On Friday, the Bank of Japan will hold its first monetary policy decision under the leadership of the new Governor Kazuo Ueda. After taking the helm, Ueda has repeatedly highlighted that the central bank is in no rush to change the current policy settings, and thus no action is expected at this gathering. However, investors may be eager to find out whether there will be any hints regarding the timing of a potential normalization step, as well as whether there will be any changes in the Bank’s communication style in the Ueda era.

Policy changes not likely to happen quickly

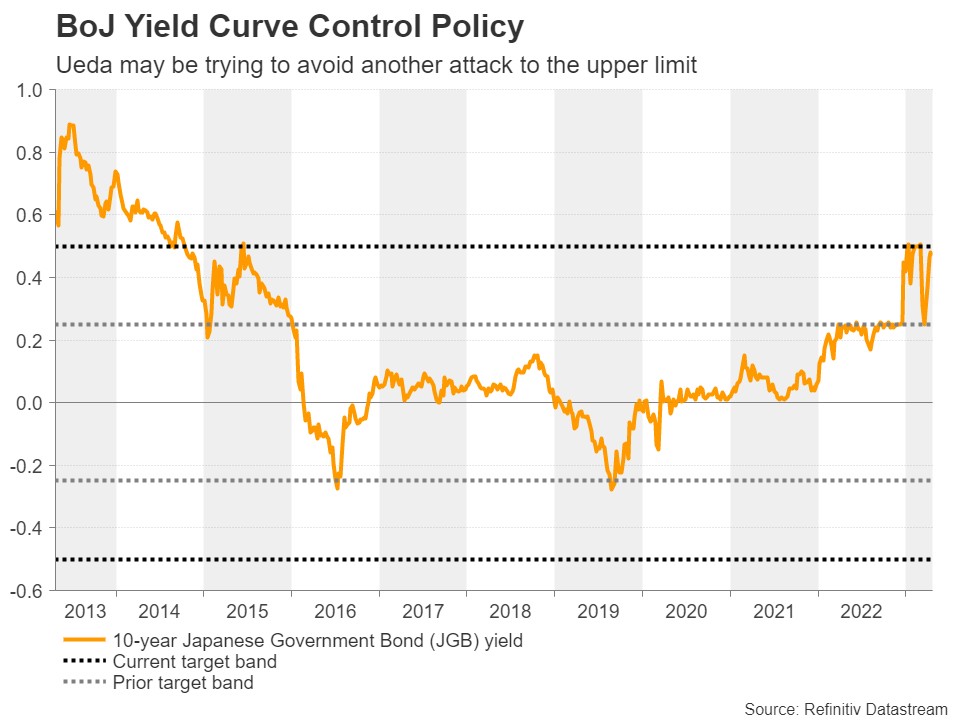

The last time the BoJ gathered to decide on monetary policy was back on March 10, with Kuroda taking the driver’s seat for the last time. Disappointing those expecting further widening of the yield control band, policymakers decided to keep all policy settings untouched under the reasoning that inflation seems to be fueled by import costs of raw materials rather than strong domestic demand.

Since taking the helm, Kuroda’s successor Kazuo Ueda has dropped some hints that massive stimulus will eventually be phased out, but he reassured the financial community that changes will not happen quickly. Like most of his new colleagues, he is an advocate of the view that inflation in Japan is not fueled by domestic demand, and by repeatedly highlighting that the current stance remains appropriate, he may be trying to avoid any anticipation of a pivot soon and thereby a surge in long-dated yields.

