Summary

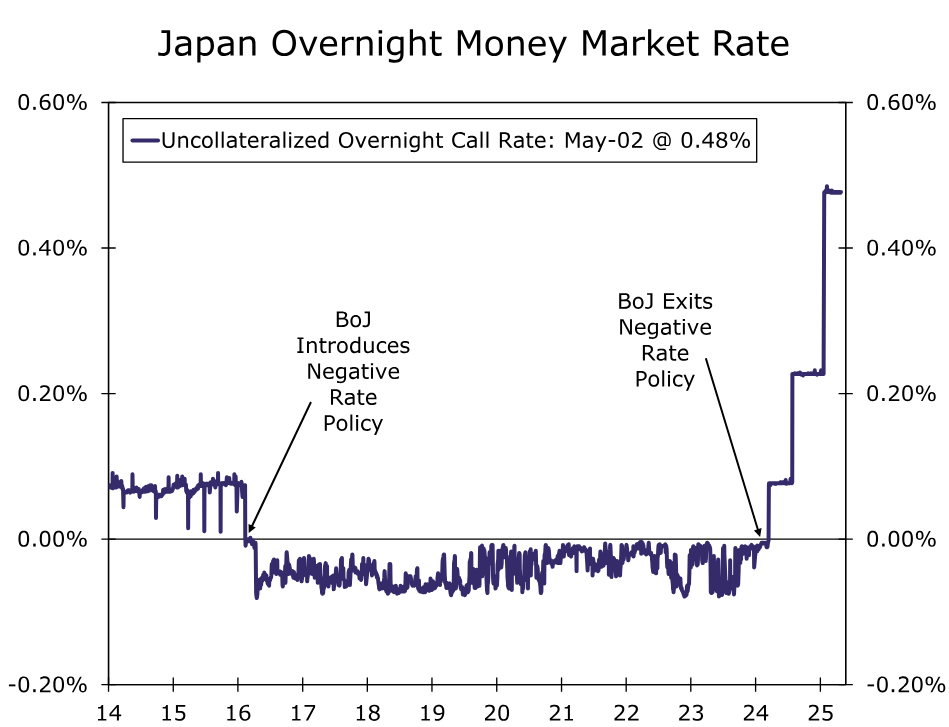

- In a widely expected decision, the Bank of Japan (BoJ) held its policy rate at 0.50% at this week’s meeting. Uncertainty around trade policy appears to be a key factor that kept BoJ policymakers on the sidelines this month, and dovish-leaning elements of the decision and updated economic forecasts suggest this rate pause may extend for a bit longer.

- In its updated projections, the BoJ downwardly revised its GDP growth and underlying inflation forecasts for fiscal years 2025 and 2026, and noted that risks for both economic activity and prices remain skewed to the downside. The central bank now sees the 2% inflation target being reached in FY2027 instead of FY2026. Comments from Governor Ueda were somewhat mixed, as he noted that a delay in the achievement of the price target does not necessarily mean a delay in rate hikes.

- Given this mix of a somewhat dovish-leaning policymaker stance, elevated uncertainty, but also recent encouraging wage and price growth data and our own more-optimistic view of GDP growth, we do forecast another BoJ rate hike, though expect it to now come later than we previously anticipated. We see the BoJ hiking its policy rate by 25 bps to 0.75% in October of this year. By that point, we suspect that policymakers will have more clarity around global trade policy and local economic growth and inflation developments.

- We see a gradual pace of yen appreciation against the dollar this year as the BoJ hikes while the Fed is cutting rates. However, around the turn of the year when the Fed concludes its easing cycle, U.S. growth improves and the BoJ is on hold, we expect to see renewed yen weakening against the dollar through late 2026.

