Tuesday March 13: Five things the markets are talking about

European equities are drifting following a mixed session in Asia and the ‘mighty’ U.S dollar is steady as capital markets wait for this morning’s U.S inflation report for clues on the pace of Fed policy-tightening. Treasury yields have nudged a tad higher, while oil has slipped again.

This morning’s U.S CPI (08:30 am EDT) could confirm that U.S inflation remains tepid, even as the job market remains tight. Last Friday’s Labor Department report showed that U.S wages rose +2.6% y/y in February, below expectations, while the annual wage gain in January was revised down to a +2.8% increase.

Note: The market will also be looking to reports on wholesale prices and retail sales (Mar 14) for guidance ahead of next week’s FOMC meeting (Mar 20-21). The Fed is expected to hike rate +25 bps and is scheduled to release their updated forecasts for the path of monetary policy (dot plot) and economic growth.

Politics again is a market focus after President Trump issued an executive order blocking Broadcom from acquiring Qualcomm, thwarting a +$117B hostile takeover in the name of U.S national security.

On tap: China data on industrial production, retail sales and fixed-asset investment are all out on Wednesday and are expected to point to slower growth.

1. Stocks mixed results

In Japan, equities rallied for a fourth consecutive session overnight as a weaker yen (¥107.07) triggered buying, offsetting any weakness in steelmakers and automakers still battered by concerns about U.S tariffs on imported steel and aluminum. The Nikkei average gained +0.7%, while the broader Topix added +0.6%.

Down-under, Australia’s S&P/ASX 200 slipped -0.4% on weakness in major mining and oil stocks, while in S. Korea, the Kospi closed out +0.4% higher, supported mostly by Samsung’s +3.9% gain.

In Hong Kong, stocks ended little changed on Tuesday as investors considered the impact of a government reshuffle on the mainland. China is merging its banking and insurance regulators and giving new powers to policymaking bodies such as the People’s Bank of China (PBoC) in the biggest government shake-up in years. At close of trade, the Hang Seng index was flat, while the Hang Seng China Enterprises index rose +0.4%.

In China, stocks broke a three-day winning streak and ended lower, weighed down by healthcare and consumer stocks and the impact of a government reshuffle. At the close, the Shanghai Composite index was down -0.5%, while the blue-chip CSI300 index was down -0.9%.

In Europe, regional indices trade higher across the board following the mixed session in Asia. Stateside, shares of Qualcomm will be in focus after receiving a presidential order prohibiting Broadcom’s proposed takeover.

U.S stocks are set to open in the ‘black’ (+0.2%).

Indices: Stoxx600 +0.1% at 379.6, FTSE flat at 7215, DAX +0.2% at 12437, CAC-40 +0.5% at 5301, IBEX-35 +0.8% at 9800, FTSE MIB +0.4% at 22846, SMI +0.1% at 8979, S&P 500 Futures +0.2%

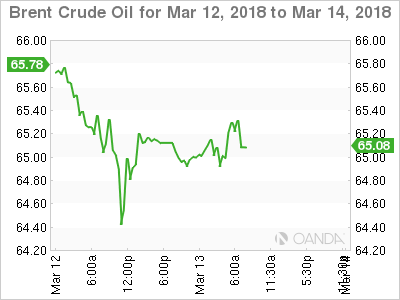

2. Oil prices dip on rise in U.S crude output, gold lower

Oil prices have dipped overnight, extending Monday’s losses, as the relentless rise in U.S crude output continues to weigh on the market.

Brent crude futures are at +$64.77 per barrel, down -18c, or -0.3%. U.S West Texas Intermediate (WTI) crude futures are at +$61.18 a barrel, down -18c, or -0.3% from Monday’s close.

Note: Both crude benchmarks dropped by around -1% in yesterday’s session.

Nevertheless, global healthy demand and ongoing supply restraint by OPEC and Russia is preventing much deeper pullbacks presently. However, U.S production is expected to rise above +11m bpd by late 2018, taking the top spot from Russia, according to IEA.

