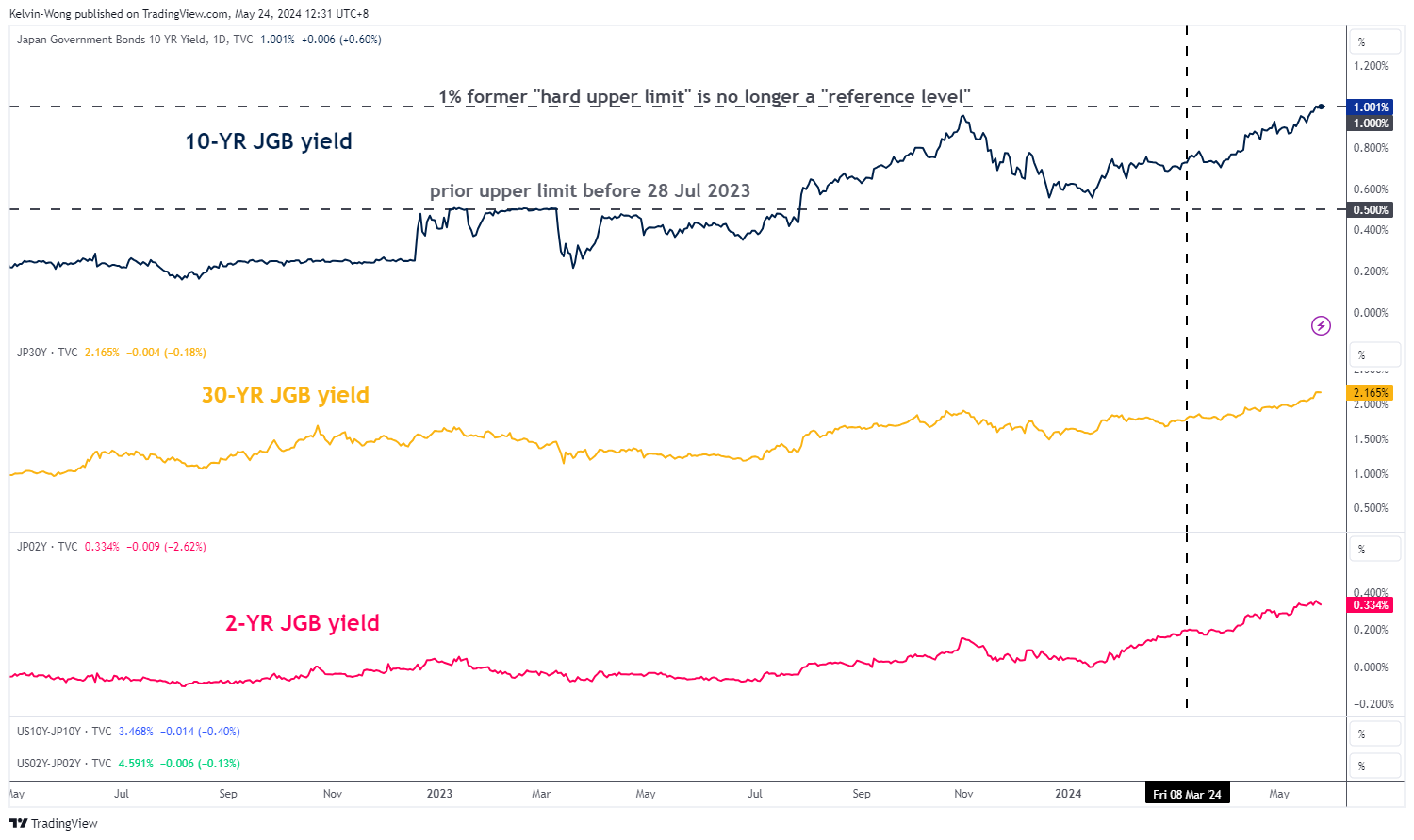

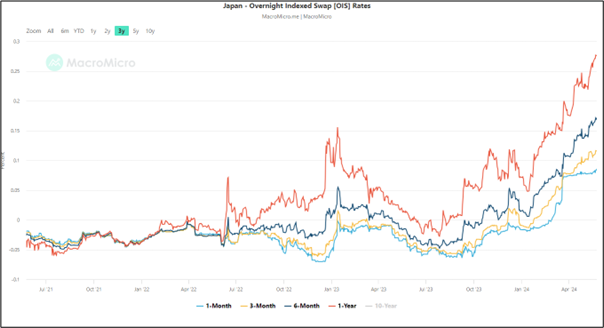

- The 10-year JGB yield has continued to push higher to 1% together with 3-month and 6-month overnight indexed swap (OIS) rates in Japan at 0.12% to 0.17%

- The JPY has failed to strengthen despite the bullish movements in JGB yields and OIS rates.

