Key Takeaways

- US inflation accelerated sharply in April, with headline CPI rising to 3.8% y/y and core CPI to 2.8% y/y, reinforcing the “higher-for-longer” Federal Reserve narrative and effectively eliminating expectations for rate cuts in 2026.

- Semiconductor stocks led a broad technology pullback after an extended rally, with the Philadelphia Semiconductor Index falling 3% as major chip names, including Qualcomm and Intel, experienced aggressive profit-taking.

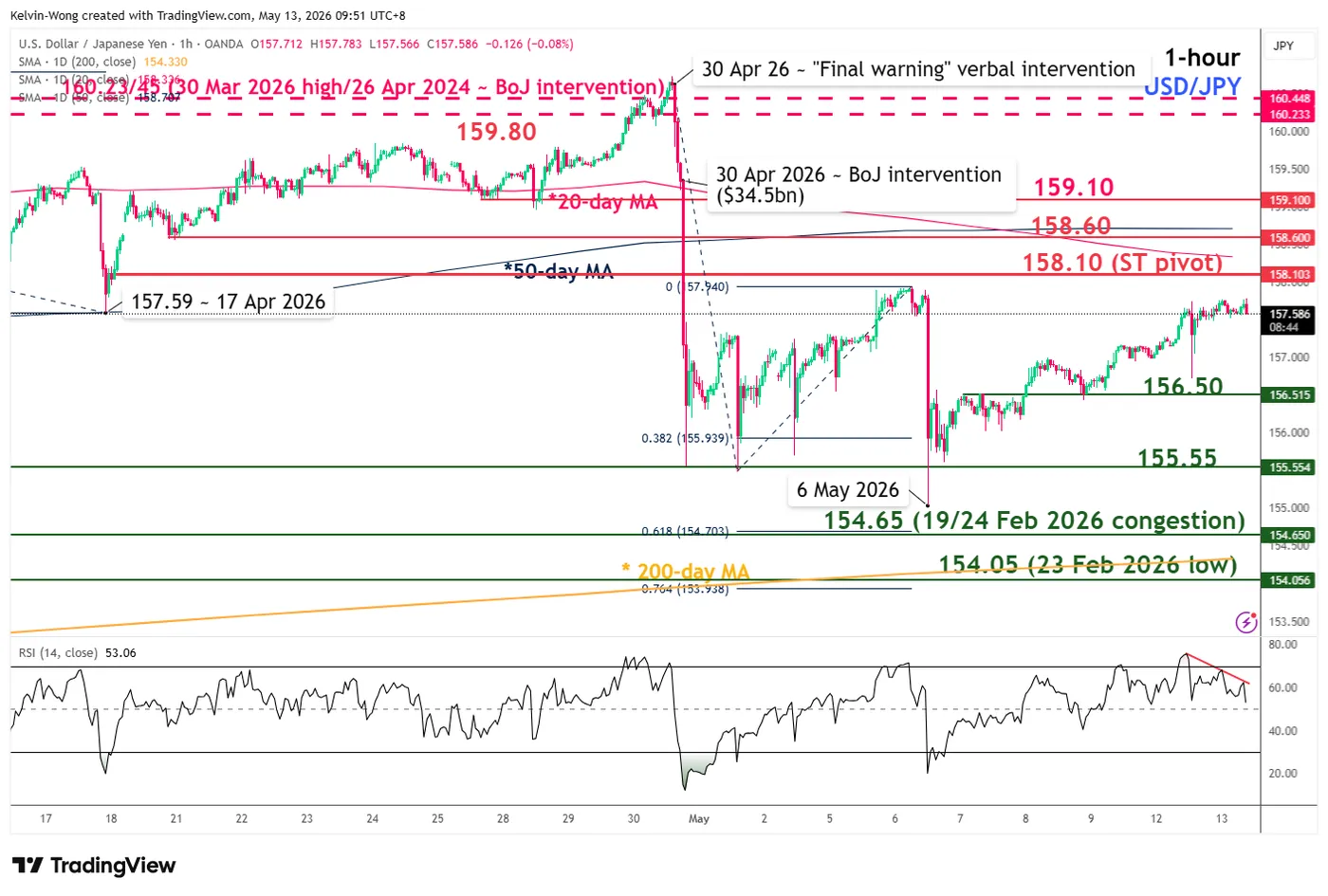

- Chart of the day: USD/JPY climbed toward the key 157.90 intervention risk zone as rising US yields strengthened the US Dollar, although bearish RSI divergence now signals growing short-term upside exhaustion risks.

