Here are the latest developments in global markets:

FOREX: The dollar index was slightly down on Tuesday after gaining less than 0.2% on Monday, in an environment where concerns for a trade war following the Trump administration’s decision to impose tariffs on imported steel and aluminum were easing.

STOCKS: US markets closed markedly higher yesterday, recovering some of their latest losses, as concerns over a potential trade war receded somewhat. The gains came after US House Speaker Paul Ryan urged the President to reconsider his tariffs, sending the message that not even the Republicans are comfortable with such measures. The Dow Jones led the charge, gaining nearly 1.4%. The S&P 500 rose by 1.1%, while the Nasdaq Composite followed in its track, up by 1.0%. Futures tracking the Dow, S&P, and Nasdaq 100 are all flashing green as well. Asian markets took their cue from the US and surged. In Japan, the Nikkei 225 and the Topix finished higher by 1.8% and 1.3% respectively, while in Hong Kong, the Hang Seng trade higher by 2.3%. Europe was a similar story. Futures tracking all the major indices were a sea of green today, pointing to a higher open for these benchmarks.

COMMODITIES: In energy markets, oil prices staged a comeback yesterday, as risk sentiment recovered. Commodities like oil are considered relatively risky and are thus quite sensitive to changes in investors’ risk appetite. Both WTI and Brent crude are higher by 0.2% today, extending the gains from yesterday. Today, traders will look to the release of the private API inventory data, which tend to set the tone for what to expect from the official EIA data, due out tomorrow. In precious metals, gold was higher but only by 0.1%, last seen near the $1320 per ounce mark. Gold traded lower yesterday, as diminishing concerns over a trade war likely decreased the yellow metal’s allure, a reaction seen in other safe havens as well, such as the Japanese yen and the Swiss franc.

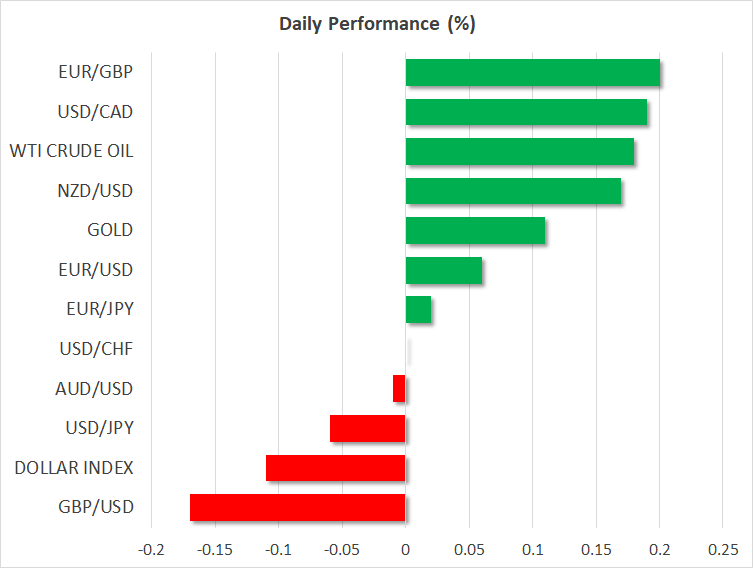

Major movers: Dollar little changed as trade fears recede; loonie under pressure

Major movers: Dollar little changed as trade fears recede; loonie under pressure

The dollar’s index against a basket of currencies was 0.1% down amid receding worries for a trade war following last week’s decision on tariffs by US President Donald Trump. Pressure on Trump – coming from House Speaker Paul Ryan as well – to reconsider his decision, may have acted as a catalyst for market concerns to ease.

Equity markets gaining is also an indication that market participants are becoming less worried of the situation. Still, with things looking fluid, it should be said that markets may be running ahead of themselves.

Dollar/yen was little changed at 106.13 after rising on Monday. This compares to Friday’s 16-month low of 105.23 when the yen was attracting safe-haven flows on the back of uncertainty over trade. Also yen-related, the currency didn’t react much after Bank of Japan Governor Haruhiko Kuroda said on Tuesday that there were downside risks to the central bank’s forecast that inflation would reach its 2% target around the fiscal year ending in March 2020.

In other closely watched pairs: euro/dollar was not much changed at 1.2335, with the pair recording a two-week high of 1.2365 on Monday, a day during which uncertainty following Sunday’s Italian elections was dominating attention. Brexit-sensitive sterling was 0.15% down versus the greenback at 1.3830.

