Wednesday promises to be an eventful day for the dollar, with US CPI data for March and the minutes from the latest FOMC meeting likely to trigger renewed volatility in the world’s reserve currency. While a potential acceleration in inflation and a confident tone in the minutes could help the greenback recover a little, numerous trade and political uncertainties persist. Until they dissipate, any rallies in the currency could remain relatively limited.

Monetary policy has moved out of the spotlight in recent weeks, taking a back seat to global trade concerns, which have dominated price action in markets. With anxieties on the trade front subsiding somewhat though, for now at least, attention could gradually shift back to economic releases. In this respect, the US CPI data and the FOMC minutes from the March policy meeting that will be released on Wednesday at 1230 and 1800 GMT respectively are likely to set the tone for the greenback.

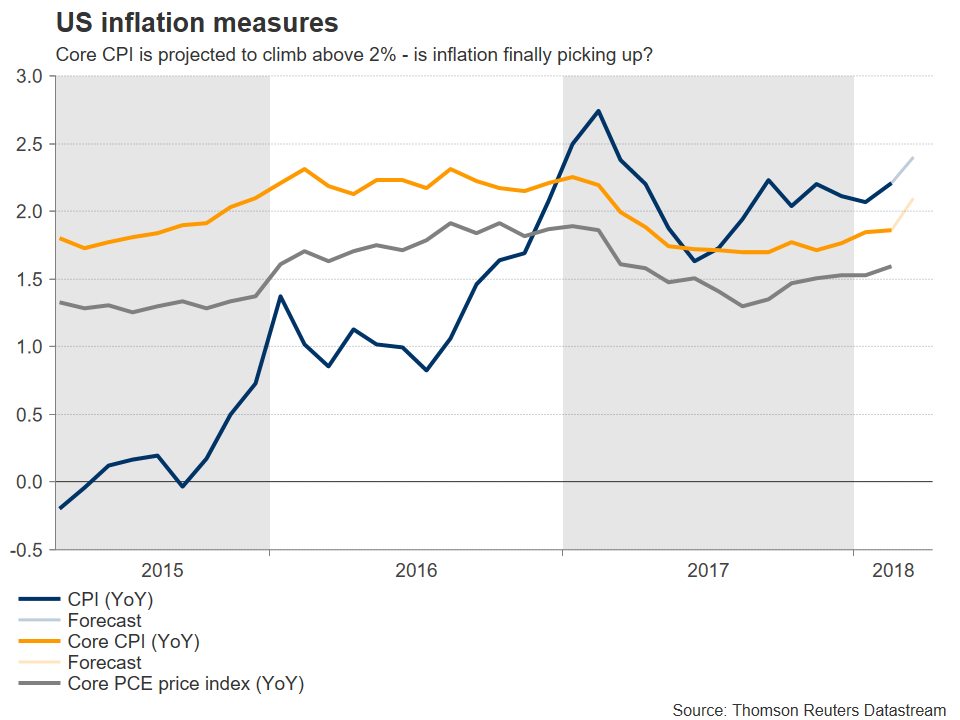

Kicking off with inflation, in March, the US CPI rate is forecast to have risen to 2.4% year-on-year, from 2.2% previously. The core rate – which excludes volatile items – is projected to have climbed to 2.1%, from 1.8% in February. These optimistic forecasts are supported by the Markit manufacturing and services PMIs for March, both of which showed a strong increase in prices charged by US firms. If the actual CPI figures meet these forecasts, then the narrative that US inflation is finally picking up steam would gain traction, amplifying expectations for a more aggressive tightening pace by the Fed.

Speaking of the Fed, the minutes from the March FOMC gathering – where the Committee raised interest rates by 25bps – will be closely watched for any fresh policy hints. Prior to that meeting, there was speculation policymakers could raise their rate projections to signal a total of four rate hikes in 2018, from three previously. However, officials disappointed those looking for such changes, keeping the so-called “dot plot” for 2018 unchanged at three hikes, triggering a drop in the dollar.

Speaking of the Fed, the minutes from the March FOMC gathering – where the Committee raised interest rates by 25bps – will be closely watched for any fresh policy hints. Prior to that meeting, there was speculation policymakers could raise their rate projections to signal a total of four rate hikes in 2018, from three previously. However, officials disappointed those looking for such changes, keeping the so-called “dot plot” for 2018 unchanged at three hikes, triggering a drop in the dollar.

That said, there were hawkish signals too, which markets mostly overlooked back then. First and foremost, the decision to keep the 2018 dots unchanged was a very close call. If just one more policymaker had raised her/his own projection to four hikes, the median dot for 2018 would have shifted higher as had been anticipated by some. Moreover, the rate projections for 2019 were revised up, which is another sign the Committee is becoming more confident in general. If the minutes reflect a sense of optimism, the dollar could gain as speculation for four hikes this year resurfaces.

Of course, there are also risks for the dollar. For instance, if the minutes reveal concerns about trade tensions and their potential impact, that could overshadow other positive signals on hikes. However, such worries are unlikely to be reflected in these minutes, given Chair Powell’s comments after the meeting that a discussion on trade had taken place, but the Committee’s outlook had not changed due to these risks. Not to mention that the gathering took place before trade tensions truly escalated, back when only the US tariffs on steel and aluminum were public.

