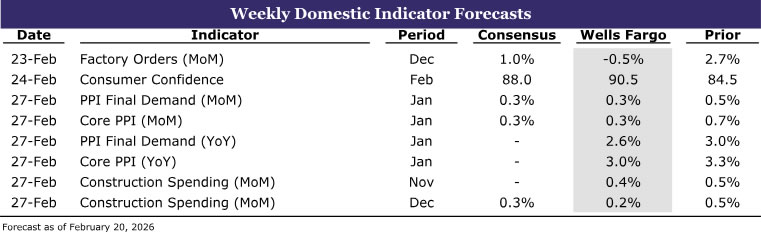

Summary

U.S. Week in Review:

- This week’s data delivered a familiar theme with an important twist. The U.S. economy continues to be shaped by powerful forces in high-tech and AI-related investment, but recent releases suggest the growth story may finally be broadening. At the same time, trade flows are moving in a less supportive direction, reminding us that not all parts of the economy are pulling in sync.

U.S. Week Ahead:

- Consumer confidence likely rebounded modestly in February after January’s decade low as cooler inflation and a better jobs report offered relief, even as high living costs and geopolitical risks persist.

- Construction spending likely improved at year-end, though we expect the results to be mixed beneath the surface, with data center construction driving strength but continued weakness in residential and structures investment expected as high interest rates and economic uncertainty continue to constrain activity.

U.S. Week in Review

Broadening Drivers of Growth: Unpacking GDP and Looking Ahead

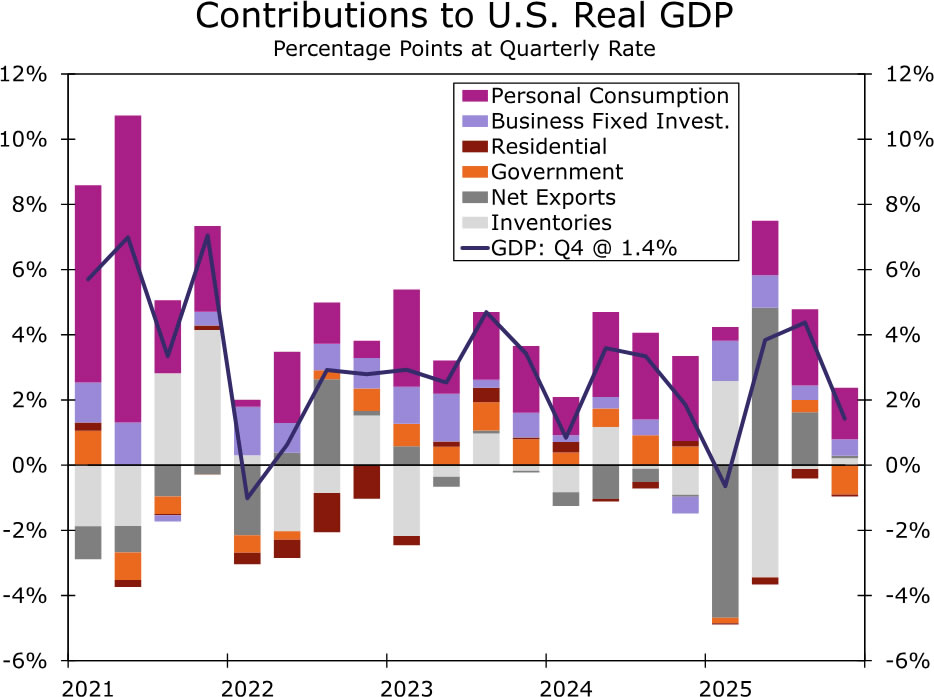

We had maintained a well-below consensus forecast for fourth quarter GDP and the official release this morning confirmed our suspicions that a government shutdown and a gold-excluded trade balance held back broader growth during the period. The annualized rate of GDP came in at just 1.4%, roughly half the 2.8% growth rate expected by the consensus.

Government spending, negatively impacted by the longest-ever shutdown, pulled growth lower by nine-tenths of a percentage point (chart). Net exports added less than a tenth of a percentage point (0.08) to the headline figure. Both commercial and residential fixed investment were slight drags during the fourth quarter as well.

