Sunrise Market Commentary

- Rates: Sentiment-driven trading ahead of payrolls?

We expect trading to be subdued and sentiment-driven today ahead of tomorrow’s US payrolls report. Ongoing strength on stock and oil markets might weigh on core bonds. The US Note future closes in on the contract low, but higher earnings/inflation readings will probably be necessary to trigger a break. - Currencies: Dollar bottoms going into tomorrow’s key US payrolls

The recent USD decline slowed yesterday. Technical considerations (EUR/USD coming close to the cycle top) and strong US eco data helped to put a floor for the dollar. We expect the dollar to hold a wait-and-see mode today. Sterling tried to change fortunes at the first day of the year, but failed to sustain that constructive momentum.

The Sunrise Headlines

- US stock markets extended their record race, eking out gains between +0.4% and +0.84%. Asian risk sentiment is positive as well with Japan outperforming on their first trading day of the new year in a catch-up move.

- FOMC Minutes showed that Fed members wrestled with how much of an economic impact to expect from Donald Trump’s tax cuts as they raised rates last month and continued to be flummoxed by persistent low inflation.

- China’s services sector activity expanded at its fastest pace in over three years in December on solid growth in new business, with the outlook improving to a six-month high, the Caixin Chinese services PMI showed (rise to 53.9).

- UK PM May believes Barnier is bluffing when he says there will be no special deal for financial services, officials said, as the UK prepares to negotiate its post-Brexit ties with the EU.

- Chancellor Merkel’s Christian Democrat-led bloc and its prospective coalition partner, the SPD, said the chances of a successful conclusion to their exploratory talks have improved after a meeting in Berlin yesterday.

- The US auto industry suffered its first annual sales decline since the financial crisis eight years ago, but a streak of strong profits is expected to overshadow a slowdown in dealership traffic.

- Today’s eco calendar contains services PMI’s in the UK and EMU (final), US ADP employment and weekly jobless claims. Spain and France tap the market while Fed Bullard is scheduled to speak

Currencies: Dollar Bottoms Going Into Tomorrow’s Key US Payrolls

Dollar decline slows ahead of the payrolls

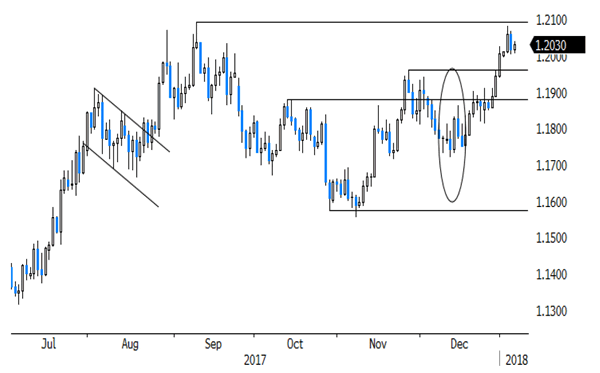

The dollar’s slide slowed yesterday. The US currency regained modest ground against the euro as interest rate differentials widened again slightly. US data (auto sales & Manufacturing ISM) were better than expected, adding to USD constructive sentiment. The Fed minutes revealed different views on persistent low inflation and on the Fed’s policy approach, but a majority of governors supports gradual normalisation. EUR/USD closed the day at 1.2010, off Tuesdays top of 1.2081. USD/JPY bottomed, finishing the day at 112.51.

The risk rally continues in Asia overnight, but the dollar holds near yesterday’s closing. EMU services PMI’s are expected to confirm strong readings from the preliminary report today. US ADP private job creation is expected at a solid 190 000. US jobless claims are expected marginally higher. US data will likely be OK, but won’t change the broader picture ahead of tomorrow’s US payrolls. Risk sentiment stays constructive, but is less supportive for the dollar than it was in the past. The USD might stabilize off recent lows ahead of the payrolls. Recently, the greenback suffered as the global recovery could force other major CB’s (including ECB) to join policy normalisation. Still, we maintain the working hypothesis that it won’t be that easy for EUR/USD to set a new cycle high without really important news. US payrolls and especially wage growth will be key for the next directional USD move.

Global picture USD: The Dec Fed & ECB meetings didn’t bring clear directional guidance for EUR/USD. A narrowing in the (LT) interest rate differential finally drove EUR/USD to the topside of the 1.1554/1.2090 range. A break would improve the ST picture. We don’t preposition for such a break, yet. Quite some good news on the euro/bad news on the dollar should be discounted. Price data remain in focus.

Sterling yesterday failed to hold a tentative improvement from the first day of the year. In order-driven trade, GBP lost ground against the euro and the dollar. Today’s UK services PMI is expected marginally stronger at 54.0. Brexit noise might resurface as negotiators prepare next steps. EUR/GBP showed a consolidation pattern of late. We don’t see a trigger for a big GBP comeback. A EUR/GBP rebound above 0.89 might reinforce the euro positive/sterling negative momentum. Recent UK data were mixed. We don’t expect the BoE to raise interest rates soon. The EUR/GBP 0.8700/60 support looks solid. Ongoing euro strength or soft UK data might keep EUR/GBP 0.90 on the radar further down the road. We keep a EUR/GBP buy-on-dips in case of return action to 0.87.

EUR/USD topside test rejected