- Broad-based US dollar strength and the deceleration in the lagging core-core CPI inflation trend are the main drivers of short-term JPY weakness.

- Watch the key short-term support of 155.90 on the USD/JPY.

Since our last publication, the price actions of USD/JPY have continued to hold above its 20-day moving average acting as a support at 155.90 at this juncture despite a rise in both the 10-year and 30-year Japanese Government Bonds (JGB) yields since the start of this week to 1% (its highest level in almost 12 years) and 2.17% respectively (see Fig 1).

JGB yields and overnight index swap rates are pointing to a possible BoJ rate hike in July

Fig 1: JGB yields medium-term & major trends as of 24 May 2024 (Source: TradingView, click to enlarge chart)

Fig 2: Japan Overnight Indexed Swap Rates major trends as of 24 May 2024 (Source: MacroMicro, click to enlarge chart)

Even the overnight indexed swap rates (OIS) for 3-month and 6-month have risen at a faster pace to 0.12% to 0.17% over the 1-month OIS and their spreads have widened significantly which suggests the OIS market is pricing a higher chance of another Bank of Japan (BoJ) interest rate hike in the July meeting (see Fig 2).

So, what is causing the failure of the yen to stage a short-term bullish reversal?

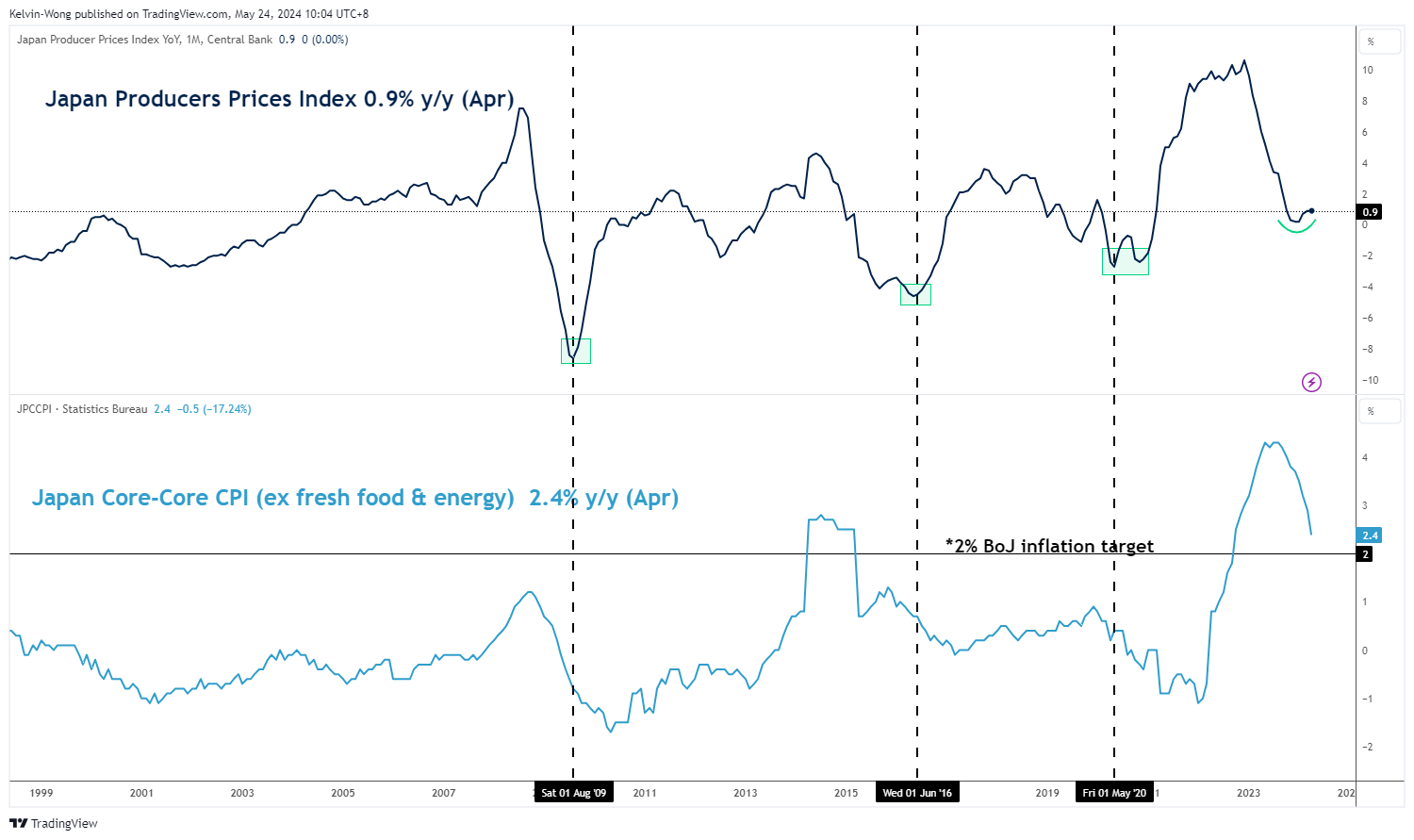

Deceleration of consumer inflationary trend in Japan

Fig 3: Japan Producer & Consumer Price Indices as of April 2024 (Source: TradingView, click to enlarge chart)

Inflation data is one of the key matrices to guide BoJ’s path of normalizing its decade-long ultra-accommodative monetary policy after ending its short-term negative interest rate in March.

BoJ Governor Ueda has implied in his public speeches that an interest rate hike cycle in Japan can only take shape if the inflation trend maintains a virtuous cycle of sustained, stable achievement of BoJ’s 2% target coupled with strong wage growth.

So far, Japan’s producer prices (PPI) have started to show signs of turning the corner after close to a year of deceleration from December 2022 to January 2024. In the past four months, the PPI has risen to 0.9% y/y in April from 0.2% y/y printed in January.

An interesting point to note is that the PPI tends to bottom out ahead of Japan’s consumer inflation as seen in the three past periods of August 2009, June 2016, and May 2020 (see Fig 3).

So far, the Japan core-core CPI (excludes fresh food and energy) which is closely watched by BoJ as a key gauge of broader inflation trends in Japan has failed to turn around and continued its path of deceleration since August 2023. It rose at a slower pace in April to 2.4% y/y from 2.9% y/y in March.