Top Macro Headlines

- US consumer prices jump further: Headline annual US CPI inflation rose to 3.8% y/y in April, higher than expected and the highest in three years. This means real wage growth has turned negative for the first time since 2023. Core inflation also jumped to 2.8% y/y, its steepest rise since September 2025.

- Iran peace deal on “life support”: Hopes for a Middle East peace resolution are fading rapidly after US President Donald Trump stated the US-Iran ceasefire is on “life support,” sending oil prices sharply higher.

- Semiconductor sector sells off: A 70% rally over the past six weeks in chip stocks unraveled, with the Philadelphia Semiconductor Index falling 3%. Market darlings like Qualcomm, down 11.5%, and Intel, down 7%, dragged down the broader tech sector.

- US and Japan address FX volatility: Amid a surging US Dollar, US and Japanese officials, including Bessent, agreed that excess foreign exchange volatility is undesirable.

- Anthropic share transfer rules raise doubts: AI giant Anthropic updated rules surrounding the buying and transfer of its shares, raising doubts about ownership rights ahead of its highly anticipated IPO.

Key Macro Themes

- Fed rate cut bets wiped out: The historic energy shock and 3.8% CPI print have completely wiped out market expectations for Federal Reserve interest rate cuts this year. If the Fed does move, current pricing from the CME FedWatch tool shows it will be to tighten.

- Political pressures stoke global yields: Wary that a successor to UK leader Keir Starmer may increase borrowing, long-term UK bond yields have surged to their highest levels since 1998. This complements rising yields in the US due to inflation fears.

- Potential froth coming off the AI rally: The sharp decline in semiconductors suggests investors are taking profits from an overheated sector, exacerbated by wild volatility in Asian tech markets and rising long-term borrowing costs.

Global Market Impact

Equities: The S&P 500 fell 0.2%, and the Nasdaq 100 dropped 0.9%, dragged down by semiconductor stocks. The Dow inched higher by only 0.1%. Europe closed in the red. US healthcare was a bright spot, gaining 2% with UnitedHealth up 3%.

Fixed Income: US Treasury yields surged 5 bps across the curve, reacting to inflation data and a soft 10-year note auction characterized by a low bid/cover ratio. UK 30-year yields hit highs not seen since 1998.

FX: The US Dollar rose broadly as rate cut expectations evaporated. Sterling fell 0.5%, becoming the biggest decliner among major currencies amid UK political uncertainty.

Commodities: Oil prices rebounded aggressively on fading ceasefire hopes, with WTI surging 4% to move back above the critical $100/bbl level. Brent rallied by 3% to close at $107.70/bbl.

Asia Pacific Impact

- Stock markets: Japan managed to end higher on Tuesday, 12 May, but Asia ex-Japan broadly declined. South Korea’s KOSPI ended down 2% after a wild rollercoaster ride, setting the tone for the global semiconductor sell-off.

- Currencies: The South Korean Won slumped 1% against the surging US Dollar, reflecting vulnerability to the global energy shock and risk-off sentiment.

- Economic outlook: Focus shifts heavily to the upcoming Trump-Xi Beijing summit. Investors are seeking clarity on AI policies and broader trade relations as inflation risks mount globally.

Top 4 Economic Data/Events to Watch Today

- AU Westpac Consumer Confidence (May) – 9.30 am SGT Impact: AUD/USD, AUD crosses, ASX 200

- Eurozone Q1 GDP Flash and Industrial Production (Mar) – 5.00 pm SGT Impact: EUR/USD, EUR crosses, DAX

- US Producer Price Inflation (Apr) – 8.30 pm SGT; consensus: 4.9% y/y, Mar: 4.0% y/y Impact: US Treasuries, USD, US stock indices

- Asian Earnings Heavyweights: Tencent, Alibaba, Nissan, SoftBank Impact: Hang Seng Index, Nikkei 225, global tech stocks

Chart of the Day: USD/JPY Squeezed Up to Intervention Risk Level of 157.90

Fig. 1: USD/JPY minor trend as of 13 May 2026. Source: TradingView.

The recent four-day rebound of 1.8% in USD/JPY, from the 6 May 2026 low of 155.03, has reached the prior Japanese authorities’ “stealth intervention” level of 157.90.

In addition, short-term momentum has turned bearish, as the hourly RSI momentum indicator flashed a bearish divergence condition at its overbought region on Tuesday, 12 May, in the US session.

Watch the 158.10 key short-term pivotal resistance. A break below 156.50 may see a further potential drop to retest the next intermediate supports at 155.55 and 154.65.

However, a clearance with an hourly close above 158.10 negates the bearish scenario for a further squeeze up to see the next intermediate resistances coming in at 158.60, also the 50-day moving average, and 159.10.

{kind=link}