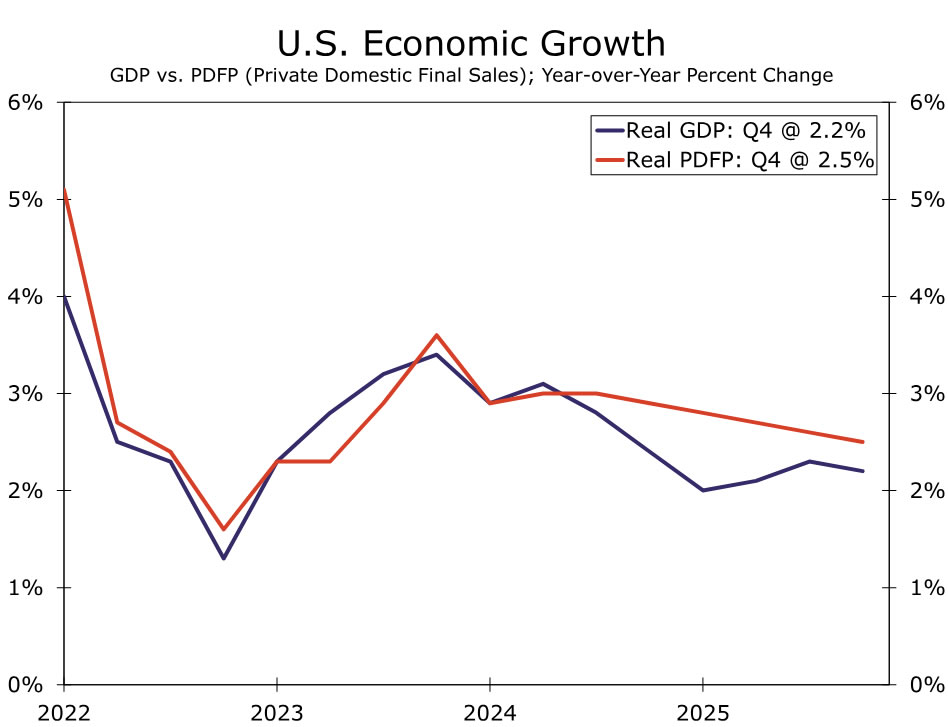

The growth drivers were largely consumer (which boosted growth 1.6 percentage points) and business fixed investment spending (which added 0.5 percentage points, even after accounting for the drag from structures). In terms of underlying U.S. growth, it was strong. We’ve emphasized this measure a lot throughout 2025: real final sales to private domestic purchasers, which removes government, inventories and net exports, the most volatile components this year. That measure was up at a 2.4% annualized clip in Q4 and 2.7% for the full year, only slightly below the pace registered last year, demonstrating a more stable growth picture (chart).

In plain English: If you exclude trade volatility and the associated impact on inventories, the overall economy is doing about the same as last year. Yet, for much of that period, resilience in business investment has been more optical than organic—a surge in AI and high-tech spending masking softness elsewhere. Orders, production, and imports tied to computers, communications equipment, and semiconductors have surged, while more traditional capital goods struggled to keep pace. This was true in Q4 as well where the 3.2% annualized pickup in real equipment investment was due entirely to stronger investment in information processing equipment, while other areas of capex (industrial, transportation, other) declined.

December durable goods orders and January industrial production also released this week hint that this imbalance may be starting to ease. Core capital goods orders stabilized, and shipments rose at a pace consistent with solid equipment investment growth. Stripping out the notoriously volatile aircraft category reveals modest but broad-based gains across most durable goods sectors, enough to handily exceed low expectations.

On the production side, manufacturing output rose at the fastest monthly pace in nearly a year. While high-tech continues to dominate in level terms, output excluding high-tech also posted its strongest gain in almost 12 months, reaching its highest index reading in more than two years. In short, the AI investment boom remains intact, but it is no longer the only game in town.

Supportive tax incentives and an early year pickup in commercial and industrial lending appear to be encouraging firms to finance projects beyond AI infrastructure. That shift matters: A more balanced capex cycle would make the expansion more durable and less dependent on a single sector carrying the load.

