{kind=link}

Summary

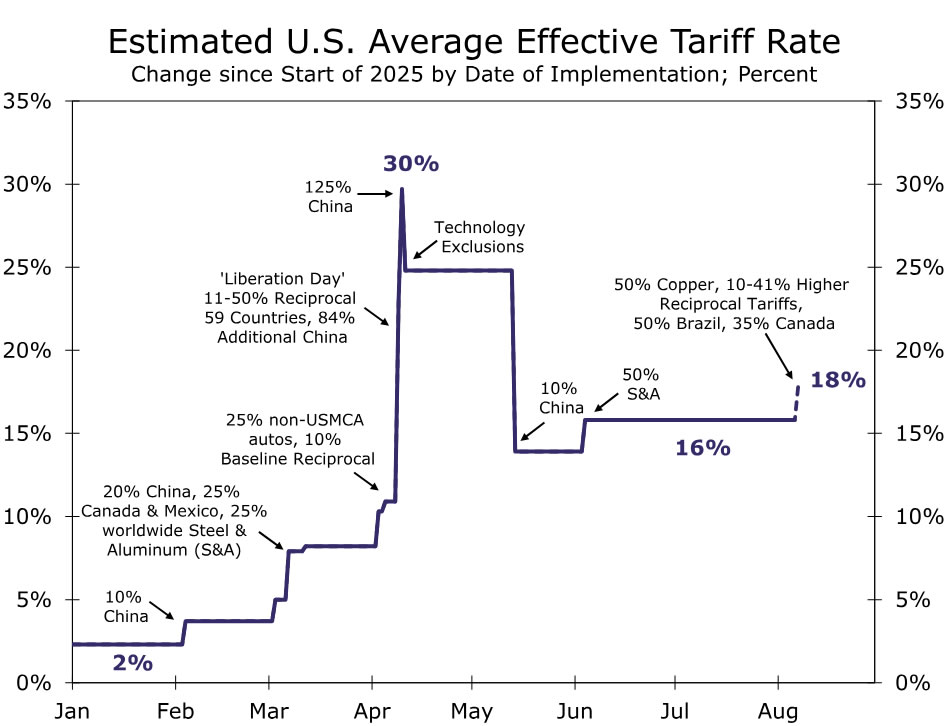

Recent trade announcements have been billed as an escalation in the trade war. By our reckoning, the upshot is actually an effective tariff rate of 18%. That is the midpoint between the 16% rate in place prior to yesterday’s announcement and the roughly 20% rate that would have been in effect today in the absence of it.

Can You Keep Up?

Yesterday evening President Trump announced updated tariff rates of 10-41% on over 60 countries. This comes after Trump twice paused higher reciprocal rates originally announced in early April to allow for negotiations. Yesterday’s announcement has been billed as a complete reshaping of global commerce, yet that is really not quite the way to think of this.

The reshaping already happened on April 2 when the President offered his opening bid in his campaign to force a new global trade system. The sweeping tariff orders announced yesterday effectively create a more practical framework and in many cases offer a lower tariff rate than would have been the case had things reset on August 1. Beyond the latest round of reciprocal rates, the Administration announced tariffs on copper products as well as a trade deal with the European Union and additional tariffs on Brazil this week. Yet, even with this latest codification of tariff rates, much remains in flux as deal-making continues and as the President continues to use tariffs for leverage in foreign affairs.

State of Play: What’s in Effect and What Do we Know?