Bank Of Japan Announcement Holds Steady Amid Uncertain Outlook

In a widely expected decision, the Bank of Japan (BoJ) held its policy rate at 0.50% at this week’s meeting. Uncertainty around trade policy appears to be a key factor that kept BoJ policymakers on the sidelines this month, and dovish-leaning elements of the decision and updated economic forecasts suggest this rate pause may extend for a bit longer. In the Outlook for Economic Activity and Prices, policymakers highlighted that Japanese economic growth is likely to moderate in the nearer-term before rising again in the medium term. In turn, during the period while economic growth is somewhat modest, this should lead to sluggish underlying inflation as well, before it gradually rises again later in the forecast horizon. The central bank also noted that risks to both its economic and inflation outlook are skewed to the downside for fiscal years 2025 and 2026.

In terms of the updated forecasts, policymakers notched up their Fiscal Year 2024 (April 2024-March 2025) real GDP forecast to 0.7% from 0.5% previously, but downwardly revised their projections for FY2025 and FY2026, to 0.5% (1.1% previously) and 0.7% (1.0% previously), respectively, citing changes in trade policy. The BoJ also introduced fiscal year 2027 into its forecast horizon, for which it projects real GDP growth to pick up further, to 1.0%. As for underlying price pressures (CPI ex-fresh food inflation), the BoJ kept its fiscal year 2024 forecast unchanged at 2.7% and revised its FY2025 and FY2026 forecasts down to 2.2% and 1.7%, respectively. For FY2027, the central bank sees CPI ex-fresh food inflation at 1.9%. In the accompanying commentary, officials noted that they see inflation reaching a level consistent with the 2% inflation target in the second half of the projection period, around fiscal year 2027. This marks a delay in the achievement of the price target as compared to the forecasts from January; those projections saw the target being achieved in FY2026.

In Governor Ueda’s press conference, he offered a somewhat more balanced tone in contrast to the policy statement. He began by acknowledging heightened uncertainties both concerning global trade policy and BoJ policymakers’ confidence that their economic projections will be realized. Ueda framed the forward-looking path for domestic inflation as one that would see more of a stalling before the 2% inflation target is sustainably achieved, but in notable remark, stated that a delay in the achievement of the price target does not necessarily mean that rate hikes will be delayed. In our view, his press conference comments appeared to balance a somewhat dovish economic outlook while also maintaining a degree of policy flexibility.

It appears that market participants interpreted the statement and accompanying comments as somewhat dovish-leaning, as the yen weakened noticeably against the dollar, to around the 145 per dollar mark after hovering between 142.50-143.00 per dollar yesterday prior to the announcement.

As we will detail in the remainder of this report, while we do see some economic reasons that further BoJ tightening can be delivered, the dovish tilt of the commentary and forecasts has led us to see policymakers waiting until October of this year to raise the policy rate by 25 bps, in order to wait to gain more clarity on the developments of global trade policy and the domestic economic growth and inflation outlook.

Wage and Price Trends Still Supportive of Eventual Further Bank of Japan Tightening

