bpd. The deal expires in March 2018, but it’s expected to be extended at tomorrow’s meeting.

However, Russia is concerned that a more robust extension could lead the oil price to rally too sharply, which would send the Russian rouble higher and harm exports. It’s also worried that a steep price rise could trigger another increase in U.S production.

Note: API data yesterday showed that U.S. crude inventories rose by +1.8m barrels in the week ended Nov. 24. The market was looking for a -2.3m barrel drop.

Gold prices have crept a tad higher amid a weaker dollar, while N. Korea’s latest missile test seems to have had little impact on the safe-haven metal. Spot gold is up +0.2% at +$1,295.92 an ounce.

3. U.S yield curve flattens

The U.S Treasury yield curve continues to flatten, with the 10-year note at +2.32%, down -1 bps, while U.S two-year note trades unchanged at +1.74%. The spread trades atop its 10-year low at +58 bps.

Jerome Powell’s testimony to the Senate Finance Committee yesterday seems to have assured the market that Trump’s nominee would ‘not’ do much different from Ms. Yellen in setting monetary policy. Powell confirmed market expectations that the case for another +25 bps “is coming together” next month, although he cautioned nothing has been decided.

Fed funds futures are putting a +96% probability on a hike with a probability of another +25 bps hike above +50% by mid-2018. The consensus of Fed watchers call for three rate increases in 2018.

Elsewhere, Germany’s 10-year Bund yield has increased +2 bps to +0.34%, the biggest increase in almost three-weeks, the U.K’s 10-year Gilt yield increased +6 bps to +1.253%, the highest in more than two-weeks

4. Little support for the ‘big’ dollar

The U.S dollar is finding it difficult to gain traction, pulled down by broad strength in GBP and EUR as well as worries over a possible U.S government shutdown after Democrats pulled out of a meeting with President Trump yesterday.

Note: The not so ‘mighty’ dollar is on track for its worst month in four-months, and its worst year in fourteen-years, has dipped another -0.2% against the majors ahead of the U.S session.

The EUR (€1.1867) is +0.2% higher supported by a number of German states reporting a stronger than expected CPI data for Nov – several states readings w ere above the ECB target of around +2.0%.

GBP/USD (£1.3402) is trading atop of its two-month highs as some concerns of a ‘hard’ Brexit were diminished after reports circulated that U.K will move closer to the E.U demands for a financial settlement. Market expectations of next potential Bank of England (BoE) rate hike seem to have moved forward to Sept 2018 from Nov as a result of progress.

5. Eurozone confidence continues to rise

Euro data this morning brought some good news for the ‘single’ unit and the European Central Bank (ECB).

The European Commission’s Economic Sentiment Indicator continued to rise this month, hitting its highest level in 17-years as the reading of 114.6 slightly exceeded market expectations.

As with last week’s German PMI release, the survey bodes well for the economy’s momentum going into next year, and there was also a note of encouragement for the ECB in its long battle to boost inflation in the form of another pickup in the rate of price increases expected by consumers over the next year.