- We expect the Federal Reserve to keep its monetary policy unchanged at the March meeting, in line with consensus and market pricing.

- Powell will avoid giving firm forward guidance regarding the Fed’s reaction to the war in Iran. Stronger USD and tighter financial conditions are partially compensating for the inflationary effect from higher energy prices.

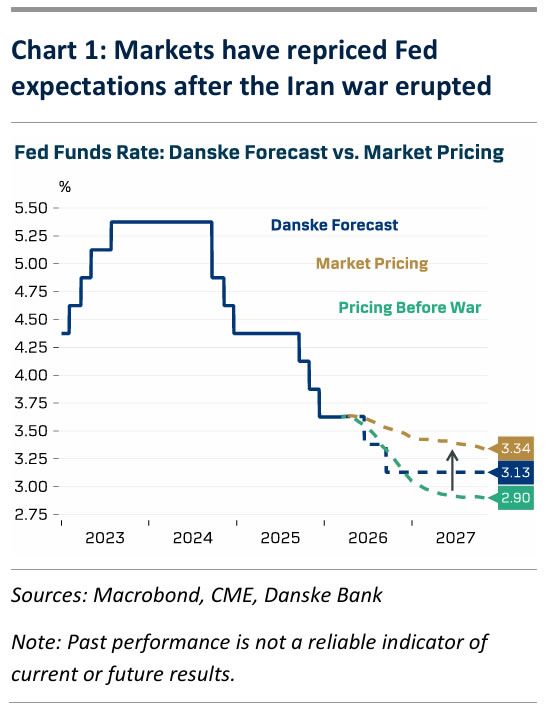

- Solid macro allows the Fed to hold a steady hand for as long as the energy supply uncertainty persists. Further out, we still expect the Fed to cut rates twice this year. We expect only a muted market reaction to this week’s meeting.

FOMC participants had a few days to discuss the war in Iran before the March blackout begun, and the message heard from both hawks and doves was noticeably uniform. Hammack, Miran and Kashkari said it is ‘too early’ to judge the impact on the economy, while Williams, Barkin, Waller and Daly all underscored that they need more time to evaluate the implications for monetary policy.

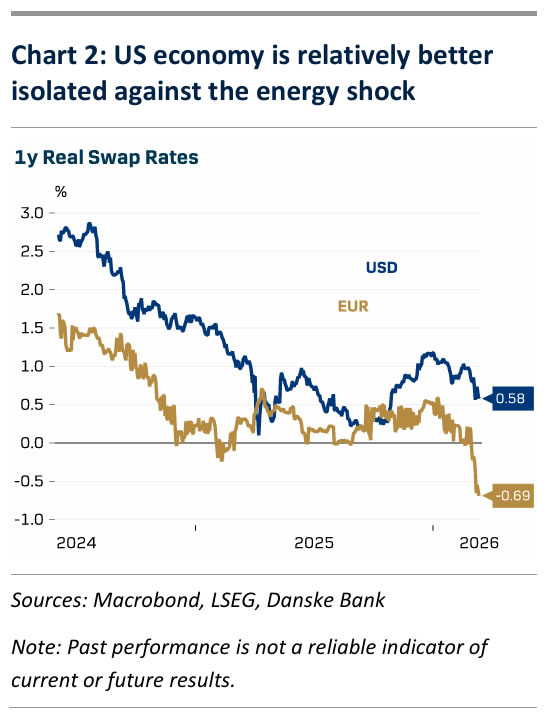

And we would agree. The Fed is not under pressure to make quick policy changes, as the US economy remains relatively well insulated against the energy shock. US Henry Hub natural gas prices have hardly moved during the war whilst European natural gas and global LNG benchmarks are up almost 50% m/m. A stronger USD has partially shielded the American consumer against rising oil prices, while tighter financial conditions constrain demand. US short-end inflation expectations have risen and real rates are down, but relatively much less so than the EUR equivalents.

Powell will carefully avoid giving any strong forward-looking signals and emphasize the two-sided nature of the risks stemming from the energy supply shock. Most FOMC participants still see the current policy rate level somewhat above neutral, and once the energy uncertainty eases, we expect the Fed to eventually deliver two more rate cuts in June and September. Extending uncertainty could push the expected cuts further out into the future but not erase them completely, which we expect to be reflected also in the updated dots.

Rising energy costs will weigh on households’ disposable income, which is already under pressure amid cooling labour markets. But for now, the relatively solid labour market data should assure the Fed that downside risks to growth remain contained. 2026 GDP forecasts will likely be revised marginally lower from December after the weak Q4 reading. Inflation forecasts could be revised higher, but we would not put too much emphasis on them at this stage given the sensitivity to the assumptions made about the persistence of the energy shock.

We expect no changes to the Fed’s balance sheet operations either. The reserve management purchases of T-bills are likely to continue until the April tax date in line with earlier guidance. After mid-April, normalizing tax revenue inflow and the likely beginning of tariff refunds will ease USD liquidity conditions, allowing the Fed to decrease the T-bill purchase amounts substantially.

{kind=link}