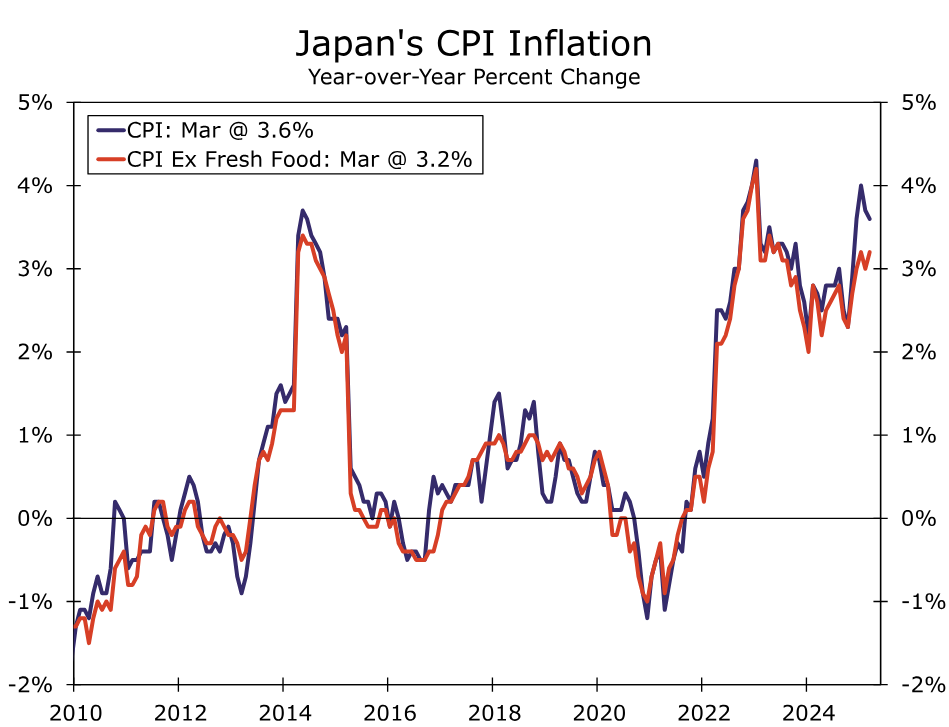

Regarding recent economic news, both wage and price growth developments appear to be consistent with additional BoJ tightening, in our view. Inflation has been above the central bank’s 2% target for quite some time now, and while readings from 2024 saw price growth slowing closer to the 2% mark, national CPI inflation popped again around the turn of the year. March CPI inflation came in at 3.6% year-over-year, and the underlying measure—which excludes fresh food—has been gradually accelerating in recent months and printed at 3.2% in March. We will see the release of the April national CPI report toward the end of May. In the meantime we received the Toyko CPI inflation figures for April, which surprised to the upside.