Data supports staying patient

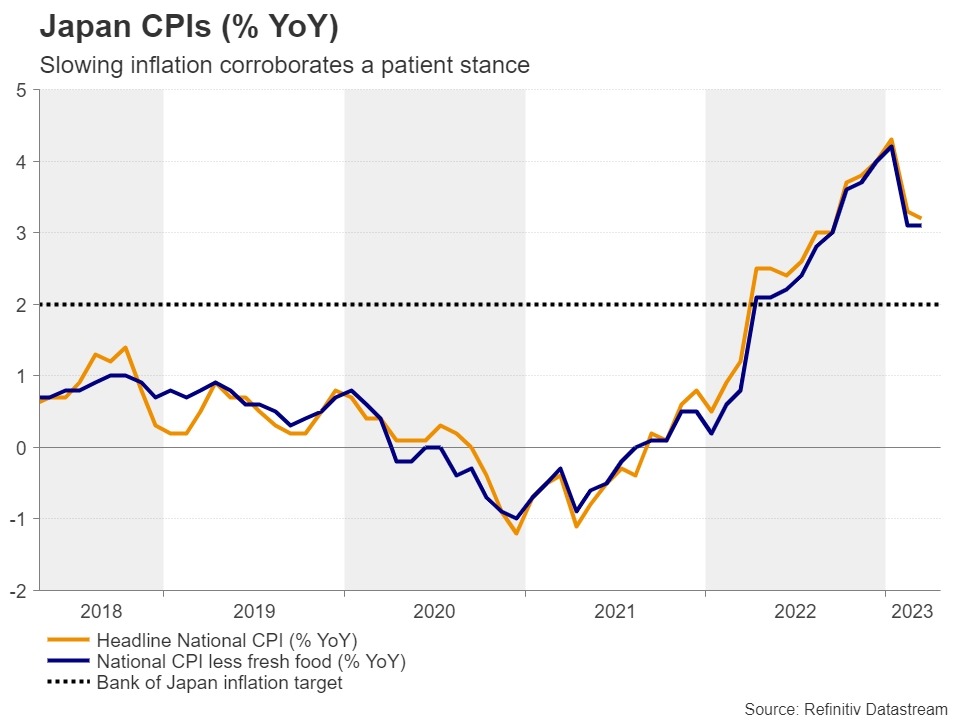

On the data front, headline inflation slowed in March by a tenth of a percentage point in yearly terms, but the month-over-month rate rebounded more strongly than expected and the underlying year-over-year CPI rate stayed unchanged. Although this may have stimulated expectations of a normalization step sooner rather than later, it is far from suggesting that a change is imminent.

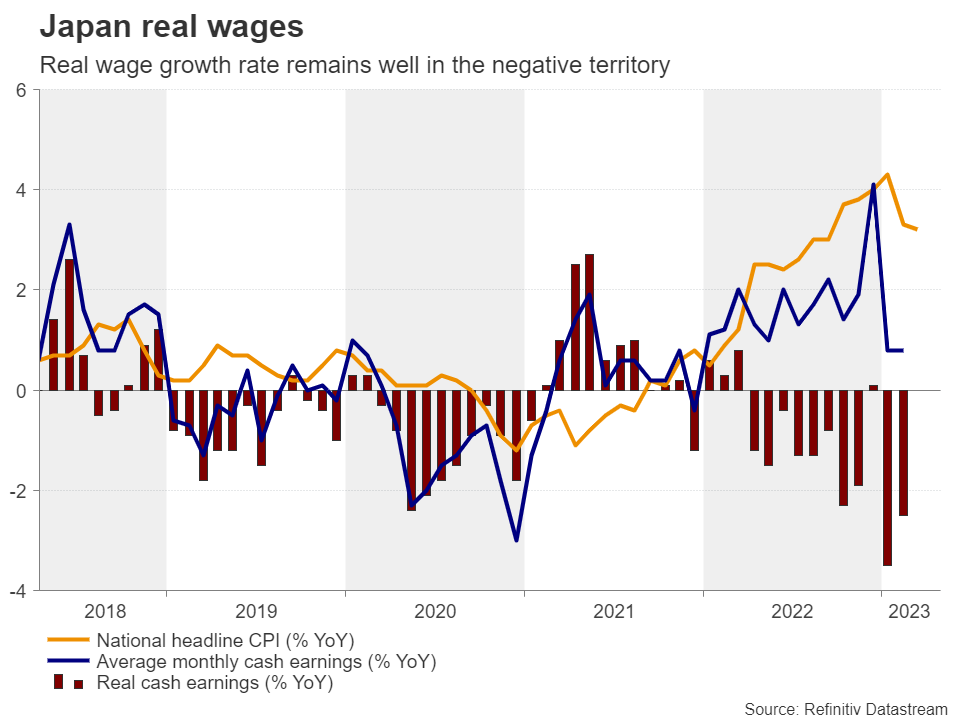

After all, these rates follow the steep slowdown during the month of February, which corroborated the narrative that inflation in Japan may be largely imported. On top of that, despite unions agreeing with employers on raising salaries by the most since 1993, the latest wage data we have in hand is for February, where earnings growth held steady at 0.8% y/y, leaving the real rate well in the negative territory. Therefore, given the Bank’s emphasis on wage growth, officials may not only prefer to wait for the accord to be reflected in the data, but also for evidence of sustained momentum before they proceed with removing further accommodation.

