{kind=link}

Summary

The FOMC is widely expected to leave the fed funds rate unchanged at its January meeting. There will be no update to the SEP at this meeting, and we expect the post-meeting statement and press conference to signal maximum flexibility as the Committee strives to keep its options open. Our forecast remains for two 25 bps rate cuts at the March and June meetings, but the risks to our forecast look increasingly skewed toward later and possibly less easing this year. In fact, given our view on how economic growth will evolve this year, there is a sound argument that the longer the FOMC waits to cut, the higher the hurdle becomes to justify on economic grounds the need to ease further.

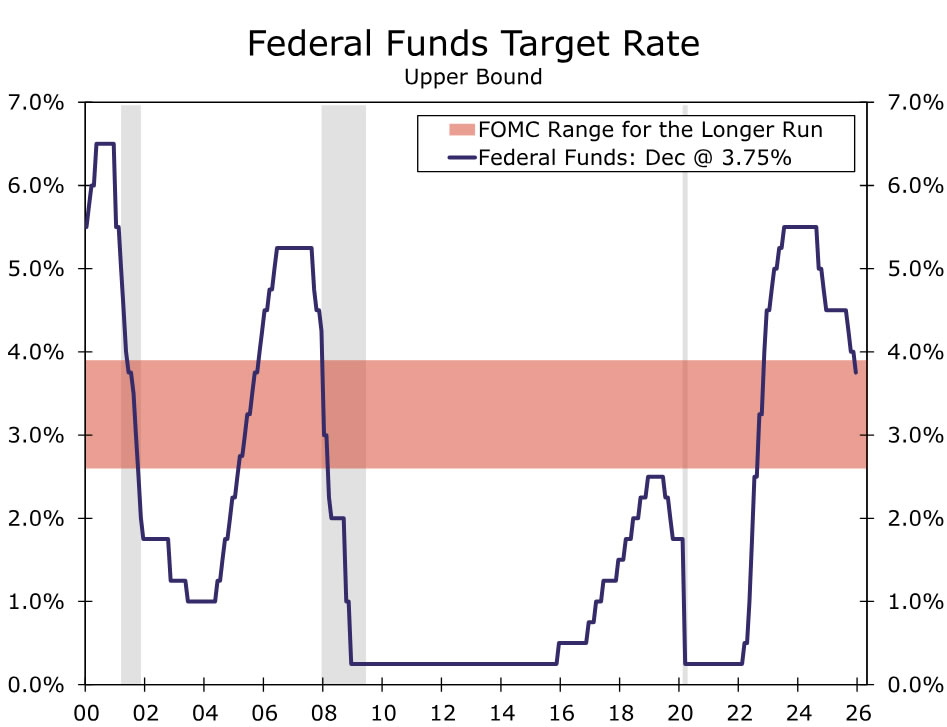

We anticipate the FOMC will leave its policy rate unchanged at 3.50%-3.75% on January 28. The FOMC’s prior meeting in December concluded with the Committee’s third consecutive 25 bps cut. In a relatively close decision—the dot plot revealed six policymakers would have preferred to hold the policy rate steady—the FOMC also signaled the bar for additional easing would be higher going forward.

The higher bar for additional easing comes as the fed funds rate is now back in the vicinity of neutral, i.e., the policy rate that is neither restrictive nor accommodative (Figure 1). Disagreement over the neutral rate is one key factor driving divergent views on the FOMC about the appropriate path of policy.