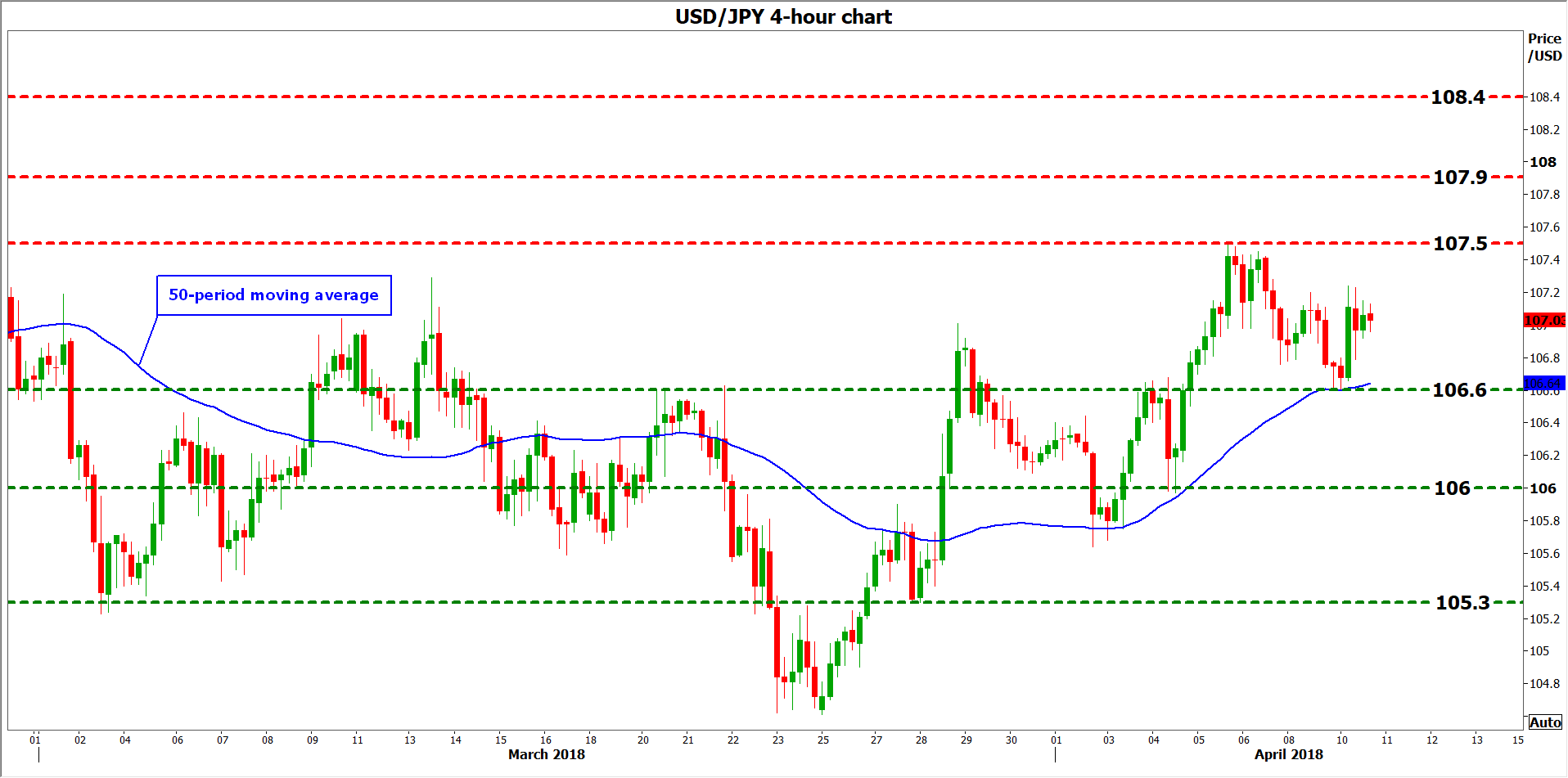

As for what is priced in already, investors have fully discounted another 25bps rate hike by year-end, and they also see an 80% probability for a second one, according to the Fed funds futures. An upside surprise in the CPI data or an upbeat tone in the minutes, could cement expectations for another two hikes this year and hence, push the dollar higher. Dollar/yen could edge up and challenge the 107.50 zone, defined by the April 5 highs. Further advances may encounter resistance initially around the peaks of February 21, at 107.90, and subsequently at 108.40, the lows of February 6.

As for what is priced in already, investors have fully discounted another 25bps rate hike by year-end, and they also see an 80% probability for a second one, according to the Fed funds futures. An upside surprise in the CPI data or an upbeat tone in the minutes, could cement expectations for another two hikes this year and hence, push the dollar higher. Dollar/yen could edge up and challenge the 107.50 zone, defined by the April 5 highs. Further advances may encounter resistance initially around the peaks of February 21, at 107.90, and subsequently at 108.40, the lows of February 6.

On the flipside, a disappointment in the CPIs, or a downbeat account of the FOMC meeting that focuses on trade risks for instance, could bring the greenback under renewed selling interest. In this case, dollar/yen could drop back down for a test of the 106.60 territory, identified by the April 10 lows. Steeper declines would likely bring the round figure of 106.00 into play, and further down, attention would shift to the 105.30 barrier, marked by the February 27 trough.

In the bigger picture, it’s important to note that even if the dollar spikes higher on these releases, numerous uncertainties persist. On trade, although US-China tensions subsided lately, we are not “out of the woods” yet. In politics, the Mueller investigation is heating up, while in geopolitics, the US is contemplating military action against Syria, risking fresh tensions with Russia. Until these risks ease, and most notably the trade risk, any rallies in the dollar could remain relatively limited.

{kind=link}