{kind=link}

- ECB decided to leave its key policy rates unchanged with the deposit facility rate at 2.00% as widely expected by markets and consensus.

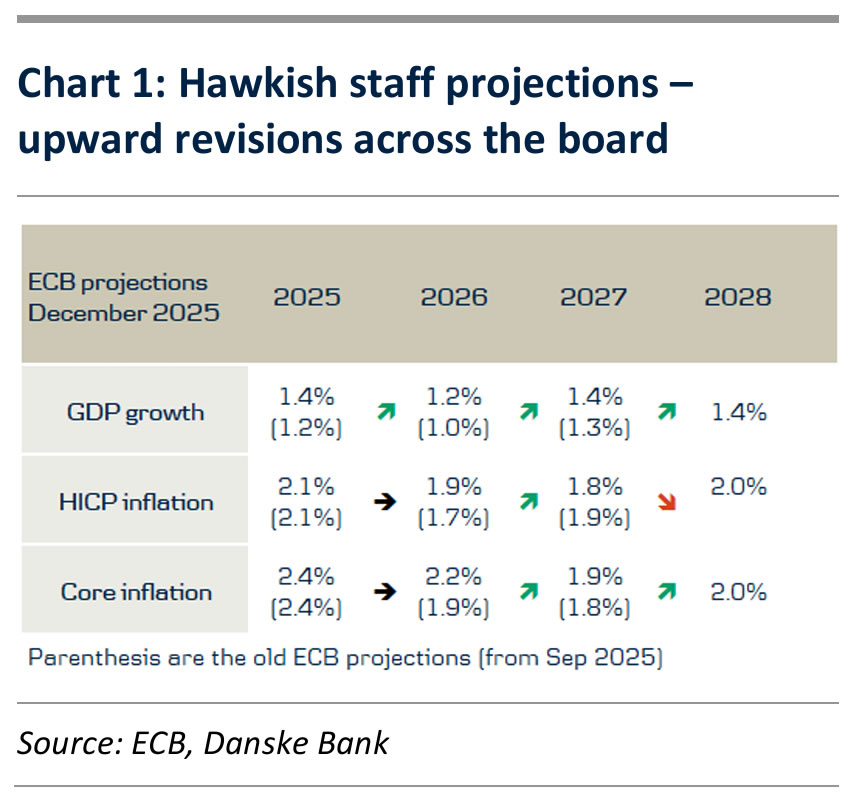

- The new staff projections delivered a hawkish surprise for markets with upward revisions to growth over the entire horizon and to inflation in 2026. However, the moves faded during the press conference as Lagarde’s “meeting by meeting” approach and lack of guidance did not reaffirm Schnabel’s hawkish views.

- We maintain our call that the ECB will leave the deposit rate unchanged at 2.00% throughout both 2026 and 2027.

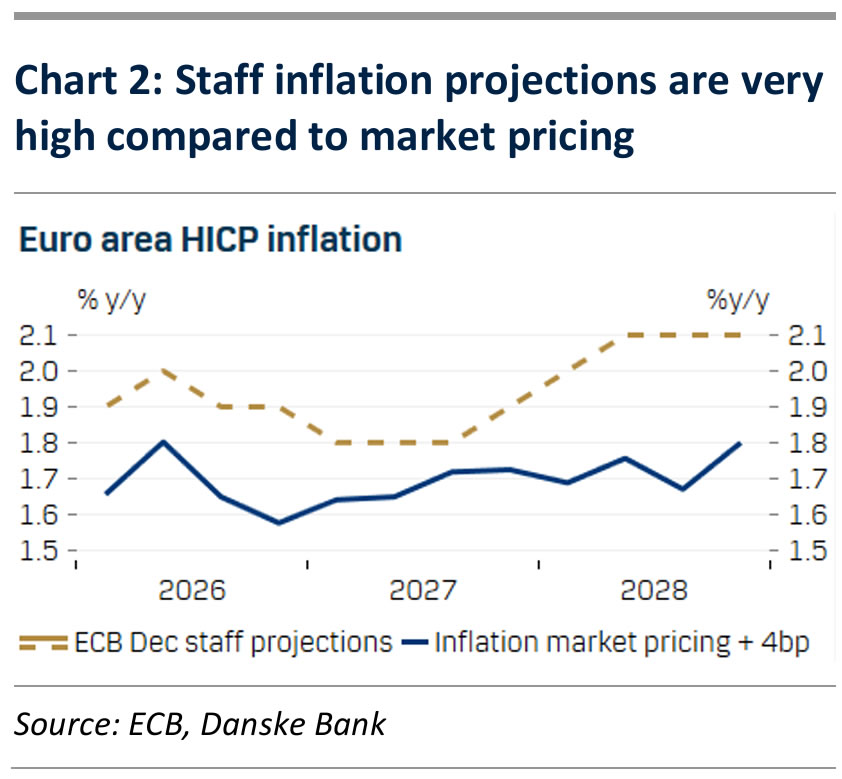

As widely expected, the ECB decided to keep its policy rates unchanged at today’s meeting, leaving the deposit rate at 2.00%. The new staff projections delivered a hawkish surprise for markets with upward revisions to growth over the entire horizon and to inflation in 2026 (see chart 1). The GDP forecast for 2026 was revised up to 1.2% y/y (from 1.0%) and to 1.4% y/y in 2027 (from: 1.3%). Headline inflation was revised up to 2.2% y/y (from: 1.9%) in 2026 and core inflation to 2.2% y/y (from: 1.9%). Markets reacted by sending front-end rates higher and EUR/USD rose on the hawkish staff projections. We note that the inflation projections are on the high side compared to our own, market pricing, and consensus expectations (see chart 2). Hence, we think there is a good chance that the ECB would end up disappointed on inflation in 2026, which should reduce expectations for hikes. While we think the forecasts are optimistic, the staff projections do nevertheless cement the view in the ECBs that they are in a good place with no need for imminent rate cuts.

During the press conference Lagarde was asked whether it was more likely that the next move would be a hike relative to a cut, referencing Schnabel’s recent interview. Lagarde did not answer the question directly and instead said that the consensus in the ECB was that all options remained open and that they stick to a meeting-by-meeting approach. In our view, this highlights that the consensus in the Governing Council is clearly less hawkish compared to Schnabel especially due to diverging views on the inflation outlook. At the same time, Lagarde also said that she would not give forward guidance by commenting on market pricing given that uncertainty is still very high. The fact that she is referring to high uncertainty implies that staff projections play a smaller role in deciding current policy changes like we saw in September. Lagarde’s descriptive comments on the economy and decision not to agree with Schnabel’s view led to a fading of the initial rise in rates following the hawkish staff projections. Hence rates ended the meeting flat and EUR/USD little changed as we expected.

We maintain our call that the ECB will leave the deposit rate unchanged at 2.00% throughout both 2026 and 2027. Higher than expected activity and wage growth has reduced the need for cuts in 2026 while our expectations of a clear undershooting of inflation the comings years should keep the ECB from hiking in 2027. We have liked our paying bias the past months also supported by recent data. While we cannot exclude that rates can continue to move slightly higher in the very near-term, we are increasingly attentive to the risk-reward skew on a 1–3-month basis to start to favour receivers.