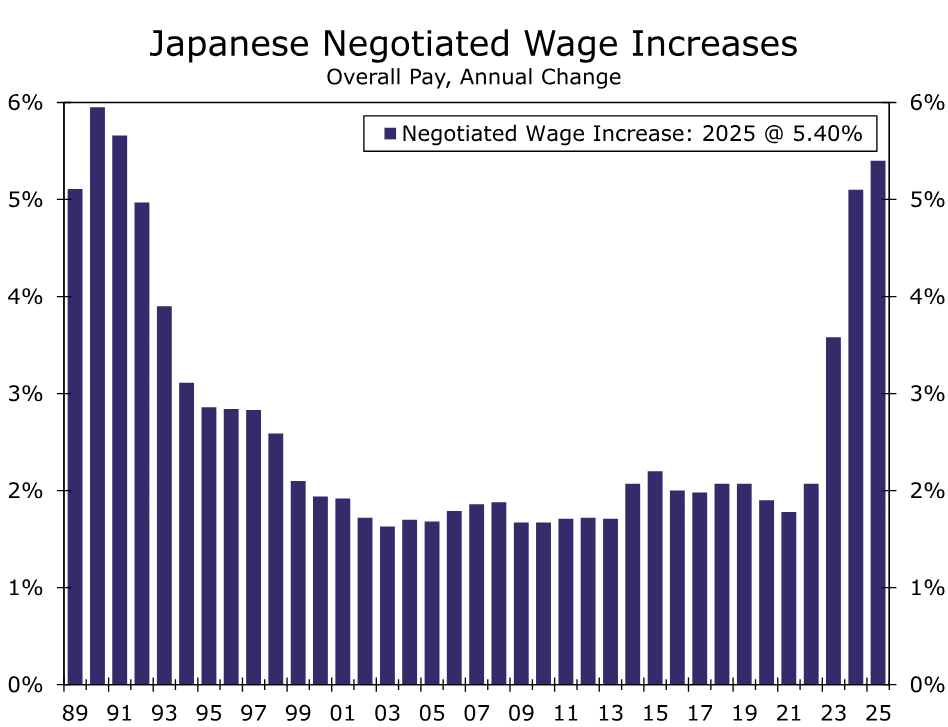

Given that Bank of Japan policymakers have long highlighted the desire for a “virtuous cycle” between wages and prices to take hold in order to help the economy to sustainably achieve on-target inflation, it is also important to consider recent trends in wage growth. Early results from this year’s spring wage negotiations have generally been encouraging, with Rengo—Japan’s largest group of labor unions—reporting their latest tally of an average wage increase of 5.4% year-over-year for its members, which is noticeably elevated by historical standards. The final tally from this year’s negotiations has not yet been released, but it appears that the momentum seen last year—for which the final tally was 5.1%—remains. Last year’s reading was the highest since the early 1990s. Looking into monthly labor earnings data, which are more backward-looking, the picture is somewhat mixed. Headline labor cash earnings growth has been reasonably solid, coming in at 2.7% year-over-year in February. Real earnings growth was negative in January and February, following two months of positive growth at the end of last year. Measures that examine the same sample base of workers from month-to-month also appear to be of interest to BoJ policymakers. Earnings growth for all workers in this group came in lower than expected in both January and February, though the readings are still elevated by historical standards. While within the details of the monthly wage growth data there may be some signs that the momentum is somewhat uneven, we believe that price and wage growth trends as of late are overall consistent with an additional BoJ rate hike.

Growth Trends Mildly Encouraging Overall, Though Risks Remain

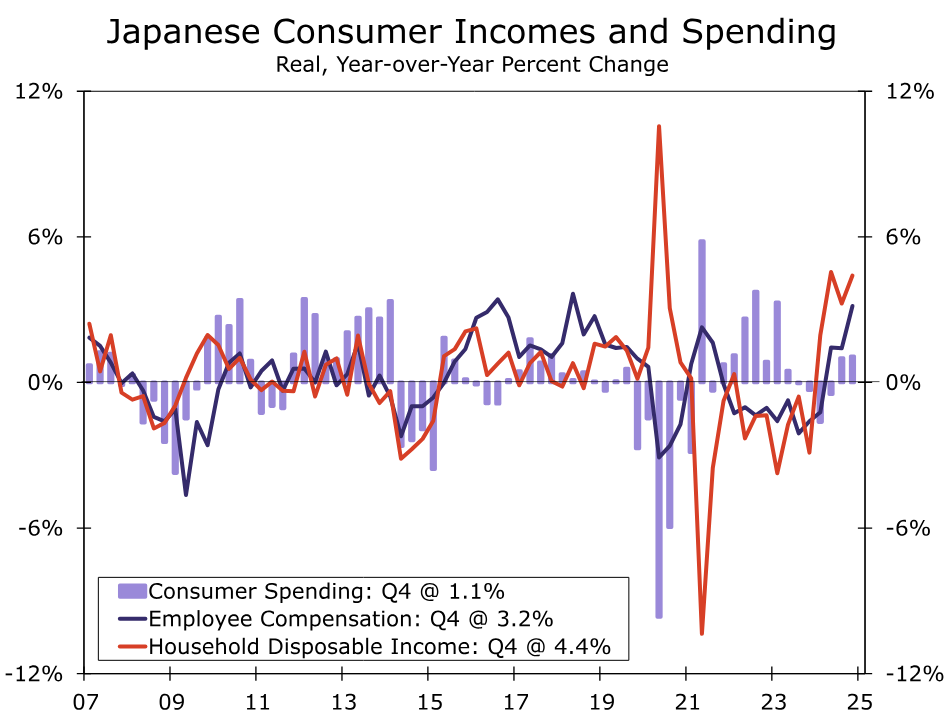

Turning to the growth outlook, recent activity data and sentiment surveys have shown some mildly encouraging signs, suggesting Japan’s economy was in a reasonable position ahead of the U.S. tariff announcements in early April. While we don’t view these growth trends as providing a decisive argument for further Bank of Japan tightening, nor do we view recent trends as a significant impediment to further rate hikes. Looking first at GDP growth, Japan’s economy grew 2.2% quarter-over-quarter annualized in Q4-2024, and, indeed, has shown steady growth over the past three quarters. During that time, both consumer spending and business capital spending have enjoyed perceptible gains. In another encouraging development, income trends have also firmed in recent quarters, reflecting wage gains as well as the government’s tax cuts and income support measures. For Q4-2024, real household disposable income rose 4.4% year-over-year and real employee compensation rose 3.2%, both outpacing the 1.1% growth in consumer spending. Those firming income trends suggest that Japan’s consumer can continue to support the economy in 2025.

