Friday January 5: Five things the markets are talking about

After a positive week of global economic data boosted markets, investor focus now turns to today’s U.S. jobs release (8:30 am EDT) as the next key economic barometer.

The ‘mighty’ greenback, which had been battered and bruised throughout 2017 – U.S dollar index lost just under -10% against G10 currency pairs – requires today a much-stronger-than-expected December non-farm payroll (NFP) headline print to garner much needed support.

Note: The market is not expecting any changes to the U.S jobless rate (+4.1%), and a healthy headline print of +180k new non-farm jobs last month, with average hourly earnings set to rise +0.3% on the month.

However, a stronger reading may not even be the answer. Market consensus ahead of yesterday’s ADP reading was for an increase of +193k, but the payroll firm’s report put growth at +250k. That reading was incapable of pushing up U.S Treasury yields further yesterday or even encourage the U.S dollar "bulls" to add to their positions.

Canada is also reporting its labor market data this morning (8:30 am EDT). Of late, the headline print has been surprisingly strong (+2K expected and +6% unemployment rate).

1. Global stocks print new records

In Japan, the Nikkei share average extended Thursday’s gains overnight, probing a three-decade high as banking and brokerage firms rose. The Nikkei was up +0.9%, while the broader Topix closed +0.8% higher.

Note: In the holiday-shortened week, the Nikkei has risen +4.2% since opening on Thursday.

Down-under, Aussie shares ended higher on Friday, hitting a fresh decade-peak and completing its first weekly session of gains in the New Year. The S&P/ASX 200 index rose +0.7%. In Korea, the Kospi closed out on a winning note, up +0.4%, as the KRW traded at a three month high due to equity flows.

In Hong Kong, equities were up for their ninth-day and closed atop of their ten-year high. At close of trade, the Hang Seng index was up +0.25%, while the Hang Seng China Enterprises index rose +0.07%.

In China, both major benchmark indexes climbed for a sixth straight session, helped by gains for property developers. The Shanghai Composite index was up +0.2%, a six-week high, while the blue-chip CSI300 index was up +0.25%.

In Europe, regional indices continue to trade higher following strong gains yesterday with the FTSE100 making new all time highs. This morning, the DAX leads the gainers, rising +1% on the back of record closes on Wall Street overnight, where the Dow crossed +25K for the first time.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 +0.6% at 395.9, FTSE +0.3% at 7717, DAX +1.0% at 13300, CAC-40 +0.7% at 5453, IBEX-35 +0.5% at 10369, FTSE MIB 0.8% at 22681 , SMI +0.4% at 9551, S&P 500 Futures +0.2%

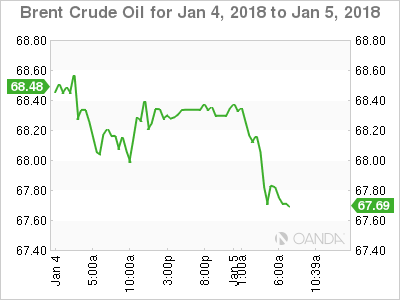

2. Oil slips from 2-year high on rally doubts, gold prices fall

Ahead of the U.S open, crude oil prices fell, dropping away from its two-year-highs, as soaring U.S production undermines its +10% rally from the low print in early December that was driven by tightening supply and political tensions in OPEC member Iran.

Brent crude futures are at +$67.88 a barrel, down -19c, or -0.3% below Thursday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$61.81 a barrel. That is -20c or -0.3% below the last close.

Note: Oil prices have received general support from production cuts led by OPEC and by Russia, which started in January 2017 and are set to last through 2018, as well as from strong economic growth and financial markets.

The current momentum, which is also being supported by a record cold spell along the east cost of the U.S, suggests that further upside is on the cards, however, higher prices continues to attract higher U.S shale production, which is a threat to the ‘bull’ market.

