Sunrise Market Commentary

- Rates: Commodity sell-off could hurt risk sentiment

Risk sentiment deteriorates in Asia this morning with Japan losing up to 2%. Yesterday’s commodity sell-off continues on Asian exchanges and gains traction cross markets. Spillover to Europe could lift core bonds via safe haven flows. Trading was lackluster so far this week with investors unwilling to front run on Friday’s payrolls and next week’s Fed meeting. - Currencies: Risk-off correction to slow further USD gains

The dollar profited slightly from the protracted rise in US ST yields yesterday. Especially EUR/USD drifted gradually lower. However, the US rebound was blocked later in the session by a risk-off correction. This correction continues this morning in Asia. USD/JPY remains vulnerable. The jury is still out, but USD/EUR looks more resilient.

The Sunrise Headlines

- US stock markets ended around 0.4% lower yesterday. Asian risk sentiment deteriorated with Japan losing up to 2%. Asian commodity markets catch up with yesterday’s sell off in mainly industrial metals.

- UK PM May is facing a revolt from inside her Cabinet over her plan to keep UK regulations aligned with the EU after Brexit, a split that threatens to undermine her hopes of breaking the deadlock in negotiations.

- Donald Trump plans to recognise Jerusalem as the capital of Israel and will announce plans to move the US embassy there from Tel Aviv, defying fears among counterparts in the Middle East and elsewhere that such a move would threaten efforts to broker peace.

- Australia’s economy expanded by 0.6% Q/Q in Q3 (vs 0.7% Q/Q expected) thanks to a long-awaited jump in business investment, though marked weakness in household spending cast a cloud over the outlook for growth.

- Chicago Fed Evans questioned whether the Fed is really in a hurry to raise rates. “What if we just decided to wait until the middle of the year and if we saw inflation pick up, then we could do something?”

- BoJ board member Masai advocated sticking with ultra-easy monetary policy due to uncertainty over how fast inflation will rise, while warning that the central bank should remain on guard against the possible side-effects.

- Today’s eco calendar contains US ADP employment and Bank of Canada’s interest rate decision. ECB Mersch is scheduled to speak and Germany taps the market.

Currencies: Risk-Off Correction To Slow Further USD Gains

Risk-off correction to cap further USD gains?

There were few data with market moving potential yesterday. US ST yields rose further, widening the interest rate differential in favour of the dollar. Of late, the dollar often ignored the guidance from interest rate markets, but this time it helped the US currency to some cautious gains. The US non-manufacturing ISM was slightly softer than expected. It didn’t hurt the dollar much, but the US currency lost slightly ground later as equities turned again negative. EUR/USD closed the session at 1.1826. USD/JPY finished at 112.60.

The US equity slide accelerated in Asia overnight. Commodity related stocks are taking the lead in the decline after a sell-off of copper yesterday. Losses on Asian markets vary from about 0.5% (India) to almost 2% (Japan). The equity decline pressures US yields with modest impact on the dollar. USD/JPY dropped to the low 112 area. EUR/USD is less affected and trades in the 1.1840 area. Yesterday, the Aussie dollar profited from positive comments in the RBA statement. Part of the gain was already undone yesterday (copper correction). The reversal continued this morning as Australian Q3 GDP was slightly softer than expected at 0.6% Q/Q and 2.8% Y/Y (0.7% Q/Q and 3.0% Y/Y was expected).

There are few data with market moving potential in Europe or in the US today. The ADP labour market report is the exception to the rule. The consensus expects 190 000 net job growth in the US private sector (from 235 000 in October, probably still affected by the consequences of the hurricanes). We have no reason to take a different view from consensus. The expected job growth remains good, given that the US eco cycle has already advanced quite a long way. Of late, the reaction of the (FX) market to the ADP was mostly modest as the month-on-month correlation with the payrolls is not that tight

The dollar showed a mixed picture last week, rebounding against the yen but holding relatively soft against the euro. This week, there were tentative signs (especially yesterday) that the US currency could get a bit more support from the protracted rise in ST US yields (2-y US yield rising above 1.8%). Markets are gradually moving a bit more in the direction of the Fed guidance (dot-plot). For now, it didn’t help the dollar that much. Even so, it should at least help to put a floor for the US currency as USD shorts are becoming ever more expensive.