If investment and production offered a positive signal, trade delivered a counterweight. December saw a sharp widening in the trade deficit, driven by a large increase in imports alongside a decline in exports. On the surface, that combination pointed to a meaningful drag on fourth quarter growth. But digging deeper tempers the headline. More than half of the widening was due to non-monetary gold flows, which are excluded from GDP calculations and reflect asset reallocation rather than underlying production demand. Adjusting for gold significantly reduces the apparent deterioration in net exports, thus explaining the flat contribution to headline Q4 growth.

The trade data also underscore how much last year’s import weakness may have been overstated. Goods imports finished 2025 well below where they began the year, particularly outside of high-tech categories, but the evidence points more toward caution than capitulation. Firms appeared to adopt a wait-and-see approach amid tariff uncertainty rather than execute a wholesale restructuring of supply chains.

With inventories lean and little sign of large scale onshoring, there is scope for imports to rebound modestly this year—even if tariff rates remain elevated. Ongoing legal and policy uncertainty around tariff authority, as well as upcoming reviews of trade agreements, means trade policy will remain a swing factor, but not necessarily an ever-tightening constraint.

At the end of the day, consumers are still spending. Real personal consumption expenditures advanced at a 2.4% annualized rate in Q4, driven by solid services-sector demand, which offset a modest pullback in goods purchases. If you’re looking for a sign of caution in the GDP data, we’d highlight the fact that the services resilience looks to be driven by non-discretionary categories like healthcare, housing & utilities and financial services. The more discretionary-oriented areas (transportation, recreation and food & accomodation) all lagged or posted modest growth rates. That development doesn’t leave us overly concerned of a consumer pullback as we’ve cautioned of a soft finish, but it signals some stress in the consumer sector. We expect more favorable after-tax income growth and larger average tax refunds to help offset some of this household pressure this year.

Taken together, this week’s indicators tell a nuanced story. Beneath the noise, there are early and encouraging signs that investment and production growth are becoming more broad based, reducing the economy’s reliance on the high-tech sector alone. At the same time, trade is shifting from a big tailwind to a mild headwind for growth as imports normalize.

The message is not one of reversal, but of rebalancing. Momentum within the domestic economy is improving in a healthier way, even as external dynamics complicate the growth arithmetic. As we look ahead, the sustainability of the expansion will hinge less on a single sector’s boom and more on whether this nascent broadening continues to take hold.

