{kind=link}

Here are the latest developments in global markets:

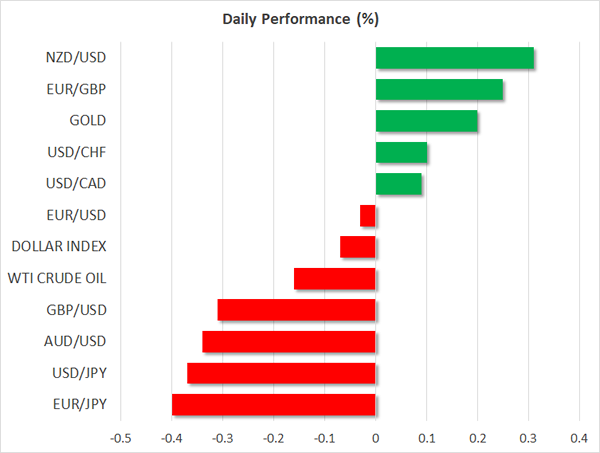

FOREX: The dollar weakened against its major counterparts on Wednesday as unless a deal is reached the government will run out of funds on Friday. This is spreading fears of a partial government shutdown. The pound was under pressure amid weakening hopes for progress on Brexit talks and on reports of a failed plan to kill the UK Prime Minister. The aussie tumbled in the wake of disappointing GDP growth figures and the kiwi surged to a one-week high.

STOCKS: There was a broad selloff in Asian equities following yesterday’s declines on Wall Street; the Nikkei 225 closed 2.0% lower and the Hang Seng was last down by 1.8%. Euro Stoxx 50 futures traded 0.8% lower at 0747 GMT. Dow futures were lower by 0.3%, S&P 500 contracts were down by 0.2% and Nasdaq 100 equivalents traded down by 0.4%.

COMMODITIES: Oil prices retreated after the API weekly report showed gasoline and distillate inventories in the US climbed unexpectedly. WTI crude fell by 0.33% to $57.43 per barrel and Brent declined by 0.24% to $62.70. Gold rose by 0.20% on the day to $1,268.30 per ounce but remained near four-month low levels.

Major movers: Dollar struggles as government budget deadline looms; aussie back to $0.75

US government agencies will run out of funds on Friday midnight unless a deal is reached, with Republicans postponing the planned House vote on the temporary budget – aiming to finance the government until December 22 – from Wednesday to Thursday to solve disputes with conservatives who desire a tighter budget. However, Republicans are said to push harder to pass the bill this week as they are also under pressure to address other issues by the year-end, including the tax overhaul bill. The dollar breached slightly below 112 yen, approaching a one-week low of 111.98 (-0.44%). Dollar/swissie retreated to a session low of 0.9856 but managed to erase losses afterwards, rising to 0.9870 and dollar/loonie retreated to 1.2700 (0.11%). The dollar index was steady at 93.31.

The euro remained flat around $1.1828 despite German factory orders in October surprising to the upside, while the pound was on a downtrend towards to $1.3400 (-0.33%).

Looking at the antipodean currencies, the aussie took a knock versus the greenback after the readings on Australian GDP growth indicated that the economy expanded by 2.8% y/y in the third quarter, below the forecasts of 3.0% but far above the previous mark of 1.8%. Household spending slowed down as well, narrowing to a multi-year low of 0.2% from 0.9% (upwardly revised from 0.8%) as heavily indebted consumers have to come tom terms with sluggish wage grwoth. Aussie/dollar tumbled close to a one-week low of 0.7570 (-0.34).

Its New Zealand cousin surged to a one-week high of $0.6915, being the best performer of the Asian session (+0.35%).

Day ahead: Bank of Canada rate decision, US ADP jobs report and EIA data the main focus

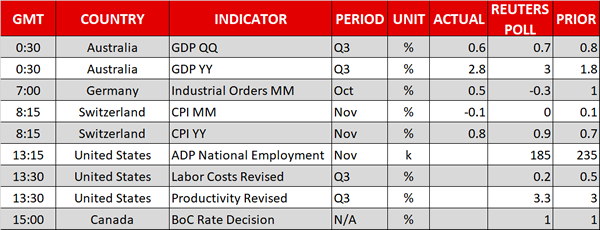

In a relatively quiet day in terms of releases, the November ADP national employment report out of the US will be released at 1315 GMT. This pertains to positions added to the economy by the private sector and is often perceived as giving an indication on the nonfarm payrolls report (due on Friday). Analysts expect the ADP report to show an addition of 185k positions. This compares to 235k in October. Shortly after (at 1330 GMT), data on third quarter US nonfarm productivity are due.

The Bank of Canada today completes its meeting on monetary policy with its decision on rates as well as the bank’s monetary policy statement being made public at 1500 GMT. No change in interest rates as expected though still the event will be closely watched for any market sensitive comments having the capacity to steer dollar/loonie as well as other loonie pairs.

The EIA’s weekly report on, among others, US crude and gasoline stocks will be released at 1530 GMT. Oil prices will be in focus with the release often causing volatility in prices.

Beyond data, deliberations on tax reform as well as on averting a government shutdown are continuing in the US, while in Europe, the European Commission College of Commissioners will be assessing whether sufficient progress has been made on Brexit discussions that would justify moving negotiations to the next step – that of the eventual future relationship between Britain and the EU.

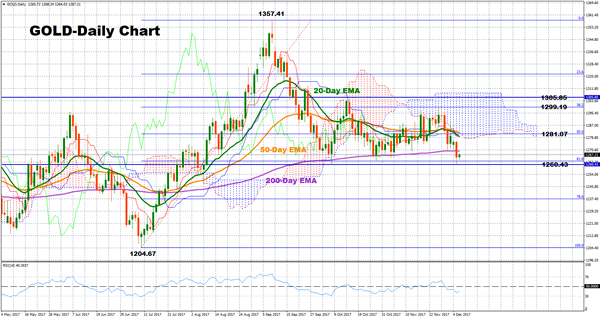

Technical Analysis: Gold breaks below 200-day EMA; neutral short-term bias

Gold has slid below the 200-day exponential moving average line (EMA) and is close to exiting the range-bound market between 1260.43 and 1305.85.

The neutral bias though remains intact in the short-term as the pair continues trading within the aforementioned range. Adding to this, the RSI has been in large part moving sideways in recent days.

However, if the ADP report out of the US beats expectations pushing the greenback higher, dollar-denominated gold could head down, reaching the lower bound of the range at 1260.43, which is not far below the 61.8% Fibonacci retracement (1262.94) of the upleg from 1204.67 to 1357.41. Further decreases could also meet the 1250 and the 1240 key-levels.

Alternatively, an upside move could face strong resistance at the 50% Fibonacci at 1281.07 before the focus shifts to a previous top at 1299.19, which is also the 38.2% Fibonacci of the previously mentioned upleg.