{kind=link}

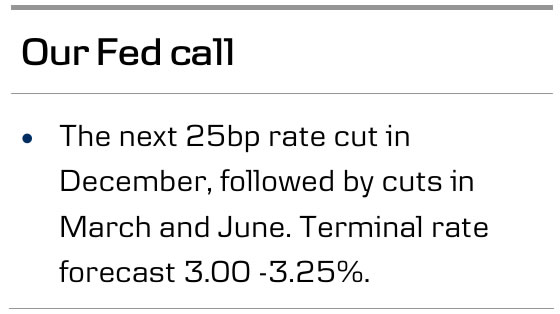

- We expect the Fed to cut its policy rate target by 25bp to 3.50-3.75% next week, in line with consensus and market pricing. We expect an equal reduction to all administered rates, but an additional 5bp cut to the IORB rate is not off the table.

- The Fed could also follow up on its October decision to end QT by announcing the start of organic balance sheet expansion in 2026, which would ease USD liquidity conditions further.

- We expect Powell to verbally push back against continuation of sequential rate cuts in early 2026. Updated dots will likely signal a range of views for 2026 rates outlook, but we expect median long-range dot to remain at 3.00-3.25%.

- Hawkish forward guidance could push UST yields higher and EUR/USD lower on Wednesday, but we maintain our upward sloping 12M EUR/USD forecast at 1.22.

Markets are pricing next week’s 25bp cut to the policy rate target as largely a done deal, but 2026 outlook for both rates and liquidity remains a lot less clear. We expect Powell to push back on expectations of sequential rate cuts continuing in early 2026, echoing the message heard in October and reflecting the widely varying views within the FOMC. Knowingly delivering a ‘hawkish cut’ is a consensus choice.

Even though incoming macro data has not delivered decisive signals since October, we believe that the decline seen in markets’ inflation expectations makes another rate cut more palatable even for the hawks (chart 1). Overall financial conditions have tightened modestly as real short rates have moved higher.

Jeffrey Schmid is likely to repeat his dissent in favour of a hold and could potentially be joined by Susan Collins and/or Alberto Musalem. Chicago Fed’s Austan Goolsbee also prepared markets in November by saying he sees ‘nothing wrong with dissenting’. On the other side, Trump-nominated governors Waller, Bowman and Miran together with NY Fed’s John Williams form the backbone of the dovish camp.

We see a good chance of the Fed pausing its easing cycle in January, as three of the four new 2026 voters – Hammack, Kashkari and Logan – have all vocally opposed the October decision to cut. In our base case, we expect final 25bp cuts in March and June. The updated dots are likely to reflect the growing diversity of views even by the end of 2026. Macroeconomic forecasts will see more cosmetic changes; we expect a small positive revision to 2026 GDP forecast while inflation outlook will likely remain mostly unchanged.

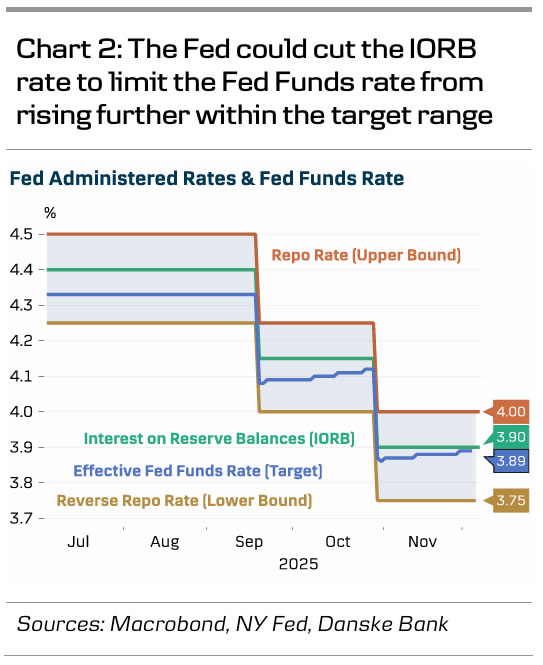

The Fed formally ended its balance sheet drawdown at the start of December, but liquidity conditions remain on the tighter side. The effective Fed Funds rate has risen modestly within the target range, and SOFR traded above the upper bound around month-end. While liquidity is not an imminent concern in our view, the Fed could pre-announce organic balance sheet expansion, or gradual QE, starting in 2026. Alternatively, the Fed could lower the interest rate of reserve balances (IORB) by additional 5bp to limit the Fed Funds rate from rising further, though we see the former more likely than the latter.