- Eurozone preliminary core CPI rate for April continued to inch lower at 2.7% y/y, its slowest pace of inflationary pressure since February 2022.

- 2-year and 10-year Eurozone sovereign bonds/US Treasuries yield spread discounts have continued to widen which supports a potential medium to long-term bearish trend on the EUR/USD.

- Watch the 1.0740 key short-term resistance on the EUR/USD ahead of the Fed’s monetary policy decision on 1 May.

Since its December 2023 high of 1.1140, the EUR/USD has traded lower in the past four months with an accumulated decline of -4.8% (-538 pips) and looks set to end this month of April with a negative footing, potentially a lower monthly closing level (traded at 1.0697 at this time of the writing below last month, March monthly closed level of 1.0790).

The key primary fundamental factor that is likely to determine the directional bias of the EUR/USD in the medium to long-term horizons is the path of inflationary trends in the Eurozone and the US which in turn dictates the monetary policy decisions and guidance of the two major developed nations central banks, the European Central Bank, and the US Federal Reserve.

Fundamentals are supporting a weaker EUR/USD in the medium to long-term horizon

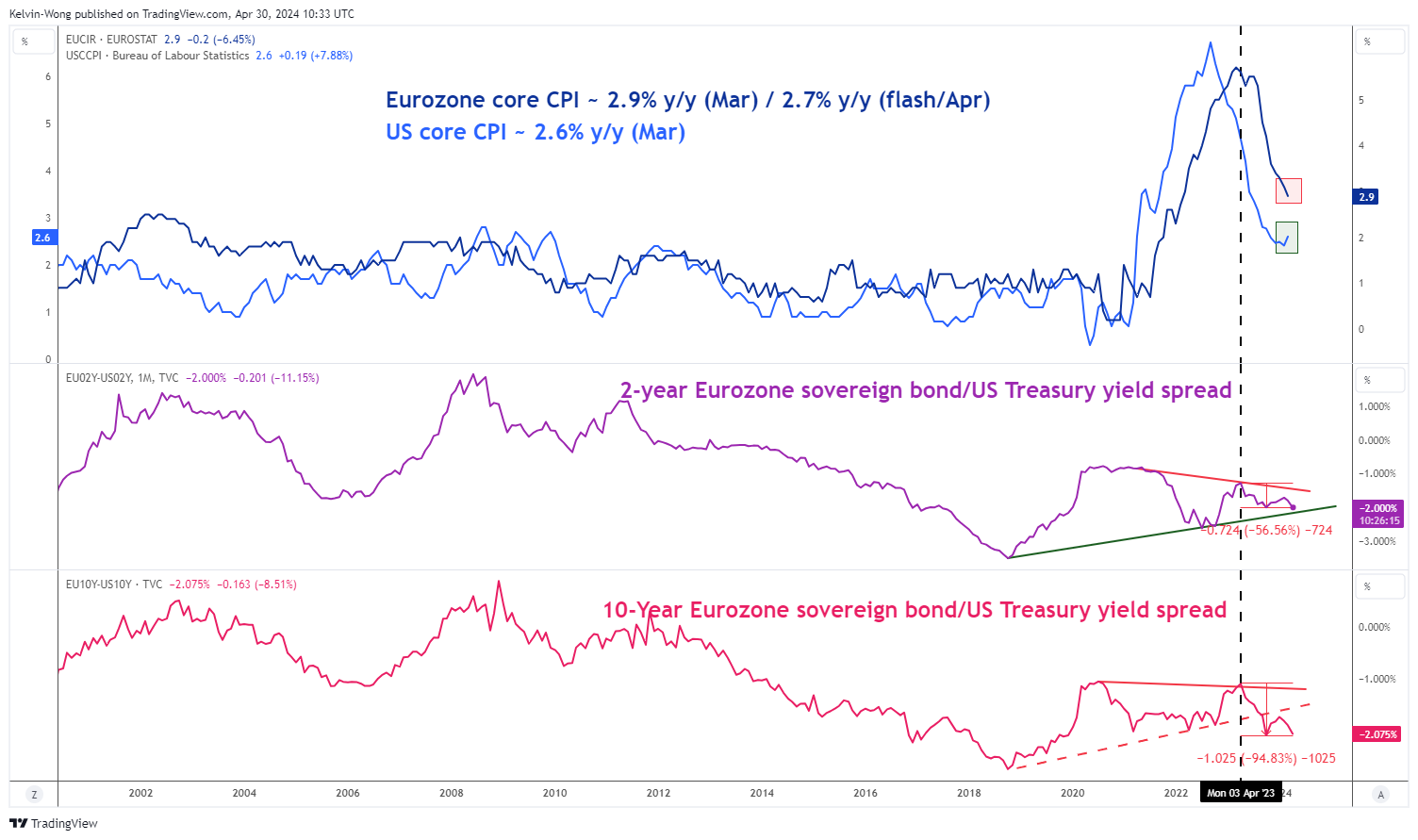

Fig 1: Eurozone, US inflationary trends with yield spreads of Eurozone sovereign bonds /US Treasuries as of 30 Apr 2024 (Source: TradingView, click to enlarge chart)

In comparing inflationary trends, the pace of change is more important than the absolute change levels. In March, the Eurozone core CPI rate (excluding food and energy) stood at 2.9% y/y which is higher in absolute terms versus the US core CPI rate of 2.6% y/y recorded in March.

On closer inspection, the trend of the US core CPI rate has inched higher from its prior month of February from 2.4% y/y to 2.6% y/y. In contrast, the trend of the Eurozone core CPI continued to decelerate in the past three months; January (3.3% y/y), February (3.1% y/y), March (2.9% y/y), and it continued to inch lower in April with a preliminary reading of 2.7% y/y, Eurozone’s slowest pace of inflationary pressure since February 2022.

Therefore, the odds of the first ECB interest rate to come in June or July have been rising whereas else the highly anticipated Fed dovish pivot narrative at the start of the year has evaporated with the expected first Fed funds rate being pushed back continuously from March (at the start of the year) to now September (based in latest data from CME FedWatch tool as of 29 April 2024) due to a sticky and elevated inflationary trend in the US.

