- Gold has been the biggest gainer year-to-date.

- Dovish Fed bets after soft NFP benefited the metal.

- Higher tariffs could increase safe-haven demand.

- Central bank purchases are also a driving variable.

Rise and shine

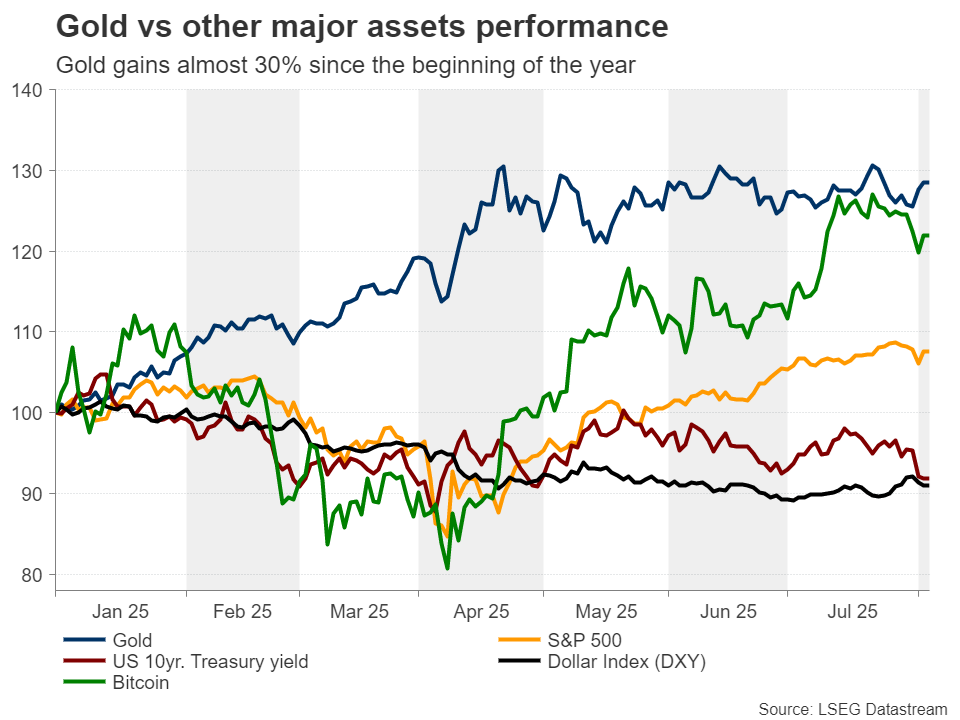

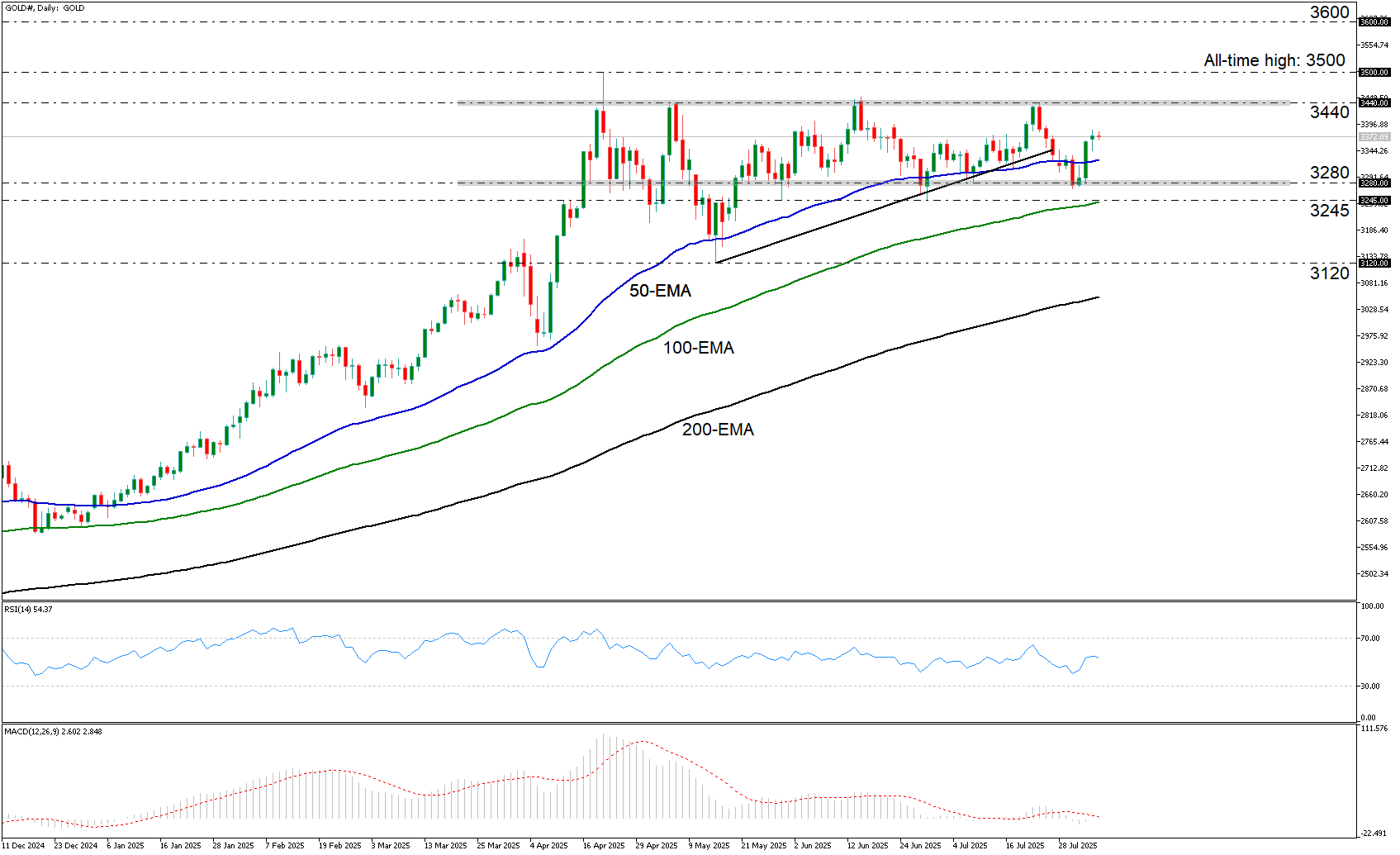

Gold has been the biggest performer among the major assets under our radar since the beginning of the year, outperforming even the crypto king Bitcoin. Although it has been range-bound since it hit a record high of $3,500 in April, investors still have the opportunity to lock profits of around 30% this year.

