Sunrise Market Commentary

- Rates: Higher CPI sends US 10-yr yield to new cycle high

The global core bond sell-off accelerated yesterday on higher-than-expected US CPI data. US yields set new cycle highs for tenors up to 10-yr. The 10-yr yield closes in on key resistance around 3.05% (2014 high). Today’s heavy US eco calendar might set the stage for more losses. Not that much good news is probably needed to do so. - Currencies: Risk rebound hammers dollar

The dollar showed remarkable swings. Higher US CPI and disappointing retail sales attracted bottom fishers in the equities. This equity rebound caused sharp USD selling across the board, even in USD/JPY. The move continues this morning. For now, this repositioning develops independent from the data. For now, the dollar is a falling knife…

The Sunrise Headlines

- Traditional market correlations disappeared after yesterday’s combination of higher US inflation and disappointing retail sales. US yields added up to 9 bps, the dollar fainted and US equities skyrocketed (>+1%). Several Asian markets are closed this morning for lunar New Year; the others gain ground as well.

- Oil prices extended gains, pushed up by a weak dollar and by comments from Saudi Arabia that it would rather see an undersupplied market than end a deal with OPEC and Russia to withhold production.

- Japan’s Finance Minister Aso says the yen isn’t rising or falling abruptly enough for us to intervene now. He couldn’t change recent yen strength. USD/JPY dropped towards 106.50.

- Australian employment data printed very close to expectations with a 16k net job creation and a stabilization of the unemployment rate 5.5%. Underlying figures disappointed somewhat as full time jobs were shed (-49.8k).

- Jacob Zuma resigned as President of South Africa, reluctantly heeding orders by the ruling ANC to bring an end to his nine scandal-plagued years in power.

- A bipartisan Senate plan to protect young illegal immigrants from deportation and pour billions of dollars into border security appeared headed toward a Senate showdown on Thursday.

- Today’s eco calendar heats up in the US with empire manufacturing, weekly jobless claims, PPI inflation, Philly Fed business outlook and industrial production. Spain and France tap the bond market

Currencies: Risk Rebound Hammers Dollar

Risk-rally hammers USD, despite higher US yields

The dollar made some wild and very remarkable swings yesterday. US CPI printed higher than expected, but retail sales posted at big miss. US yields and the dollar jumped higher immediately after the release. US yields held their gains setting new cycle peaks, but the dollar reversed course soon. An initial decline in equities attracted bottom fishers and kick-started an impressive risk-rebound, despite poor retail sales. This risk rally also hammered the dollar. EUR/USD jumped from the high 1.22 area to close the session at 1.2451. Even USD/JPY remained under pressure despite higher core yields and the equity rally! USD/JPY finished the session at 107.01. The ‘usual correlations’ didn’t work at all.

Positive risk sentiment and the dollar decline remain at play overnight. Several markets (China, Korea) are closed for the Lunar New year. Japanese equities remarkably joined the global risk rally despite a further decline of USD/JPY and poor December machine orders (-11.9% M/M). USD/JPY is trading in the mid 106 area. EUR/USD trades in the 1.2465 area holding near the overnight peak. The risk rally at least eased the decline of EUR/JPY. The pair hovers in the mid 132 area.

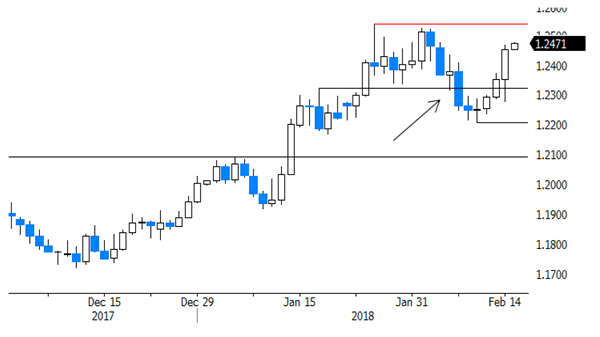

The US eco calendar is again well filled today with Empire manufacturing, Philly Fed business outlook, jobless claims, industrial production and, last but not least the PPI data. Sentiment indicators and activity data are expected to confirm decent growth. PPI is expected to rise 0.4% M/M, but decline from 2.6% to 2.5% on a yearly basis. Good eco data and/or an upward surprise in PPI might reinforce the rise in US yields. However, considering yesterday’s price action, it is unlikely to change fortunes for the dollar. The repositioning on equity markets and technical considerations are probably more important. At least for now, risk sentiment correlates with a further decline of the dollar. In this move we also keep an eye at the technicals. EUR/USD is nearing the 1.2537 correction top. A break above this level would signal more trouble for the dollar. We don’t see a fundamental reason for EUR/USD to already break this level, but this is not a good enough reason to row against the tide. The dollar is a falling knife. A return below 1.2206 would be a first sign, that the USD sell-off easing.

UK retail sales are expected to rebound 0.6% M/M and 2.4% Y/Y after a sharp setback in January. We doubt that even better than expected data will be a big help for sterling. EUR/GBP holds the 0.8690/0.9033 range, with intermediate resistance at 0.8930. We hold our view that the 0.8690 support won’t be easy to break without big progress on Brexit.

EUR/USD nears ST range top