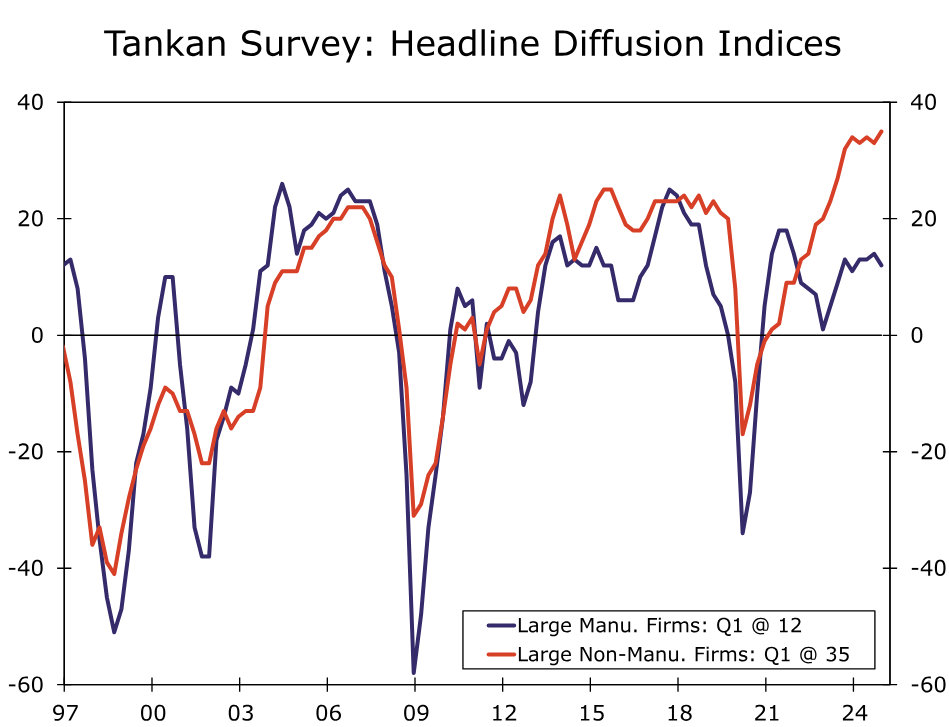

We also see indications that Japan’s economic growth held up through at least the first quarter of this year. Notably, the Q1 Tankan survey was relatively upbeat. The large non-manufacturers’ diffusion index rose 2 points to +35, while (perhaps not surprisingly, given the threat of tariffs) the large manufacturers’ diffusion index fell 2 points to +12. Both indices, however, remain at relatively elevated levels. In another promising development, Japan’s April Purchasing Managers Indices—one of the first post-tariff-announcement indicators—also showed improvement. The April manufacturing PMI edged up to 48.7, while the services PMI rose more noticeably to 52.2. As a result, the composite, or economy-wide, PMI moved into expansion territory at 51.1. While we would seek to avoid over-interpreting the gains seen in the April PMIs, at a minimum we think it is something of a relief that sentiment did not slump sharply following the tariff announcements.