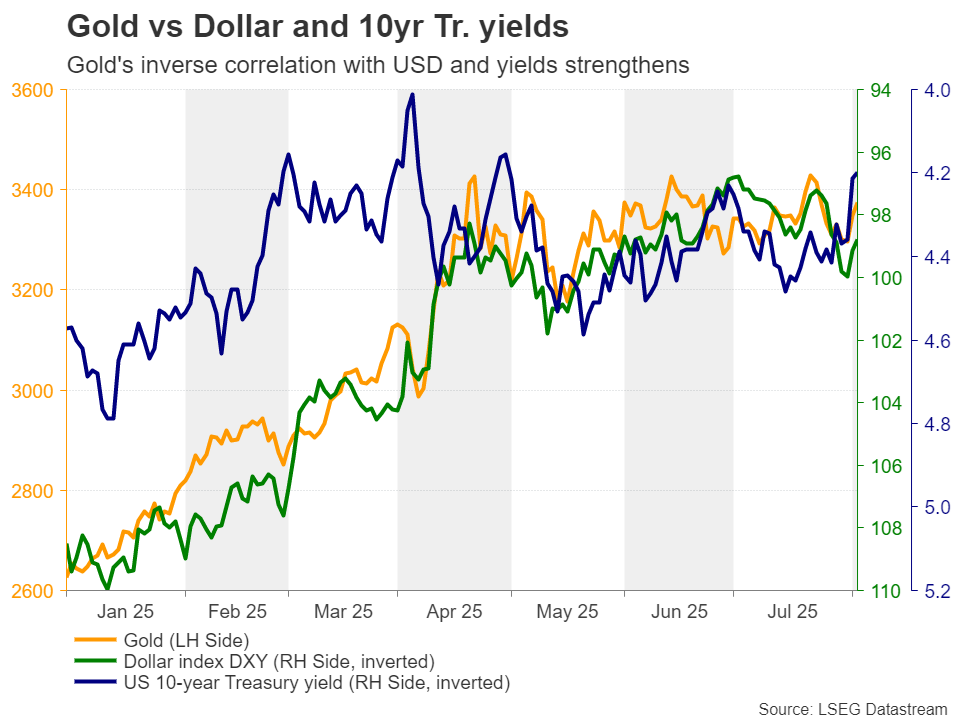

On Friday, the precious metal rebounded strongly from around the $3,280 zone after the US nonfarm payrolls for July disappointed, increasing speculation that the Fed may need to cut interest rates more aggressively than previously thought. As gold’s correlation with the US dollar and Treasury yields has strengthened in the last three months or so, the slide in the greenback and borrowing cost allowed gold to spike higher as the opportunity cost for holding the precious metal declined.

Opportunity cost falls amid dovish Fed bets

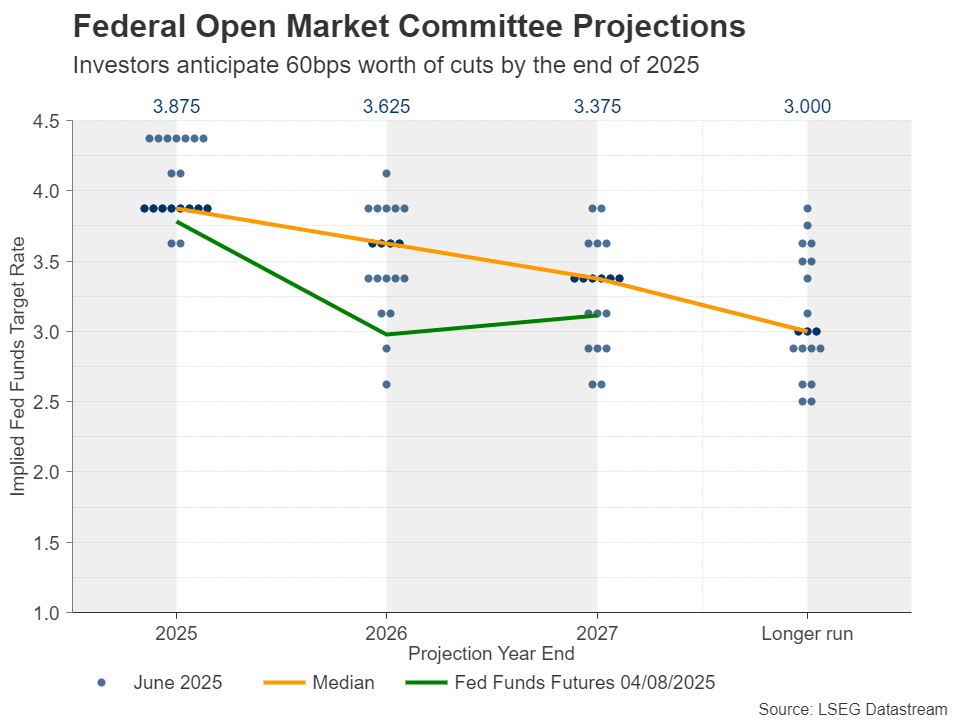

In terms of Fed expectations, according to Fed funds futures, a September quarter-point rate reduction is now nearly fully priced in, despite Fed Chair Powell reiterating his wait-and-see approach at the latest FOMC decision, at a time when investors were penciling only a 60% chance of a September rate reduction. As for the total number of basis points expected to be cut by year end, it rose from 45 to 60, suggesting that the market has once again turned a bit more dovish than the Fed itself.

This means that should US data continue to disappoint, dovish bets are likely to increase, allowing gold to extend its recovery and perhaps resume its prevailing uptrend.

Are gold traders “tarrified”?

But what could be the catalyst for a deteriorating US outlook? The answer is: Tariffs. On August 1, which was the deadline for the grace period regarding reciprocal tariffs, Trump announced steep duties on imports from dozens of countries, with the rates ranging from 10% to 41%. The levies are set to kick in on August 7, with a 35% tariff on Canadian goods already in effect.