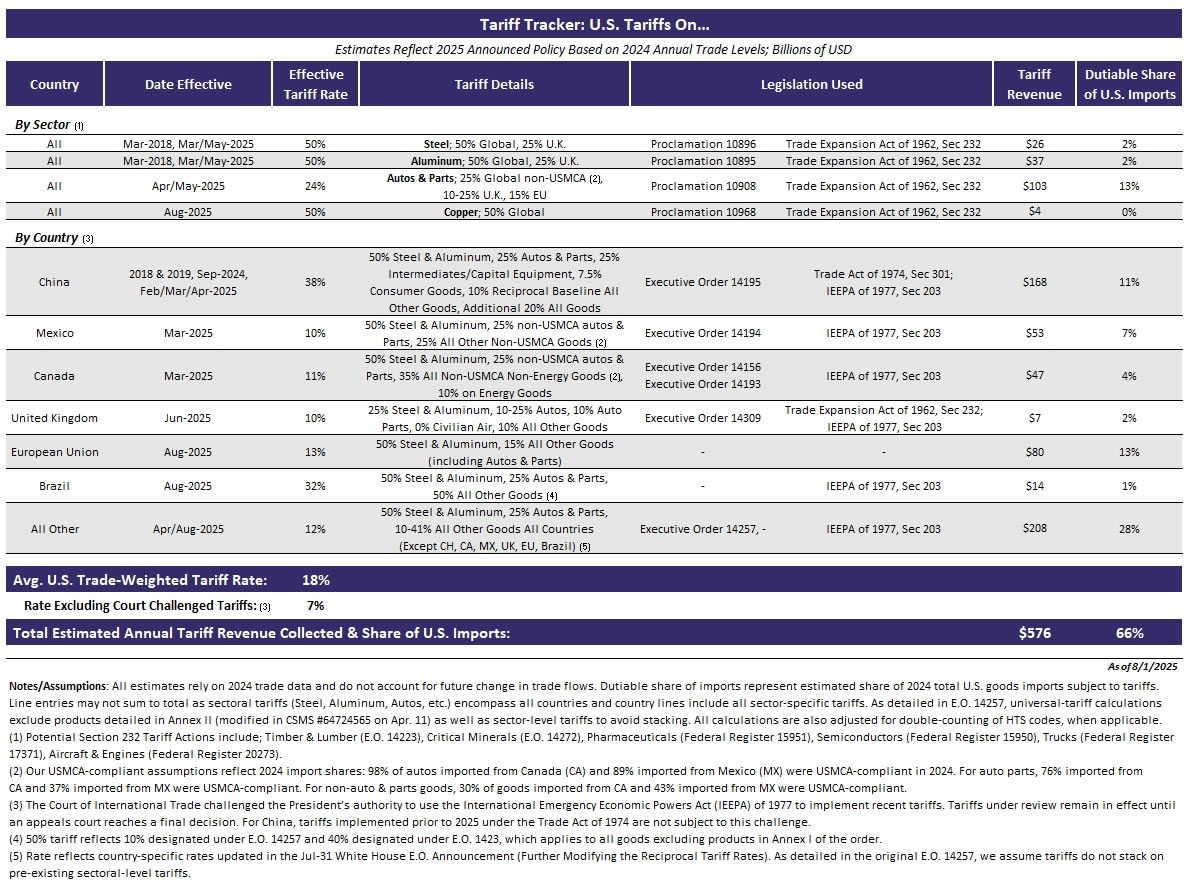

Here is a summary of the main tariff changes as of today, August 1:

- Copper: 50% on exposed copper products from every country (Effective August 1).

- Previously: 0%

- European Union: 50% on steel, aluminum, copper. 15% tariff on all other exposed goods (including autos & parts). Official Executive Order not yet available (Effective August 7).

- Previously: 50% on steel, aluminum. 0% copper. 25% autos & parts. 10% tariff on all other goods.

- Brazil: 50% steel, aluminum, copper. 25% autos & parts. 50% all other exposed goods (Effective August 1).

- Previously: 50% on steel, aluminum. 0% copper. 25% autos & parts. 10% all other goods and additional 40% all goods.

- All countries, other than China, Canada, Mexico: 50% on steel, aluminum, copper. 25% autos & parts. 10-41% on all other exposed goods (Effective August 7).

- Previously: 50% on steel, aluminum. 0% copper. 25% autos & parts. 10% on all other goods.

