Here are the latest developments in global markets:

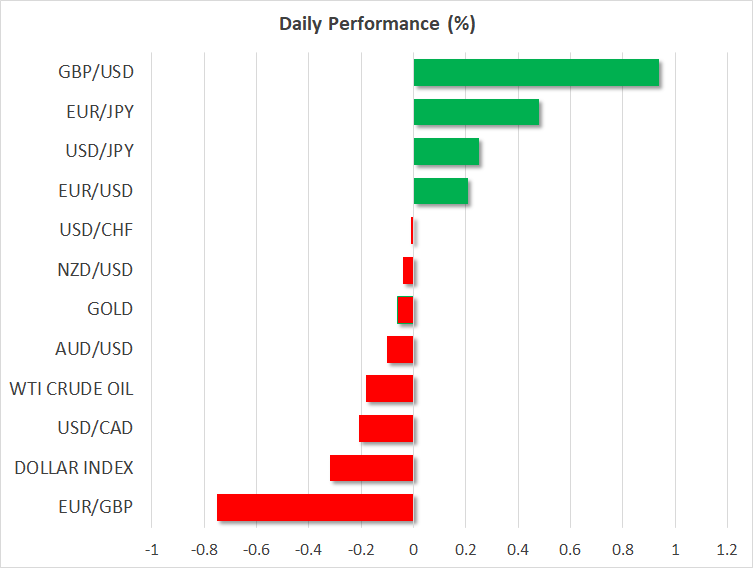

FOREX: The US dollar index outperformed on the day against a basket of currencies, falling to 89.97 (-0.22%) as the euro and the pound strengthened. Dollar/yen was gaining positive momentum in the face of uncertainties surrounding the Japanese finance minister and ahead of the FOMC rate decision on Wednesday, with the pair climbing to 106.30 (+0.21%). Euro/dollar recouped Friday’s losses rallying to 1.2324 (+0.13%) after Reuters sources reported that the ECB has shifted focus from the QE program to the path of interest rates, while pound/dollar and pound/yen hit three-week highs during early European afternoon as sources familiar with Brexit negotiations stated today that the EU and the UK agreed on the broad terms of Britain’s two-year transition deal after leaving the bloc in March 2019. The Canadian dollar was hit the hardest the past week. The loonie came under heavy selling pressure, driving dollar/loonie above the 1.3100 key level early this morning, creating a new 9-month high. Aussie/dollar was trading lower at 0.7695 (-0.27%) despite positive comments from the RBA Assistant Governor Christopher Kent and strong readings on Australia’s consumer confidence in the preceding week.

STOCK: European equities started the day on a softer tone as most of them are completing a red day. Stocks declined globally on Monday as investors awaited some risk events to take place this week, including central banks decisions, a EU summit, and the G20 meeting. The blue-chip Euro Stoxx 50 was down by 0.72%, the German DAX 30 plunged by 0.94% and the British FTSE 100 sank by 1.32% to the lowest level in almost two weeks of 7069.97 at 1030 GMT. The major US indices are poised to open lower today according to US mini stock futures

COMMODITIES: Oil prices were mixed. WTI crude oil was down by 0.08% at $62.29 per barrel, while Brent crude was up by 0.12% at $66.31. Copper plunged by 1.07% near the $3.06 level. Gold was weak at $1311.31 (-0.07%) per ounce.

Day ahead: G20 meeting could wake trade jitters; RBA meeting minutes due in the Asian session

Day ahead: G20 meeting could wake trade jitters; RBA meeting minutes due in the Asian session

The economic calendar will be empty of major data in the remaining of the day, giving some time to investors to prepare their positions ahead of high-spot events this week including three central bank policy meetings, a EU summit and the conclusion of the ongoing G20 meeting where finance ministers are expected to put pressure on the US over its unexpected trade protectionism.

Today, finance ministers from the Group of 20 biggest economies are gathering in Buenos Aires, Argentina, to kick off a two-day meeting, with the representatives expected to discuss on the performance of the global economy and the risks to growth. While such events are not usually attracting attention in foreign exchange markets, this time investors are eagerly anticipating to hear some critics against Trump’s recent import tariffs on steel and aluminum and his intention to take more aggressive steps against China, which have the potential to unleash a global trade war. The US Secretary Steven Mnuchin who will head the US team during the talks and has recently backed Trump’s tariff plans, could be in the defensive probably avoiding any comments that could worsen the negative sentiment around the story. However, if he disappoints his counterparts, supporting the need for further import tariffs on China, the dollar and other currencies linked to China’s economic performance such as the aussie and the kiwi could take a knock, while safe-haven assets could bounce higher.

Dollar bears could also take control if the Fed which starts its two-day policy meeting on Tuesday holds a dovish stance, probably throwing some cold water on speculations that the central bank could raise rates four times this year instead of three currently priced in the markets. Note that, Jerome Powell who will preside over his first meeting as Fed chair is highly expected to announce a 25bps rate hike at the conclusion of the meeting on Wednesday. The Reserve Bank of New Zealand and the Bank of England will follow but no change is expected in their monetary policy.

The EU summit on March 22-23 will be in focus as well for any updates on the Brexit front. If EU leaders manage to achieve a deal on the transition period, the pound could be free to join gains.

Turning to today’s public appearances, the Atlanta Fed President, Raphael Bostic will be speaking at 1340 GMT, while the ECB Executive board member, Yves Mersch will discuss on 2018 monetary policy challenges at 1800 GMT. Earlier, the Norges Bank Governor Oystein Olsen will also make comments at 1600 GMT.

Early on Tuesday, during the Asian session, the Reserve Bank of Australia (RBA) will publish monetary policy meeting minutes (0030 GMT), while at the same time the Australian Bureau of Statistics will be releasing figures on house prices for the final quarter of 2017. Recall that the RBA held interest rates unchanged at record lows for the 17 consecutive month on March 6, as they are waiting for further tightening in labour market to translate into faster wage growth and hence push inflation up towards the RBA’s target.

{kind=link}