{kind=link}

Dollar opens the week generally higher as boosted by news that Senate has finally passed their tax bill. But strength is relatively limited firstly on concern that Russian probe is getting closer to President Donald Trump. Secondly, there are talks that the final version of the tax bill would just give very little lift to the economy. Sterling is also cautious bullish on optimism over Brexit negotiation. Swiss Franc and Japanese Yen are trading as the weakest one today. Looking ahead, the week is jam-packed with RBA and BoC meeting, plus many heavy weight economic data including non-farm payrolls.

Final tax bill could only give 0.3% boost in 2018 growth

The US Senate finally passed their version of tax bill on Saturday after marathon debates and votes on amendments. Now Republicans will take the legislative process to the next stage and work on reconciliation of the bills of the House and the Senate. Goldman Sachs economists believe that the final structure of the reconciled bill will "reflect more of the Senate bill than the House bill". That would include having corporate tax cut to 20% effective in 2019, instead of 2018. Also, while the cut from 35% to 20% looks huge, they pointed out that considering the whole package of the tax reform, corporate tax rate will come down effective by "only a couple of percentage points". And, Gold Sachs forecast US growth to be boosted by a mere 0.3% for 2018 and 2019.

UK PM May to meet EC Juncker

UK Prime Minister Theresa May is going to have a lunch meeting with European Commission President Jean-Claude Juncker today. Juncker has set today as the deadline for May to revise her offer on Brexit. But UK government played down today’s significance and pointed to the EU summit on December 14/15 as the crucial one. In a statement, UK said that "with plenty of discussions still to go, Monday will be an important staging post on the road to the crucial December council."

For now, there seems to be agreements, in principles, on two of the three key issues already. It’s believed that May is going to offer between GBP 40b and GBP 50b for settling the divorce. And it’s reported that Irish officials and EU are optimistic on solving the problem of Irish border. But there are reports that EU MEPS are unhappy as the rights of EU citizens in UK post Brexit are being forgotten. The sticky point here is that EU is urged to insist that EU citizens rights in UK are being protected by the European Court of Justice. But this is firmly ruled out by May and UK politicians.

Looking ahead – RBA, BoC and NFP

RBA rate decision and Australian data will be closely watched. The central bank is widely expected to keep its cash rate unchanged at record low of 1.50% on Tuesday. Considering weak wage growth and lack of inflationary pressure, there is little push for a hike at the moment. On the other hand, there were even talks that RBA is in "cut" territory due to sluggish house price growth. According to CoreLogic data back in November, annual price growth mere stood at 5.2%, half of the peak of 10.4% back in May 2017. More importantly, the six month price growth stood at 0.7%. And in the past 30 years, 7 out of 9 times RBA cut interest rates as 6-month house price growth weakened to zero or turned negative. But of course, considering RBA’s high alertness on household debts, the central bank is also nowhere near a cut. Also to be released include retail sales, GDP and trade balance.

BoC rate decision is another key focus of the week. Despite last week’s stellar employment data, there is little chance for the central bank hike interest rate this time. Nonetheless, the strong job data would eased the worries that the two hikes this year were too aggressive. Going forward, giving the unknown outcome of NAFTA renegotiation, the central could likely hold their hands for a while. Governor Stephen Poloz would also want to see how the domestic economy absorbs the prior hikes. If the incoming data continue to show strength, BoC could act again in April or afterwards.

There are also other heavy weight data to be featured this week, including ISM services and non-farm payroll. These data shouldn’t derail Fed’s December hike and would instead affect the chance of the projected three hikes next year. UK will also release PMIs as productions.

