Sunrise Market Commentary

- Rates: More consolidation near sell-off lows?

Today’s eco calendar probably won’t shift trading dynamics in a profound way. German and US yields remain close to, but below, key resistance levels. In Europe, we don’t expect a break ahead of the SPD party convention this weekend and the ECB meeting next week. Cautiousness in the US might be warranted with a potential government shutdown looming. - Currencies: Dollar holds close to recent lows. Decline to slow?

The trends of a stronger euro/decline of the dollar slowed yesterday, but there was no clear sign of a trend reversal. The dollar touched new ST lows against most other majors this morning, but rebounded later. A tentative sign that the recent USD decline has gone far enough?

The Sunrise Headlines

- US stock markets ended 0.3% to 0.5% lower with Dow Jones (flat) outperforming. Most Asian stock markets record similar losses overnight.

- The ECB must keep an eye on the euro exchange rate because of the downward pressure it puts on inflation, governing council member Villeroy de Galhau said.

- In several Chinese megacities, home sales have stalled and prices have dropped. Demand has dried up in as a result of measures like higher mortgage rates, higher down-payment requirements and limits on buying a 2nd or 3rd home.

- German Bundesbank president Weidmann said that analysts’ expectations that ECB interest rates won’t rise before the middle of next year are reasonable.

- US Senators worked to salvage a bipartisan plan to protect ‘Dreamers’—young undocumented immigrants brought to the US by their parents—as the divide grew over an immigration deal key to avoiding a government shutdown.

- Czech prime minister Babis has failed in his first attempt to win parliamentary backing for his minority government, prolonging a period of political uncertainty in one of Europe’s fastest-growing economies.

- Today’s eco calendar contains UK December industrial production and final EMU CPI. The BoC is expected to hike rates from 1% to 1.25%. Germany taps the market and ECB Nowotny, Fed Mestern, Evans and Kaplan speak. The Fed releases its Beige Book. Goldman, BoA and Alcoa bring Q4 earnings

Currencies: Dollar Holds Close To Recent Lows. Decline To Slow?

Dollar holds near correction lows

The trends of euro strength and USD weakness slowed yesterday, but there was no real trend reversal yet. The euro declined on growing opposition within the German SPD to start formal coalition talks and on headlines that the ECB won’t change guidance at next week’s meeting. Later in US dealings, the USD struggled again as stocks corrected off record levels. US long term yields eased and the dollar reversed most intraday gains. EUR/USD closed little changed at 1.2260. USD/JPY finished slightly off the intraday low (110.45).

Yesterday’s reversal of risk sentiment in the US also weighs on Asian markets. The dollar hit new short-term lows against most majors early this morning, but regained its composure later as equity selling slowed and as core (US) yields turned north again. EUR/USD filled offers above 1.23, but trades again in the mid 1.22 area. USD/JPY rebounds off the 110.20 area (currently 110.85). AUD/USD came close to the 0.80 barrier. The Aussie dollar was supported by strong consumer confidence data, but also eased later in the session on the overall USD rebound.

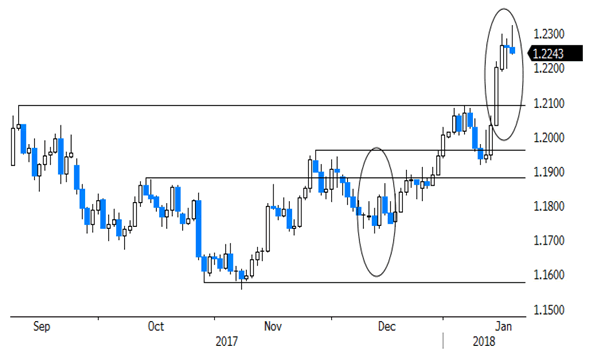

Today’s eco calendar contains final EMU Dec CPI, US production and NAHB housing confidence. The Beige Book preparing the January 31 Fed meeting will be published and several central bankers speak. ECB’s Villeroy mentioned the rise of the euro as a source of uncertainty. Is there more to come on this theme? Fed speak and the Beige Book might confirm that recent developments allow further Fed normalisation. Global sentiment on risk is a wildcard for FX trading. More risk-off probably won’t help the dollar. Global Picture. Euro strength prevails as markets prepare for a change in policy from central banks outside the US. Especially the ECB is signalling a gradual turn. Looking at the fundamentals/interest rate differentials (2-y US/German spread at +250 bps), the euro rise/dollar decline has gone quite far. However, there is no trigger for a ST change in sentiment. The technicals turned USD negative as EUR/USD cleared 1.2090/1.2167 resistance. 1.2598 (62% Retracement) is next important resistance on the charts. Is this morning’s intraday reversal a first tentative sign of USD bottoming?

Yesterday, slightly softer UK CPI data had only a limited impact on sterling. Cable mostly followed the broader USD price moves. EUR/GBP is holding a tight range near the 0.89 pivot. There are no important eco data in the UK today. BoE’s Saunders will speak in London. More technical order-driven trading might be on the cards for sterling.

EUR/USD rally slows, but to clear sign of a trend reversal yet