Yes, ahead of the August 1 tariff deadline, the dollar was acting as a safe haven, gaining ground when Trump was hardening his stance, and pulling back on easing tensions. However, although the US secured deals with some of its major trading allies, like the UK, Japan and the EU, the massive duties announced on Friday heighten not only the upside risks to US inflation but also add to concerns about the performance of the global economy. Thus, should upcoming US economic releases revive recession fears, the US dollar could extend its tumble on speculation that the Fed may prioritize safeguarding economic activity even if that means allowing inflation to run hot for a while longer. Gold could benefit from that, as well as from increasing safe-haven demand amid heightened uncertainty.

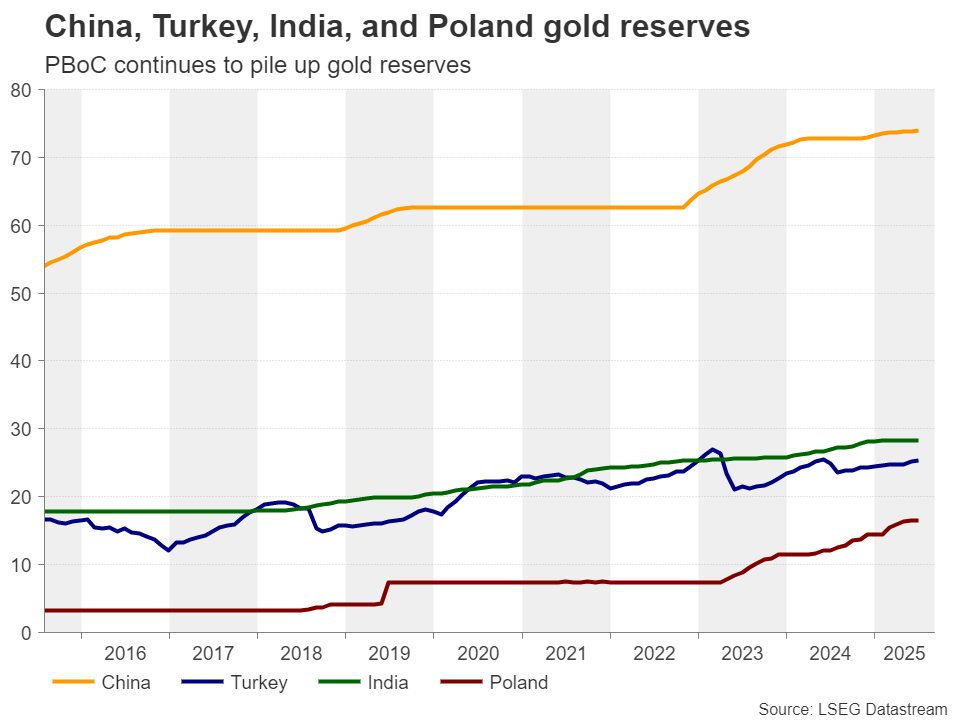

Central bank demand increases in June

Besides the Fed and Trump’s tariffs, another variable that needs to be examined are central bank purchases, especially from the People’s Bank of China (PBoC). The latest data available is for the month of June and although outdated, it is revealed that demand saw a modest increase for the third consecutive month. Back then, the deadline for finding common ground with the US was July 9 and perhaps central banks rushed into gold in order to further loosen their dependency on the US dollar should things fall out of orbit.

From here onwards, the spotlight falls on the PBoC as the world’s two largest economies failed to agree on extending a 90-day pause on tariffs during the latest round of talks in Stockholm, Sweden, last week. The deadline for a US-China trade deal is August 12, and should no common ground be found until then, tariffs could surge above 100% again. A new full-blown trade war between those two economic powerhouses could prompt Chinese officials to resume the selling of US Treasuries in favor of buying gold.

Gold rebounds, but stays range-bound for now

From a technical standpoint, gold rebounded from near the $3,280 zone on Friday, which has been acting as the lower boundary of the sideways range that’s been containing most of the price action since May 20. The upper bound is around $3,440 and since the price is still within the range, the near-to-medium-term outlook remains neutral.

For the prevailing uptrend to resume, a break above $3,440 may be needed. Such a move may initially target the record high of $3,500, hit on April 22, the break of which could aim for the next round figure of $3,600. On the downside, a break below the lower bound of the range at $3,280 could initially aim for the $3,245 barrier, marked by the lows of May 29 and June 30. A move lower could intensify speculation about a bearish trend reversal.

{kind=link}