U.S. Week Ahead

Consumer Confidence • Tuesday

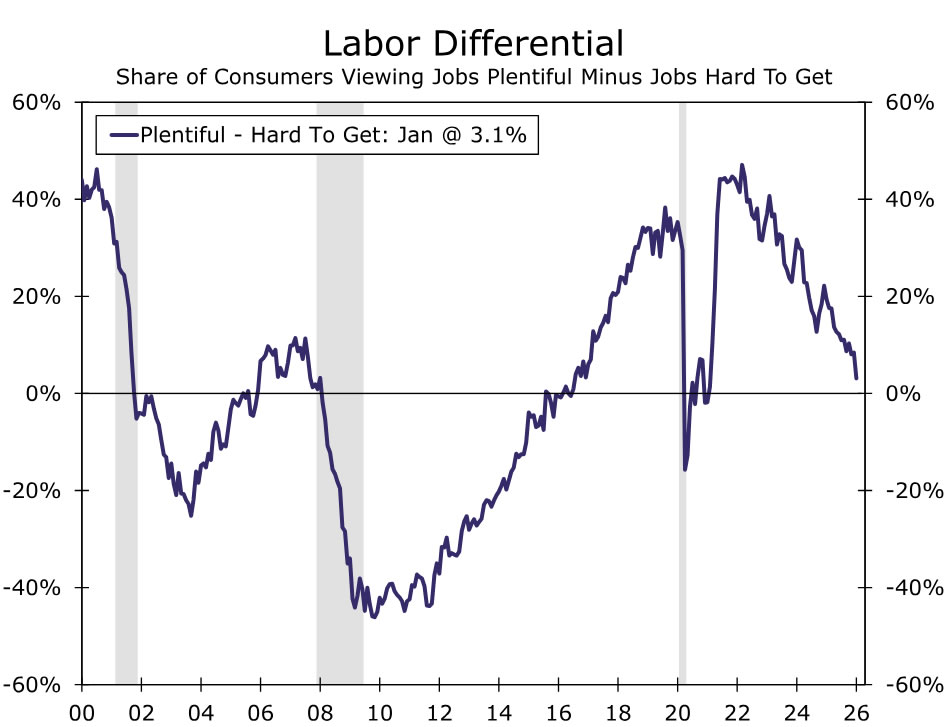

The Consumer Confidence Index fell to its lowest level in a decade in January, with a deterioration in the labor market, high living costs and geopolitical tensions contributing to the drop. The weakening jobs backdrop is particularly weighing on household sentiment: The labor differential fell to a post-pandemic low, with more consumers reporting jobs as “hard to get.” While this alone is not enough to stop households from spending, it does result in more cautious spending behavior, especially for those with less discretionary income.

We look for a bit of payback in February’s print and expect the index to rise to 90.5 from 84.5 previously. Though the labor market is far from perfect, the employment report for January was broadly encouraging, which will likely provide some relief to consumer’s weakening views of the labor market. Likewise, the CPI report came in cooler than expected in January, which may also provide support to consumer confidence. That said, despite the more-positive month of data, persistent worries of tariffs, foreign interventions and high cost of living are likely not going away soon and will continue to weigh on consumer confidence.

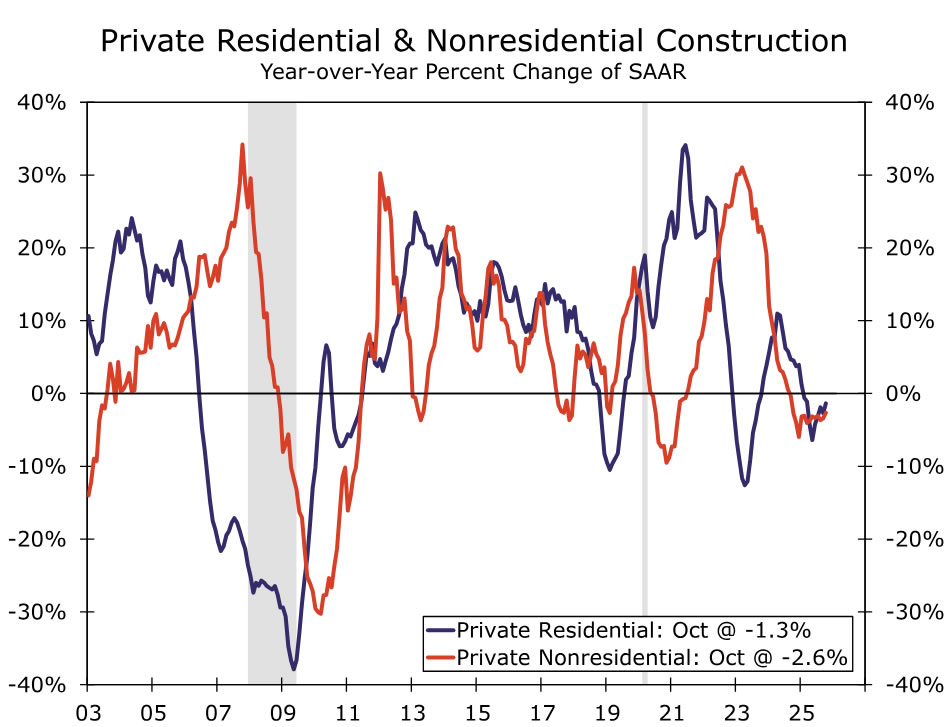

Construction Spending • Friday

Construction spending declined 0.6% in September before rebounding 0.5% in October, making overall construction spending virtually unchanged since August. Private construction was the main drag, with residential and nonresidential outlays both declining on an annual basis. Single‑family residential spending fell sharply as builders pulled back amid high mortgage rates and elevated inventories, while at the same time manufacturing, commercial and healthcare construction also weakened. Multifamily spending stabilized after earlier declines, and public construction outperformed, rising year-over-year on gains concentrated in education, water and waste projects.

November and December construction spending data will be released next week, and we look for modest monthly increases of 0.4% and 0.2%, respectively. While there remains room for growth in areas such as data center construction, we look for continued near-term weakness in residential and structures investment as high interest rates and economic uncertainty continue to constrain activity.

{kind=link}