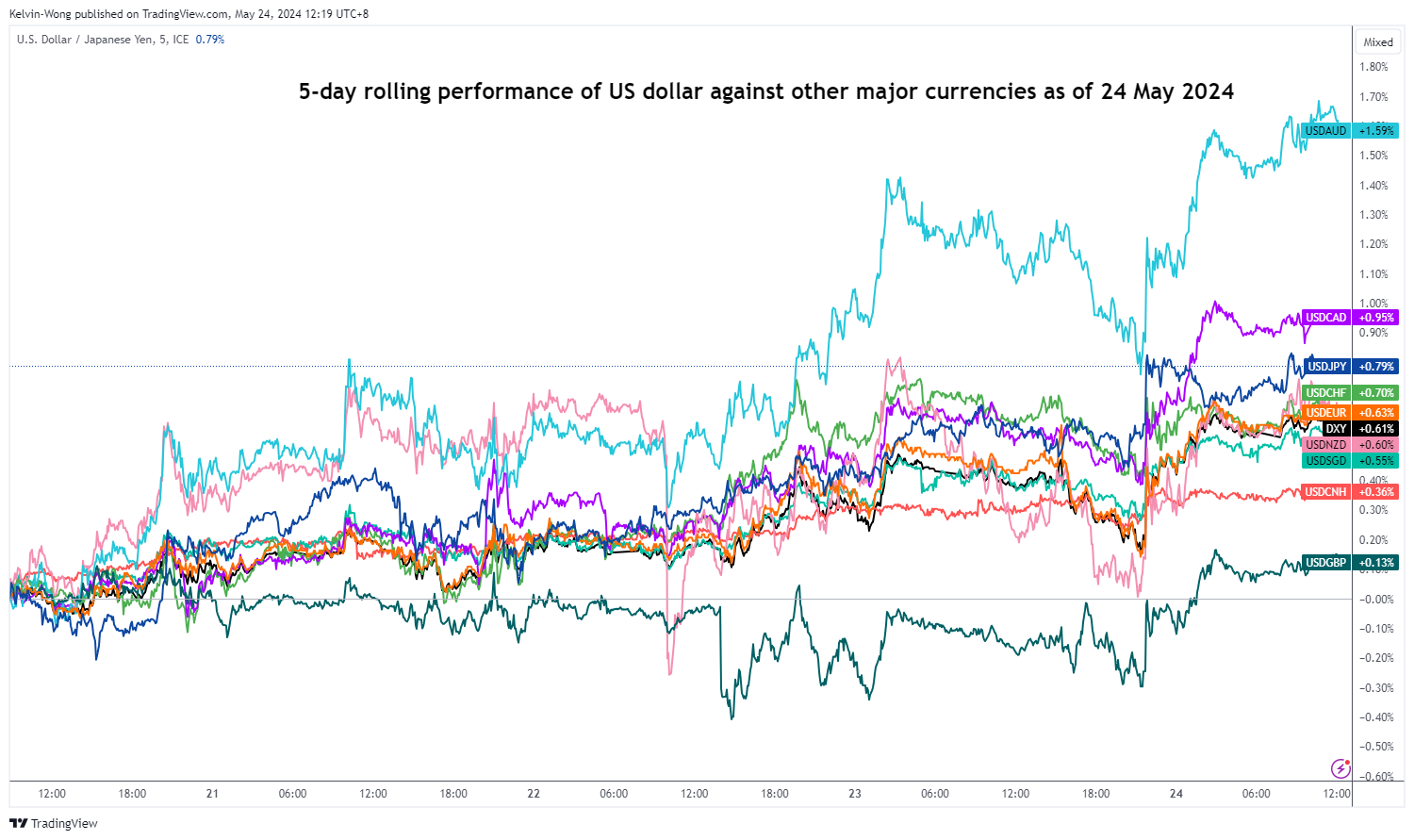

Broad-based US dollar strength revival

Fig 4: 5-day rolling performance of the US dollar against major currencies of 24 May 2024 (Source: TradingView, click to enlarge chart)

The US dollar has strengthened across the board against other major currencies reinforced by a further recovery in the US Treasury yields in place since last Friday, 17 May, and the 10-year yield is now just a whisker away from a key 4.50% technical level after it rallied by 16 basis points from last Wednesday low of 4.31% to yesterday, 23 May closing level of 4.48%.

So far, based on a 5-day rolling performance basis, the JPY is the third major weakest currency against the US dollar with the USD/JPY recording a gain of +0.8% at this time of the writing and surpassing the return of the US Dollar Index at +0.6% (see Fig 4).

USD/JPY has held above its 20-day moving average for 5 consecutive days

Fig 5: USD/JPY medium-term & major trends as of 24 May 2024 (Source: TradingView, click to enlarge chart)

Fig 6: USD/JPY short-term trend as of 24 May 2024 (Source: TradingView, click to enlarge chart)

The short-term uptrend phase of the USD/JPY remains intact, supported by a rising daily RSI momentum indicator that is above the 50 level, and has yet to reach its overbought level of above 70 (see Fig 5)

Watch the key short-term pivotal support at 155.90 (also the 20-day moving average) to maintain the short-term bullish tone for the next near-term resistance to come in at 158.00 and above it sees the 159.60/160.30 long-term pivotal resistance zone (see Fig 6).

On the other hand, a break below 155.90 invalidates the bullish bias for a minor corrective slide to expose the next near-term supports at 154.30 and 153.70 (also the 50-day moving average).

yields since the start of this week to 1% (its highest level in almost 12 years) and 2.17% respectively (see Fig 1).){kind=link}