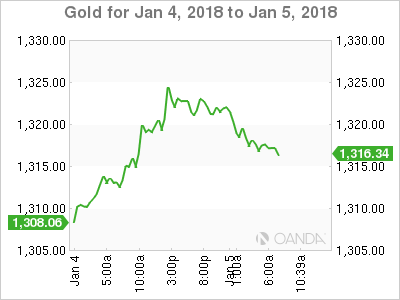

Gold prices have dipped (-0.4% to +$1,317.10 an ounce) ahead of non-farm payrolls (NFP), but the precious metal is set for a month of gains.

3. U.S yields require NFP support

Investors expect more central banks around the world to begin unwinding nearly a decade of stimulus policies in 2018.

These higher global sovereign yields are likely to make the USD less attractive to some investors and any gradual shift in capital flows from the U.S to the eurozone and/or other rising economies will continue to weigh on the dollar in coming months.

Investors are also looking for signs in today’s U.S Payrolls that an economic recovery is pushing up wages would bolster the case for the Fed to raise rates more aggressively this year and set up a potential dollar rebound.

Currently, the fixed income market is now pricing in a +68% chance of a Fed March hike and two more hikes for 2018. Any sign of inflation and these odds will tighten and should support the USD.

Overnight, the yield on U.S 10’s has increased less than +1 bps to +2.45%. In Germany, the 10-year Bund yield fell -1 bps to +0.43%. In the U.K, the 10-year Gilt yield has decreased -1 bps to +1.222%.

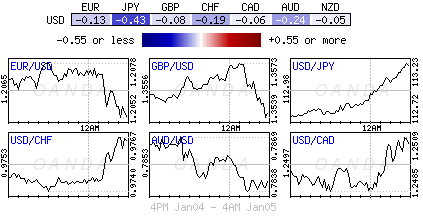

4. U.S dollar seeks guidance from non-farm payroll (NFP)

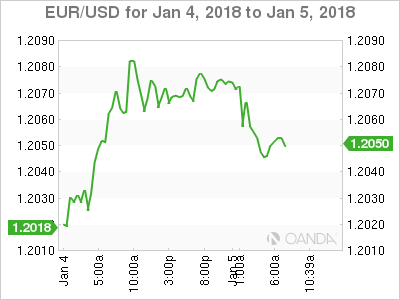

The USD (€1.2050, £1.3541, ¥113.34) remains on relatively soft footing ahead of today’s U.S December jobs report. Dollar ‘bears’ believe the greenback would likely stay under selling pressure if wages component does not show any sign of pick-up.

Note: The current global recovery has everything apart from wage growth (inflation), and this in turn is keeping the Fed rate hikes gradual and currency volatility relatively ‘low.’

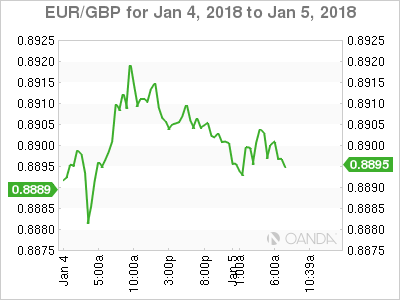

The EUR/USD (€1.2050) has managed to back away from its recent three-month high print Thursday and has yet to tackle the psychological €1.21 level with any gusto. Even slightly weaker-than-expected December eurozone inflation figures this morning (see below) has thus far failed to upset the ‘single’ unit.

Note: The EUR had benefited in recent weeks from market reassessment on the ECB policy rate outlook. Markets currently are pricing the first full +25 bps move in Eonia by mid-October 2019, compared to Q1 2020 as seen in early December.

5. Eurozone inflation disappoints

Eurostat data this morning showed that Eurozone inflation fell in December and was in line with market expectations.

Consumer prices eased from their November print last month. The headline print was +1.4% higher than a year earlier versus Novembers +1.5% headline.

Consensus believes that this morning’s print is likely to mark the start of a series of declines in the inflation rate in early 2018 as a result of base effects linked to energy prices. Nevertheless, the ECB does expect the inflation rate to pick up again in the latter half of this year.

However, of greater concern for Euro policy makers is the weakness of core inflation. The market had expected to see a rise to +1.0%, but the measure remained at +0.9% for the third consecutive month, exactly where it was in December 2016, when the eurozone economy was on the brink of what appears to have been its best year since 2007.