Of course, this process might again be aborted if global markets fall prey to an outright risk-off correction. Even so, we have the impression that the topside in EUR/USD is becoming a bit tougher.

We still see no reason for EUR/USD to rise beyond the 1.1961/1.20 area ahead of next week’s Fed meeting, unless there comes high profile negative news from the US. USD/JPY reacted more to interest differentials of late, but the pair might be more vulnerable in case of a risk-off correction.

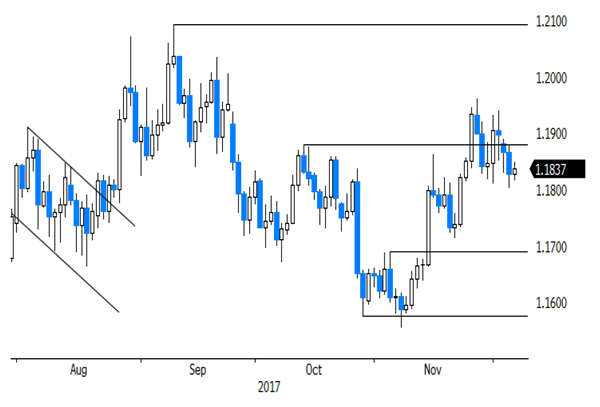

From a technical point of view: EUR/USD set a post-ECB low mid-November, but dollar momentum wasn’t strong enough. EUR/USD regained the 1.1880 MT correction top, opening the way for a full retracement to the 1.2092 top. A return below 1.1713 would signal that the rebound in EUR/USD is aborted. For now, there is no clear technical signal. USD/JPY’s momentum deteriorated early November, dropping below the 111.65 neckline. No aggressive follow-through selling occurred though. Last week the pair succeeded a nice rebound, calling off the downside alert. The pair again hovers in the 110.84/114.73 consolidation range. We amend our ST bias from negative to neutral.

EUR/USD: rally aborted, but no sustained downside correction yet

EUR/GBP

Sterling awaiting less diffuse news from Brexit

Monday’s last minute failure to strike a separation deal on Brexit kept sterling in the defensive yesterday morning. The UK services PMI came out slightly softer than expected at 53.8 from 55.6 (55.00 was expected), but price indictors in the report rose quite sharply. Sterling traded already off the recent lows at the time of the PMI release and regained some further ground late in the session. Markets apparently still hope that a deal can be reach in the near future even if the political signals from the UK remain very diffuse. EUR/GBP closed the session at 0.8797. Cable finished the day at 1.3443, but this move still reflected some USD strength.

There are no important eco data in the UK today. So, Brexit headlines/rumours will continue drive GBP trading. The comments this morning at least suggest that UK PM May has still plenty of work to do to convince hard-line Brexit supporters in her party and to meet the wishes of the DUP. Sterling is slightly in the defensive this morning. Sterling traders remain reluctant to place big directional bets as the Brexit news flow might change minute by minute. An agreement is still possible ahead of next week’s EU summit. However, given recent developments, we don’t add sterling longs at this stage. More erratic trading might be on the cards unless there comes some real clarity on Brexit.

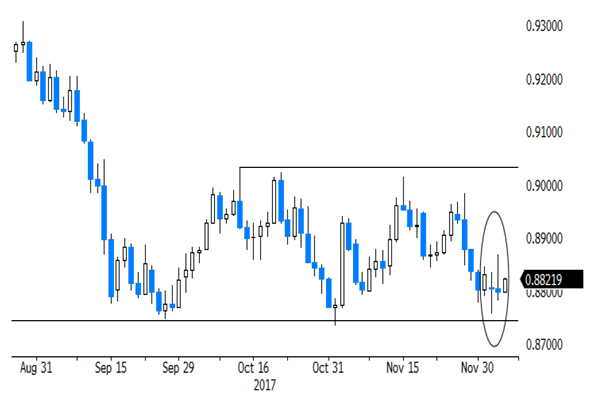

MT view/technical picture: A BoE driven sterling rebound ran into resistance early last month. Sterling declined again as markets anticipated that the rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Brexit headlines cause day-to-day gyrations. We changed our ST bias on EUR/GBP from positive to neutral mid-November. The 0.9015/33 area might be tough to break short-term. In case of more positive news on Brexit, return action to the 0.8733 (or below) level is possible ST.

EUR/GBP: downside test rejected as separation deal is no done thing yet

{kind=link}