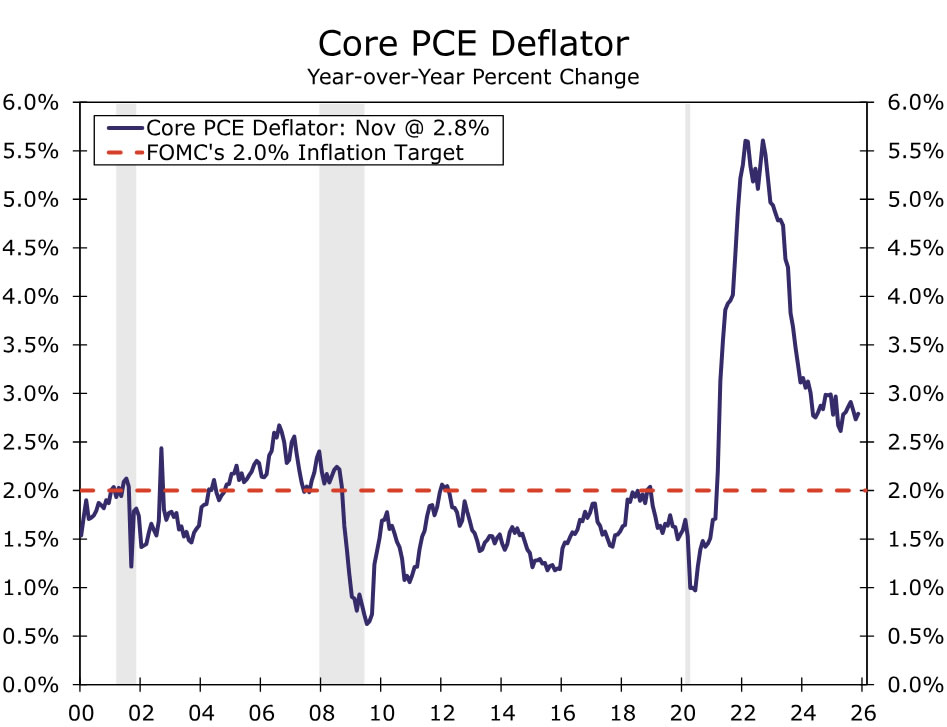

Another point of disagreement is how to weigh the balance of risks with inflation still above target and unemployment slightly above most estimates of full employment (Figures 2 & 3). At 4.4%, the latest unemployment rate is unchanged from when the FOMC last met. The inflation picture looks modestly improved even accounting for shutdown-related quirks. We estimate core PCE inflation was 3.0% yr./yr. in December, the same as December 2024 despite the lift to goods prices from tariffs last year.

There will be no updated Summary of Economic Projections, but we expect the statement to reflect the more stable balance of risks to the dual mandate. For example, it could remove the line that the FOMC “judges that downside risks to employment rose in recent months” and the reference to “the shift in the balance of risks” when discussing its policy decision. We also see the possibility for the statement to no longer say that “inflation has moved up since earlier in the year” when discussing recent economic conditions, and merely maintain that it “remains somewhat elevated.”

The post-meeting communications are also likely to emphasize the cumulative amount of easing undertaken over prior meetings that allows for any additional policy changes to be made more slowly. We do not expect Chair Powell to hint in the press conference that further easing is likely to come at the FOMC’s next meeting on March 18 given the range of participants’ views and the desire to keep options open. It is likely that Chair Powell will be asked about the DoJ’s investigation, but we expect him to respond that he has already said what he has to say on the matter.

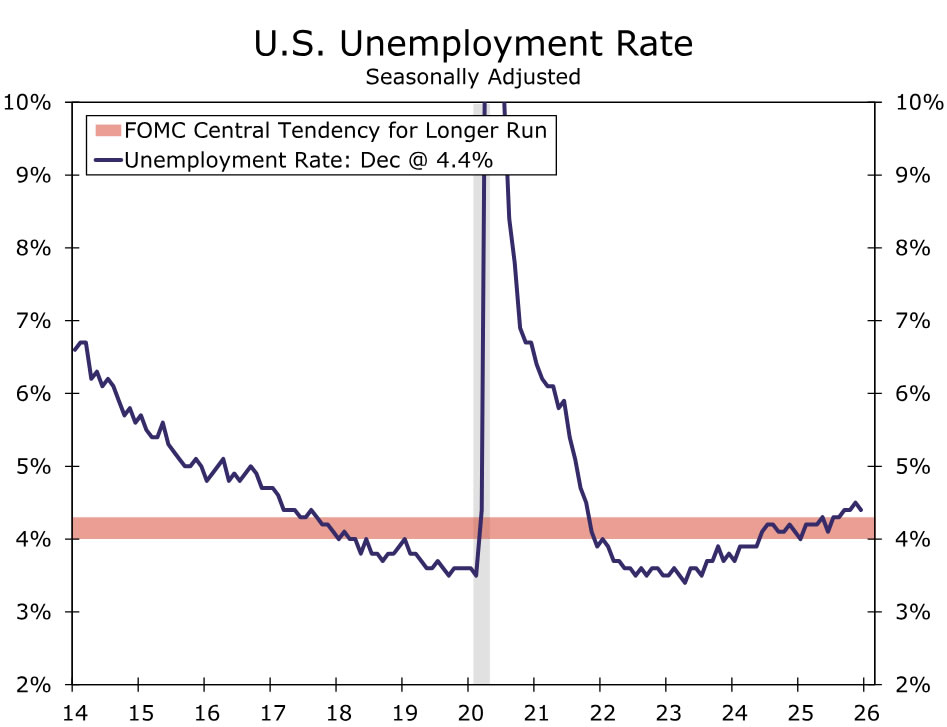

Since September, our forecast has been for the FOMC to reduce the policy rate to 3.00%-3.25% in 2026, with two 25 bps cuts in March and June. With two more months of employment and inflation data released before the March meeting, we are not changing that assumption at this time. That said, the risks to our call look increasingly skewed toward later and possibly less easing this year. Our latest forecast looks for underlying growth to firm over the spring and summer as fiscal support and prior monetary policy easing bolster economic activity and help the labor market stabilize (Figure 4). That will leave a narrow window for the Committee to ease further this year.