{kind=link}

Dollar’s rebound extends today as markets are awaiting FOMC minutes. The key to watch is any hint on the next move of Fed. That is, whether Fed will hike rates in September and start shrinking the balance in December, or reverse. Or, Fed would indeed do nothing in September. Currently, fed fund futures are pricing in less than 20% chance of a September hike. Also, odds for federal fund rates to hit 1.25-1.50% and above in December is less than 60%. Technically, the greenback is staying near term bullish against Yen. But Dollar is holding below near term resistance against Euro, Sterling, Aussie and Canadian, and stays bearish.

"Triple-whammy" of disappointing UK PMIs

In UK, Services PMI dropped to 53.4 in June, down from 53.8, and missed expectation of 53.5. Markit chief business economist Chris Williamson noted that "a slowing in services sector growth completes a triple-whammy of disappointing PMI survey readings." And while "the three PMI surveys are running at levels that are historically consistent with GDP growing by around 0.4% in the second quarter, it’s clear that the economy heads into the third quarter losing momentum." And he also said that it would be "surprise" to see BoE policy makers vote for a rate hike. And, "the current PMI reading would be more consistent with the Bank of England cutting interest rates rather than hiking." Also from UK, BRC shop price index dropped -0.3% yoy in June.

Nonetheless, markets still believed that BoE is closer than ever to have the first rate hike in the long time. The last time BoE raised interest rate was on July 5, 2007. Yes, that’s exactly 10 years ago. Back then, BoE raised the bank rate by 25bps to 5.75%, on 6-3 vote. Recent comments from BoE Governor Market Carney and chief economist Andy Haldane suggest that the central bank will discuss stimulus exit in the coming months. Other BoE hawks are maintaining their stance in recent speeches. MPC member Michael Saunders, who voted for a hike last month, said today that "households should prepare for interest rates to go higher at some point." Another hawk Ian McCafferty said in a newspaper interview that on the balance of monetary policy, "there is a need for change". And a rate hike would be "justified" and "the prudent thing to do at this stage".

Eurozone PMI – Not the start of a slowdown

Eurozone services PMI was finalized at 55.4 in June, revised up from 54.7. Germany services PMI was finalized at 54.0, revised up from 53.7. France services PMI was also revised up to 56.9, from 55.3. However, Italy services PMI dropped to 53.6 in June. Overall, Eurozone PMI composite dropped to 56.3, down from 56.8. Markit noted that "the dip in the PMI in June certainly doesn’t look like the start of a slowdown." And, "growth of new orders accelerated very slightly to reach the second highest in just over six years, and companies are struggling to satisfy this increase in demand."

ECB Governing Council member Benoit Coeure said today that "the Governing Council has not been discussing changes in our monetary policy that may come in the future." And recent market reaction to the hawkish comments from ECB President Mario Draghi was, according to Coeure, not very significant in the big picture. ECB chief economist Peter Praet said yesterday that ""underlying price pressures continue to be subdued." Praet called for patience regarding stimulus exit as "inflation convergence needs more time to show through convincingly in the data".

BoJ may lower inflation forecast this month

Reuters reported, quoting unnamed source, that BoJ will likely low inflation forecast for the current fiscal year ending March, 2018, in the upcoming meeting on July 19-20. And the inflation forecast for the next fiscal year might also be revised down. The sources noted that the economy was in good shape and BoJ might further upgrade the assessment. However, time is still needed for the positive effects to pus up prices. Nonetheless, the downward revision in inflation projections would possibly be minor, just reflecting recent softness in energy prices. At the April meeting, BoJ projected core inflation to hit 1.4% in the current fiscal year, and 1.7% in the next.

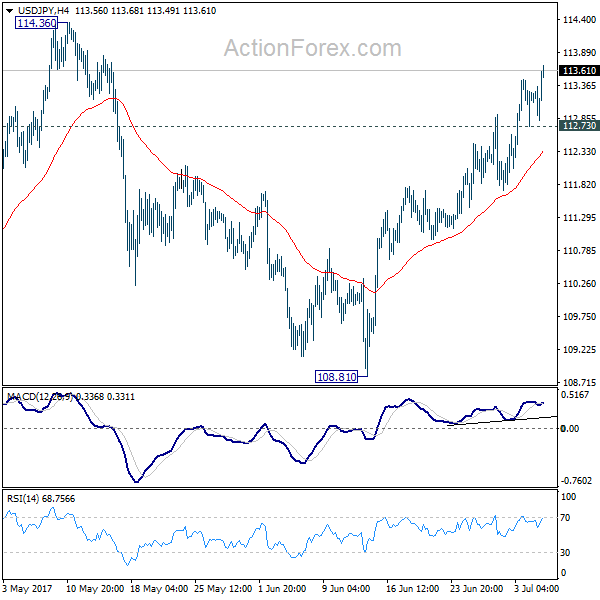

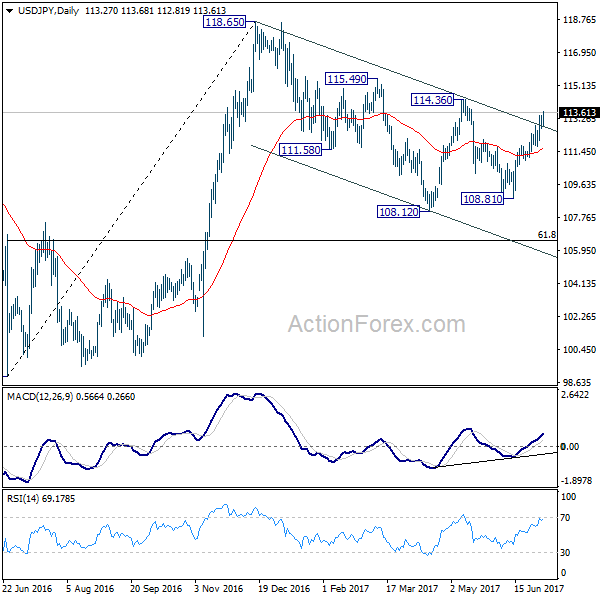

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.85; (P) 113.14; (R1) 113.57; More…

USD/JPY’s rally continues today and hits as high as 113.58 so far. Intraday bias remains on the upside for 114.36 resistance next. Decisive break there will confirm our bullish view that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65 next. On the downside, below 112.73 minor support will turn intraday bias and bring consolidation before staging another rally.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it’s uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it’s a leg in the consolidation from 125.85. Hence, we’ll be cautious on topping as it approaches 125.85.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | -0.30% | -0.40% | ||

| 1:45 | CNY | Caixin PMI Services Jun | 51.6 | 52.9 | 52.8 | |

| 7:45 | EUR | Italy Services PMI Jun | 53.6 | 54.6 | 55.1 | |

| 7:50 | EUR | France Services PMI Jun F | 56.9 | 55.3 | 55.3 | |

| 7:55 | EUR | Germany Services PMI Jun F | 54 | 53.7 | 53.7 | |

| 8:00 | EUR | Eurozone Services PMI Jun F | 55.4 | 54.7 | 54.7 | |

| 8:30 | GBP | Services PMI Jun | 53.4 | 53.5 | 53.8 | |

| 9:00 | EUR | Eurozone Retail Sales M/M May | 0.40% | 0.30% | 0.10% | |

| 14:00 | USD | Factory Orders May | -0.50% | -0.20% | ||

| 18:00 | USD | FOMC Meeting Minutes |