Focus to fall on hints about the coming months

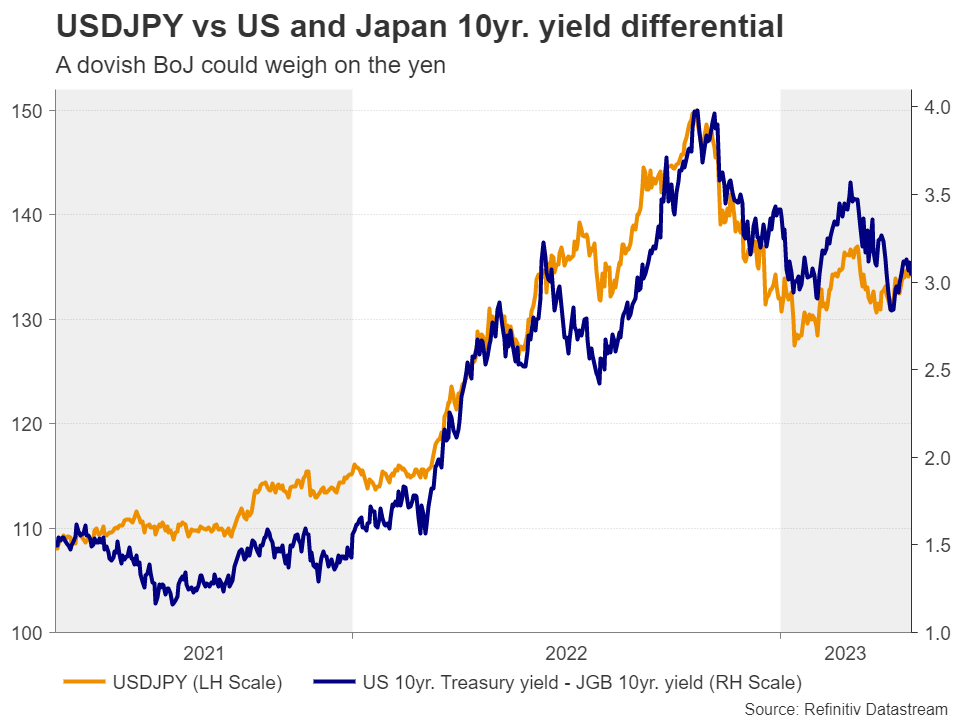

Therefore, the most likely outcome for this gathering is again no action. However, investors are likely to be looking for clues and hints on when and what kind of tightening the Bank will deliver in coming months. At his inaugural news conference on April 10, Ueda said that the lowered US and Japanese yields after the financial turmoil decreased the urgency to tweak yield curve control. So, anything suggesting that the Bank will stay the course through the summer may disappoint those expecting action soon and thereby hurt the yen.

On the other hand, any hints that another tweak may be appropriate at the upcoming gatherings could fuel the yen’s engines due to renewed market attacks on the upper limit of the target band around the 10-year yield. Nonetheless, bearing in mind that the BoJ likely prefers to avoid that, a scenario where they provide strong tightening signals seems unlikely.