Nailing down the precise effective tariff rate in such an ever-changing environment is a never-ending task for economists and trade experts and a source of enduring uncertainty for businesses weighing cap-ex decisions. We estimate that once all these recent changes to tariff policy go into effect, it will lift the average trade-weighted tariff rate to ~18% in the United States, from 16% prior to these adjustments (chart). Despite the August 1 deadline bringing clarity for some countries, the can was kicked down the road for others such as China and Mexico. Trump extended the 90-day pause on China and imposed a similar pause on Mexico, making the start of November another key deadline.

Despite recent announcements, uncertainty lingers. The higher reciprocal rates are also not set to go into effect until next week on August 7, which leaves some time for potential changes to be made. There is also a grace period for product in shipment, meaning goods shipped within the next seven days and entering the country ahead of October 5 will be tariffed at the previous lower 10% rate. This could push firms that rely on goods from countries where rates have risen most dramatically, such as Switzerland and India, to rush and get orders shipped, which could again lead to a spurt of import growth and also delay any potential pricing impact from the escalation.

Another extension to the 90-day pause on higher reciprocal rates with China has also been floated by U.S. Treasury Secretary Scott Bessent this week, but Trump has not yet formally confirmed this. Additionally, while the Administration released a Fact Sheet on the trade deal with the European Union, it has not yet released a formal executive order, leaving some of the exact details of the deal unclear. This not only breeds confusion for businesses determining what rates their products are now exposed to, but prevents U.S. Customs and Border Protection from being able to accurately enforce tariff rates.

Summary of the pending changes:

- China: 90-day pause on higher reciprocal tariff extended (through October). No change to existing tariffs.

- Mexico: 90-day pause on higher reciprocal tariff (through October). No change to existing tariffs.

- Section 232 Tariffs: Investigations into Timber & Lumber (investigation started Mar-2025), Critical Minerals (Apr-2025), Pharmaceuticals (Apr-2025), Semiconductors (Apr-2025), Trucks (Apr-2025), and Aircrafts & Engines (May-2025) are ongoing. No tariffs added.

- Legal Authority: The tariffs Trump imposed under the International Emergency Economic Powers Act (IEEPA), which includes country-specific tariffs related to Fentanyl, immigration and trade-deficits, are being reviewed by a federal appeals court. In a hearing Thursday, media reports suggest judges express skepticism that the IEEPA gives the President such broad authority when it comes to imposing tariffs. It remains to be seen how the case is eventually decided, and these tariffs will remain in effect until a ruling is made, but if they are determined illegal, tariffs paid would be refunded.

We include all of this in our updated Tariff Tracker below, and as always will continue to update it as the details become available. Ultimately once you get past a certain threshold, the rejiggering of rates doesn’t matter all that much at the macro level unless you adjust your major partners: China, Mexico, Canada and the European Union, which together accounted for around 60% of total U.S. imports last year.

As such, we’ll be paying close attention to any adjustments to these partners. Where tariffs settle on China, for example, will be one of the biggest determinants of the average U.S. effective rate and how much revenue is ultimately raised through tariffs due to how much we import from the country. But given how elevated tariffs already are on the country, we expect it has already disincentivized import demand.

Section 232 tariffs also have our attention, though they come with a little more lead time. Unlike tariffs under the IEEPA, sector-level tariffs are implemented with Section 232 of the Trade Expansion Act of 1962, which requires an investigation and public comment period. It also means the legal-authority of these tariffs isn’t currently being debated, meaning firms may be viewing them as more lasting. The investigation for the copper tariffs that went into effect today began in February, providing a six-month lead time. Most other investigations began in April, suggesting a bit more time before we see the results of those investigations. Tariffs on pharmaceutical products are getting a lot of attention given recent comments from Trump that they are coming. Even though the U.S. and the European Union have reached a trade agreement, that doesn’t mean Europe is now safe from additional tariffs and pharmaceuticals in particular would sting given the large amount of product we bring in from the region.

While many economic indicators have revealed only a benign impact from tariffs so far, we have been arguing that the negative impacts of the tariffs are hiding in plain sight. Consumers have cutback on discretionary spending, and the soft July jobs report confirmed the concerns we have been articulating. To the degree that more negative news piles up, there is apt to be growing political pressure to back off from some of the more aggressive aspects of tariff policies.