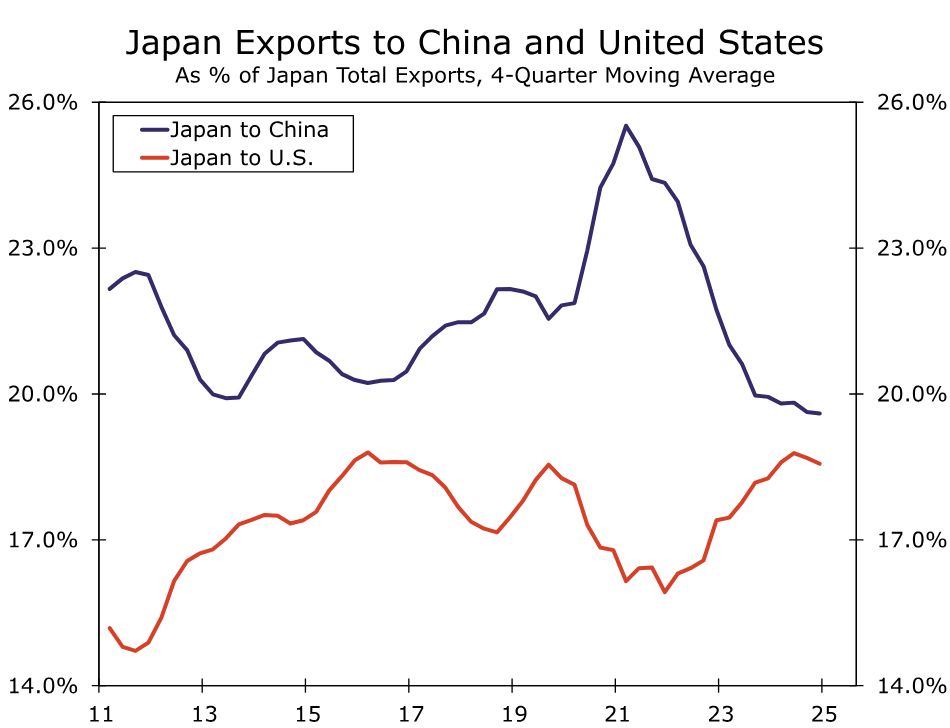

Of course, some question marks remain regarding Japan’s economic prospects, in particular a weaker outlook for two of Japan’s key trading partners, China and the United States. While exports to China have decreased a bit in importance in recent years, China still accounted for around 19½% of Japan’s total merchandise exports in 2024. On the other hand, exports to the United States have increased in importance in recent years, accounting in 2024 for around 18½% of merchandise exports. With both U.S. and Chinese economic growth expected to be noticeably slower in 2025 and 2026 amid heightened global trade tensions, Japan’s export sector appears likely to come under some pressure as this year progresses.

The increasing prominence of the United States as a trading partner for Japan also highlights the importance of Japan and the U.S. reaching some kind of agreement on trade in the months ahead. The United States announced a “reciprocal tariff” of 24% on imports from Japan in early April, although that rate has been temporarily been reduced to a 10% floor during a 90-day reciprocal tariff pause. To the extent that Japan and the United States can, during that time, reach a full trade agreement—or perhaps, more likely, a framework to continue trade negotiations—that allows for U.S. tariffs on imports from Japan to remain at 10% or lower, that would clearly be beneficial for the Japanese economic outlook. Finally, there have been mixed news reports on whether Prime Minister Ishiba is considering a new economic package at this time to help absorb the impact of tariffs. To the extent that any such package is pursued it would, at the margin, help Japan’s growth outlook. Taking into account the growth momentum around the turn of the year, potential disruptions from tariffs, and the possibility of government support measures, our base case forecast envisages Japanese GDP growth of 1.2% in 2025 and 0.9% in 2026. While, similar to the Bank of Japan, we acknowledge there are some downside risks to the growth outlook, in our view the economy’s momentum still appears solid enough to eventually elicit further Bank of Japan tightening.

Overall, taking into account the combination of a slightly dovish-leaning BoJ annoucement, along with what we view as overall encouraging wage and price trends, and our own outlook for Japan’s economic growth to maintain a reasonably steady pace, we do expect another BoJ rate hike, but we also expect it will be some time before that tightening is delivered. In the interim, we antcipate policymakers will wait as they seek a bit more clarity on trade tensions and local economic conditions. To that point, we have pushed back our expected rate hike timing to October, from July previously. We forecast a 25 bps rate hike at their October meeting, to reach a rate of 0.75%, in what we expect will be the final rate hike for this year. Our view of a BoJ rate hike in contrast to several Fed rate cuts later this year should still translate to yen appreciation, albeit likely only at a gradual pace, against the dollar over the remainder of this year. Around the turn of the year, however, as the U.S economy likely recovers and Fed easing comes to an end, we expect the yen could show modest renewed weakening through much of 2026.

held its policy rate at 0.50% at this week's meeting. Uncertainty around trade policy appears to be a key factor that kept BoJ policymakers on the sidelines this month, and dovish-leaning elements of the decision and updated economic forecasts suggest this rate pause may extend for a bit longer.){kind=link}