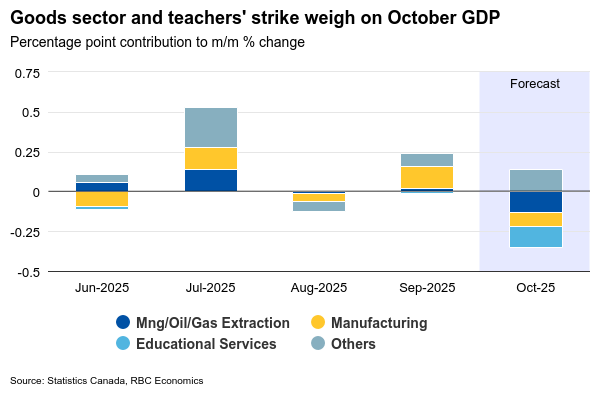

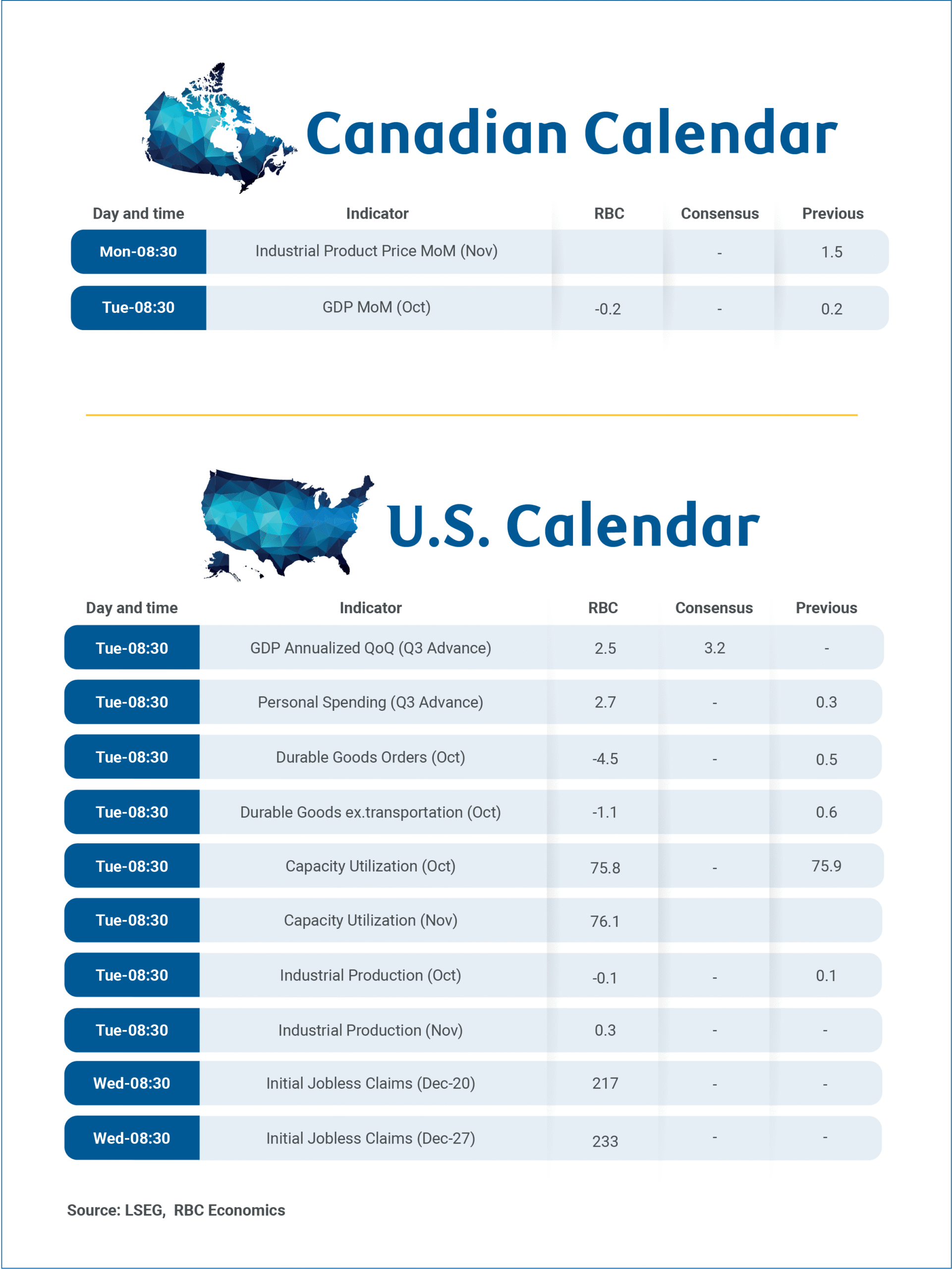

Canada’s gross domestic product report for October on Tuesday will mark Statistics Canada’s final major data release of 2025, and we anticipate a 0.2% decline in growth.

It’s slightly higher than StatsCan’s preliminary estimate released a month earlier for a 0.3% contraction. If October’s decline is realized, it would represent the steepest monthly drop in GDP since February.

Still, early indicators such as hours worked and our tracking of consumer spending suggest a possible recovery in November. We continue to expect a soft 0.5% annualized increase in GDP for Q4.

In October, we see weakness mostly from goods-producing sectors, while output among service industries remained essentially unchanged.

Non-conventional oil production in Alberta contracted sharply (-5%) in October after four consecutive months of expansion. Manufacturing output declined as well, partially reversing September’s gains. StatsCan’s October mineral production data indicated modest recovery in mining output, following declines in the prior two months, helping to cushion some weaknesses in other sectors.

For services, home resales rose 0.8% month-over-month in October, bolstering real estate activity. Arts and entertainment saw a boost from the Blue Jays’ playoff run, although the gain was likely reversed quickly in November. Offsetting stronger activities was the Alberta’s teacher strike temporarily weighing on education services. Wholesale and retail volumes also fell, by 0.7% and 0.6% respectively.

Early November indicators suggest signs of stabilization. Hours worked increased a larger 0.4%, and our tracking of RBC consumer spending data indicates continued strength, especially in discretionary purchases as the holiday shopping season ramps up. This is consistent with StatsCan’s advance retail indicator, which shows sales rebounded by 1.2% in November. Overall, we continue to expect modest growth in Q4.

Week ahead data watch:

Delayed Q3 U.S. GDP report will be released on Tuesday after the U.S. government shutdown. We look for headline GDP growth of an annualized 2.5% quarter-over-quarter—a deceleration from Q2’s 3.8%. Much of Q3’s expansion was driven by household consumption, particularly within services. Excluding volatile net trade, final domestic demand likely remained resilient, albeit growing slightly slower than in Q2.

{kind=link}