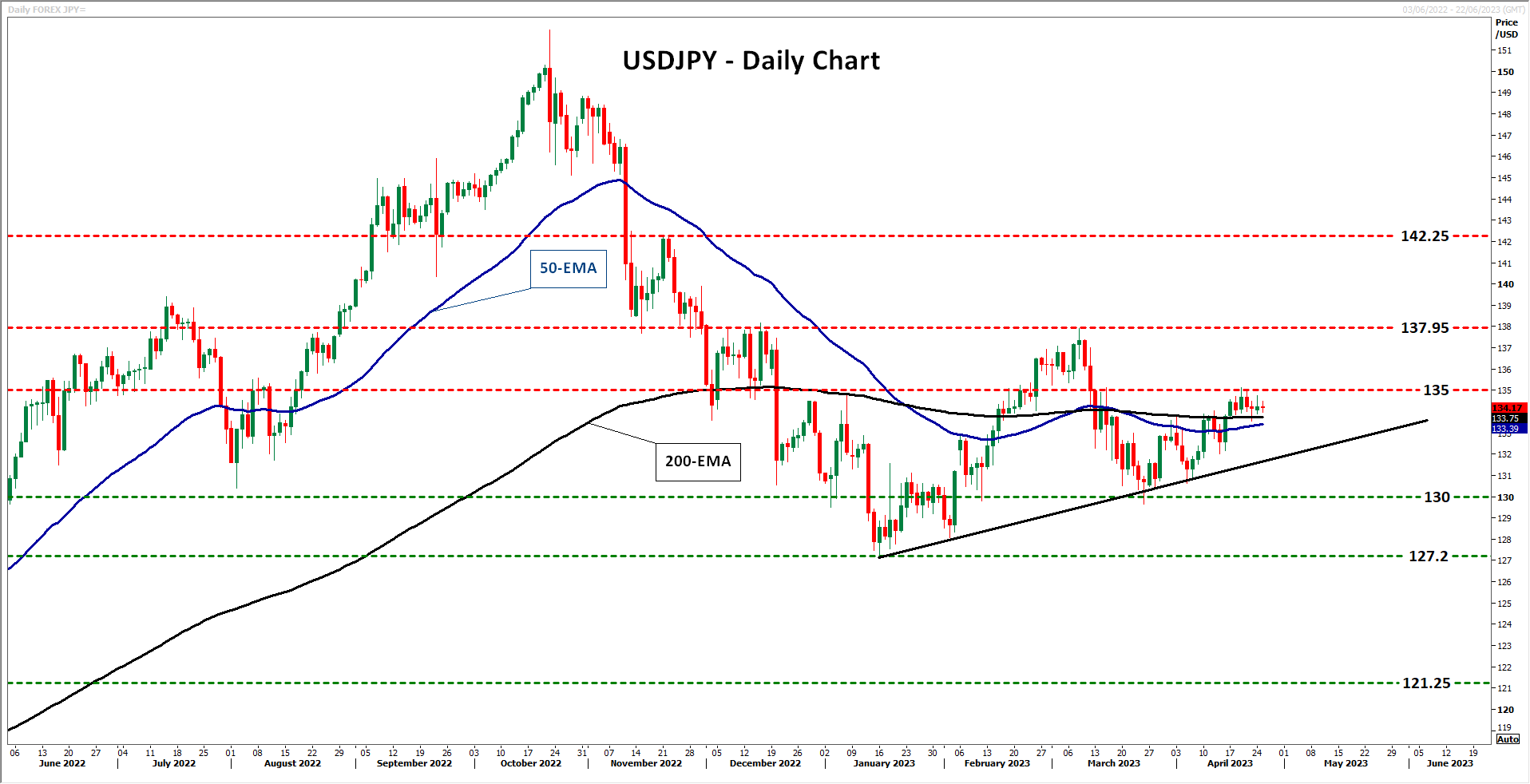

Yen could stay pressured in the short run

From a technical standpoint, dollar/yen has been in a recovery mode since April 5, when it hit the upside support line drawn from the low of January 16. Now the bulls are struggling to break above the 135.00 territory, but if they manage to do so, they may target the 137.95 barrier, marked by the high of March 8. If that zone doesn’t hold either, then the advance may extend towards the peak of November 22 at 142.25.

Having said all that though, it is still too early to chuck up the sponge on the yen. Ueda has clearly said that they are still looking for a removal of the YCC regime and a rate hike at some stage this year. So, with other major central banks, like the Fed, expected to start cutting interest rates towards the end of the year, at some point the new divergence in monetary policy expectations between the Fed and the BoJ may start working in favor of the yen.

{kind=link}