Dollar/loonie has been a pair that has been attracting additional interest lately, as Canada is the largest exporter of steel to the US. The Canadian dollar has come under increased pressure on the tariffs story, with dollar/loonie rising to 1.30 on Monday, this being an eight-month high. The pair was 0.2% up at 0731 GMT, trading close to the aforementioned peak. Trump’s intention to use the proposed tariffs on steel and aluminum to gain leverage in NAFTA talks is not helping the Canadian currency either. It should also be noted that the Bank of Canada meets tomorrow, and some of the recent softness in the CAD likely reflects expectations that policymakers may strike a concerned tone, amid heightened trade risks.

The Australian dollar was roughly flat at $0.7762, with minimal reaction to the Reserve Bank of Australia’s decision to keep interest rates steady at the record low of 1.5%, though there were some concerns as the central bank was cautious on the outlook for growth. Kiwi/dollar was higher by around 0.2%, at 0.7237.

Day ahead: Trade considerations to remain at the forefront on quiet calendar day

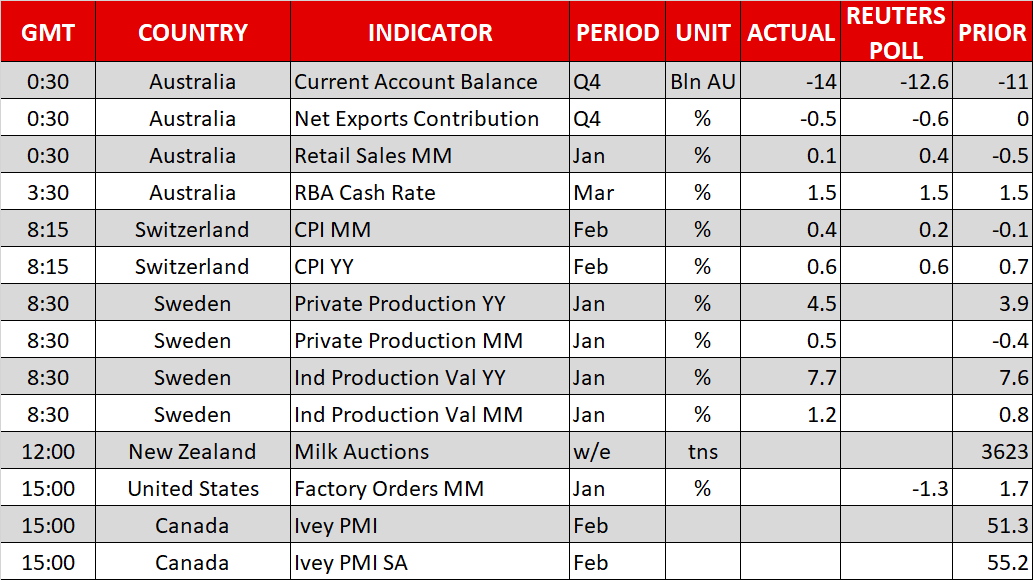

The economic calendar is relatively light today, with only second-tier releases on the agenda. In the US, factory orders for January are due out at 1500 GMT, and the forecast is for the figure to have dropped by 1.3% in monthly terms, a turnaround following a 1.7% rise previously.

In Canada, the Ivey PMI for February will be in focus (1500 GMT), ahead of the Bank of Canada’s rate decision tomorrow.

Elsewhere, NZD traders will keep their eyes on the bi-weekly milk auction. The release is tentative, lacking a specific time, but most economic calendars have it marked for 1200 GMT. While there is no forecast available for the figure, it tends to be a market mover for the kiwi dollar, considering New Zealand’s status as a major dairy exporter.

On the Brexit front, the EU is anticipated to publish its draft guidelines for a post-Brexit trade deal, though media reports suggest these are likely to be relatively short and vague, allowing room for the UK to clarify what it wants in the coming weeks.

In energy markets, oil traders will turn their sights to the private API weekly inventory data that will be released at 2130 GMT.

Equity investors will probably remain focused on any comments regarding tariffs and global trade, as they try to gauge the probability of a trade war materializing. While price action yesterday was driven by expectations that Congress will serve as a hurdle to tariffs, it’s important to note that a few hours later, President Trump said he is not backing down on the issue. Over the coming days, markets will be looking for fresh clues as to whether this rhetoric is simply posturing in complex trade negotiations, similar to the “fire and fury” remarks, or whether the US President will stick to his guns and risk a tit-for-tat retaliation by other nations.

Regarding policymakers’ appearances, we will hear from New York Fed President William Dudley (a permanent FOMC voting member) at 1230 GMT. Next in line will be the Bank of England’s chief economist and MPC member Andy Haldane, who will deliver remarks at 1800 GMT. While neither Dudley’s, nor Haldane’s topics of discussion are related to monetary policy directly, comments on the subject are always a possibility from these highly-influential policymakers. The Governor of the Reserve Bank of Australia, Philip Lowe, will also step up to the rostrum at 2135 GMT.