In it’s monthly report yesterday, the EIA noted that the rising U.S output comes largely on the back of onshore shale oil production. Production from major shale formations is expected to rise by +131k bpd in April from the previous month to a record +6.95m bpd.

Traders will take their cues form this week’s U.S inventory reports.

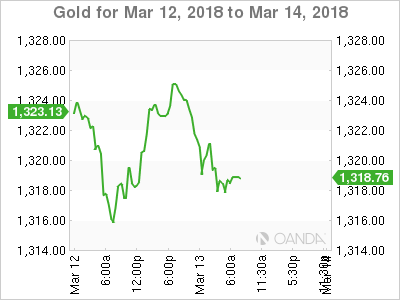

Ahead of the U.S open, gold prices are under pressure on a firmer dollar as the market waits for this morning’s U.S consumer price data to gauge the outlook for inflation and the Fed’s rate hike stance. Spot gold is down -0.2% at $1,319.87 per ounce.

3. Sovereign yields look for guidance

Euro zone sovereign bond yields are little changed, as investors continue to brace themselves for this week’s hefty bond supply as well as today’s U.S inflation data that could provide clues on the pace of monetary tightening from the Fed.

European bond markets have been well supported since last Thursday’s ECB, with policy makers stressing that interest rates will remain “low for some time” even as they take tentative steps towards exiting QE.

Today’s inflation data is particularly important, as many analyst are forecasting the Fed will raise interest rates four times this year, compared with the three increases policy makers have penciled in at their December meeting.

Note: Should the Fed signal they intend to accelerate the pace of monetary tightening, it could give a boost to the dollar, which had declined -2.5% in 2018.

A headline print that misses or meets estimates is likely to reaffirm the case for three-rate hikes this year and give the green light to fresh appetite for risk assets.

The yield on U.S 10-year Treasuries has increased +1 bps to +2.88%. In Germany, the 10-year Bund yield has climbed less than +1 bps to +0.63%, while in the U.K; the 10-year Gilt yield is unchanged at +1.494%, the highest in a week.

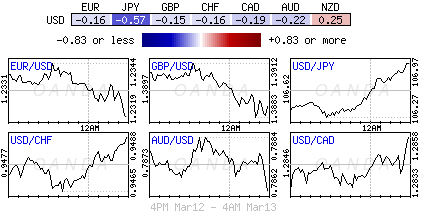

4. Dollar looks for direction

The USD is little changed against G10 currency pairs with the focus turning to today’s U.S CPI data.

GBP/USD (£1.3880) is a tad softer ahead of Chancellor of Exchequer Hammond “Spring Statement” (07:30 am today). Dealers note that the commentary would most likely influence Gilt prices the most, as less issuance is expected throughout the current fiscal year due to higher U.K tax receipts.

USD/JPY (¥107.16) is higher by +0.6% above the psychological ¥107 handle for its best session in five-months with the USD aided by yesterday’s U.S Treasury auction results – the highest 3-year bond yield in 11-years.

The market remains on Japanese political watch – Japan’s Fin. Min. Aso mighty skip the G20 finance minister meeting in Buenos Aires later this month with calls for his resignation following the recent shenanigans surrounding the cover-up of a government land sale.

Elsewhere, the EUR is little changed, trading atop of €1.2326, while the ZAR declined -0.2% to $11.8403.

5. U.S small business economy heats up

Data this morning from the NFIB (The National Federation of Independent Business) showed that U.S small business owners are showing strong confidence in the economy as the optimism index continues at record high numbers, rising to 107.6 in February vs. 107.1 (e).

The historically high numbers include a jump in small business owners increasing capital outlays and raising compensation. The federation supports +350k small U.S companies.

According to NFIB CEO, Juanita Duggan, “the historically high readings indicate that policy changes – lower taxes and fewer regulations – are transformative for small businesses. After years of standing on the sidelines and not benefiting from the so-called recovery, Main Street is on fire again.”