A less potentially less dovish Fed over its ECB counterpart can be expressed via the sentiment inferred from market-based transacted financial instruments through the yield spread of the Eurozone sovereign bonds and US Treasuries.

Both the 2-year and 10-year Eurozone sovereign bond/US Treasury yield spread discount has widened over the past year since April 2023; more pronounced on the 10-year where its discount spread has widened more by around 100 bps versus 70 bps seen on the 2-year discount spread.

The further widening trend of the 10-year Eurozone sovereign bond/US Treasury yield spread discount suggests the long-term inflationary and economic growth trends in the Eurozone are likely to be in a softer tone versus the US which in turn supports a weaker EUR over the US dollar.

EUR/USD continued to trade sideways in the short-term

Fig 2: EUR/USD minor trend as of 30 Apr 2024 (Source: TradingView, click to enlarge chart)

Since its recent bounce of +1.4% (152 pips) from its 17 April 2024 low of 1.0601, the EUR/USD has been trading in a minor sideways range configuration near its 20-day moving average acting as a first roadblock against the bulls in the past four sessions as market participants wait for the upcoming US Fed’s monetary policy decision on 1 May with the main focus on Fed Chair Powell’s press conference.

In the lens of technical analysis, watch the key short-term pivotal resistance at 1.0740 (close to the 20-day moving average) and a break below 1.0680 near-term support may trigger renewed weakness on the EUR/USD to expose the next intermediate supports at 1.0640 and 1.0600 in the first step.

On the flip side, a clearance above 1.0740 sees the potential continuation of the short-term corrective countertrend rebound for the next intermediate resistances to come in at 1.0800 (the 50-day & 200-day moving averages) and 1.0850 (also the upper boundary of the medium-term descending channel from 28 December 2023 swing high).

and looks set to end this month of April with a negative footing, potentially a lower monthly closing level (traded at 1.0697 at this time of the writing below last month, March monthly closed level of 1.0790).){kind=link}