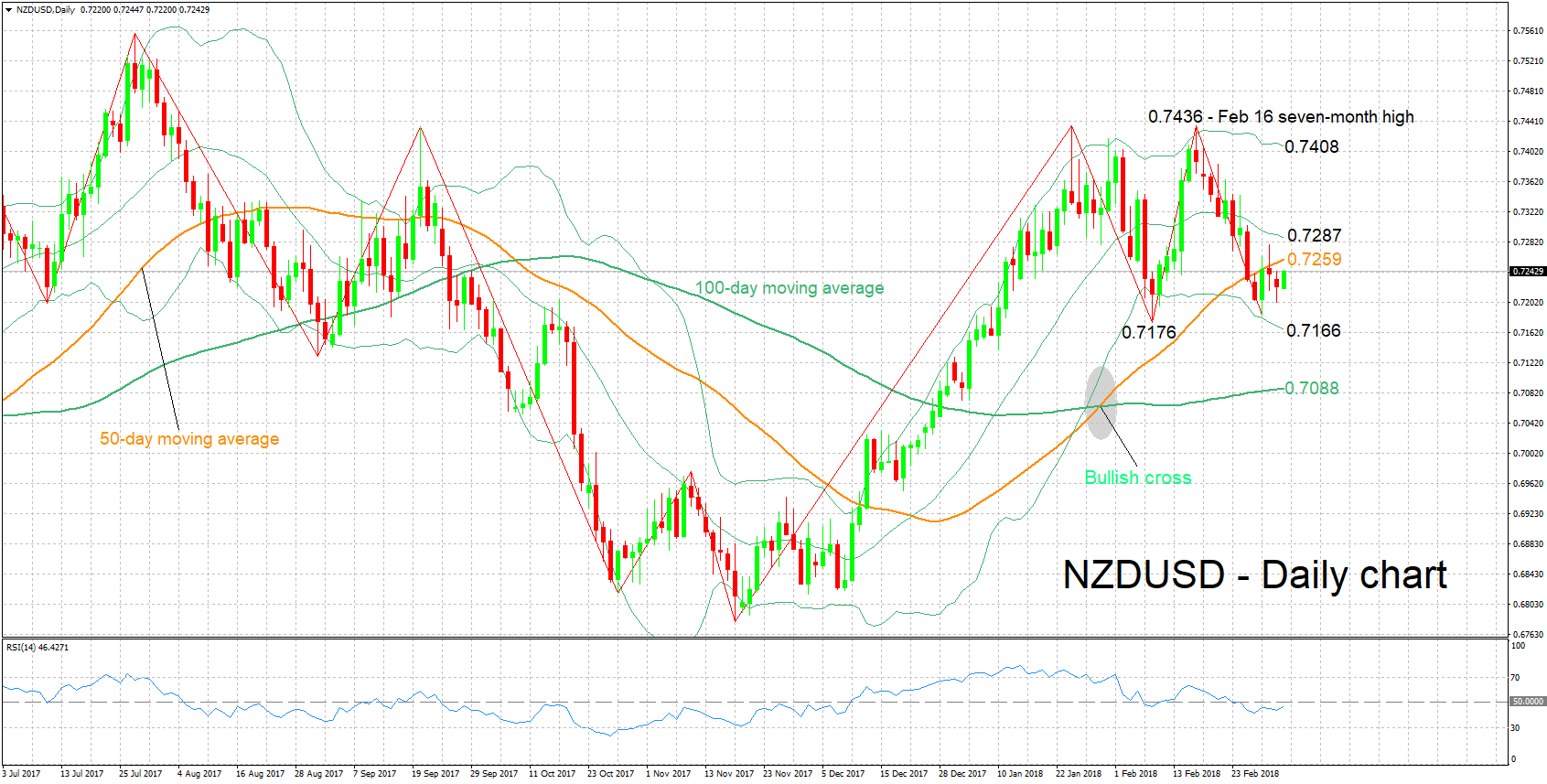

Technical Analysis: NZDUSD looking neutral ahead of milk auction

NZDUSD has distanced itself to the upside from the one-month low of 0.7185 hit last Thursday. The RSI has halted its decline and has been moving sideways for the most part in recent days, pointing to a neutral picture in the short-term.

Should today’s bi-weekly milk auction show a rise in prices, then the pair might receive a boost; New Zealand is a major dairy exporter. Resistance in this case might come around the 50-day moving average at 0.7259, with stronger gains shifting the focus to the middle Bollinger line – a 20-day moving average line – at 0.7287.

If on the other hand milk prices surprise to the downside, NZDUSD could record losses. In this scenario, support could come around the lower Bollinger band at 0.7166. The area around this level also includes last week’s one-month low of 0.7185, as well as the two-month low of 0.7176 that was recorded on February 8.

{kind=link}