Here are some highlights of the week ahead:

- Monday: Japan consumer confidence; Eurozone Sentix investor confidence; UK construction PMI; US factory orders

- Tuesday: UK BRC retail sales; RBA rate decision, Australia retail sales, current account; Eurozone services PMI final, retail sales, GDP revision; UK services PMI; Canada trade balance; US trade balance, ISM services

- Wednesday: Australia GDP; Germany factory orders; Swiss CPI; US ADP employment, non-farm productivity; BoC rate decision, Canada labor productivity

- Thursday: Australia trade balance; Japan leading indicators; Swiss unemployment rate, foreign currency reserves; German industrial production; Canada building permits, Ivey PMI; US jobless claims

- Friday: Australia home loans; China trade balance; Germany trade balance; UK productions, trade balance; Canada housing starts; US non-farm payroll, U of Michigan sentiment

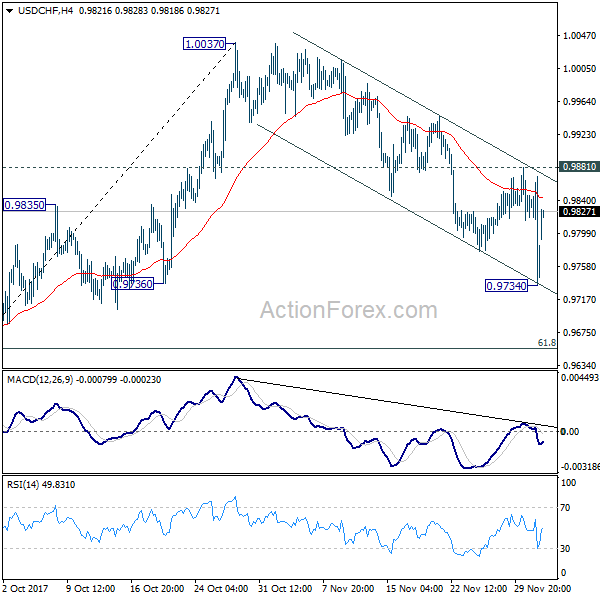

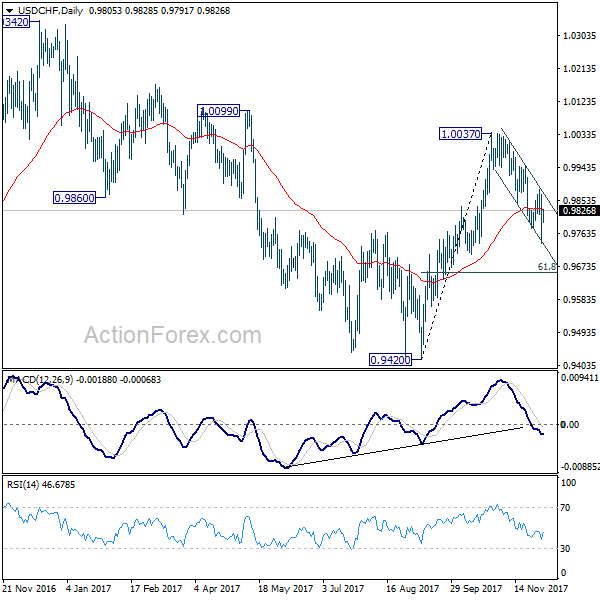

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9701; (P) 0.9786; (R1) 0.9836; More….

USD/CHF rebounds strongly today and intraday bias is turned neutral first. With 0.9881 minor resistance intact, deeper fall cannot be ruled out. Break of 0.9734 will target 61.8% retracement of 0.9420 to 1.0037 at 0.9656. Nonetheless, as choppy fall from 1.0037 is seen as a correction, we’ll look for bottoming again below 0.9656 and above 0.9420. On the upside, break of 0.9881 resistance will now indicate completion of the decline. And intraday bias will be turned back to the upside for 1.0037.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don’t expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Nov | 13.20% | 13.20% | 14.50% | |

| 0:00 | AUD | TD Securities Inflation M/M Nov | 0.20% | 0.30% | ||

| 5:00 | JPY | Consumer Confidence Index Nov | 44.9 | 44.5 | ||

| 9:30 | GBP | Construction PMI Nov | 51 | 50.8 | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Dec | 32.7 | 34 | ||

| 10:00 | EUR | Eurozone PPI M/M Oct | 0.30% | 0.60% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Oct | 2.60% | 2.90% | ||

| 15:00 | USD | Factory Orders Oct | -0.40% | 1.40% |