Between our FAQ with the team and our note on what it would take to have a serious conversation about recession, we have tossed a lot at you over the last week related to the conflict with Iran. Let us provide just a bit more context around some of the numbers we’ve been talking about.

The reality is the U.S. economy is less sensitive to higher energy prices than it once was. In the note we penned on recession risks we referenced our model simulations that suggest a sustained 50% rise in oil prices would reduce the average annual growth rate of real personal consumption expenditures (PCE) by around one percentage point. But consider this. We estimate that same 50% sustained rise in prices would have had about twice the effect back in the 1980s, lopping off around two percentage points off PCE growth. In other words, back then, talk of recession would already be gathering steam, all else equal.

The country was highly energy-sensitive then, heavily reliant on imported oil and far more exposed to sudden increases in energy costs. Higher prices translated quickly into weaker real income growth, reduced consumption and slower top-line economic activity.

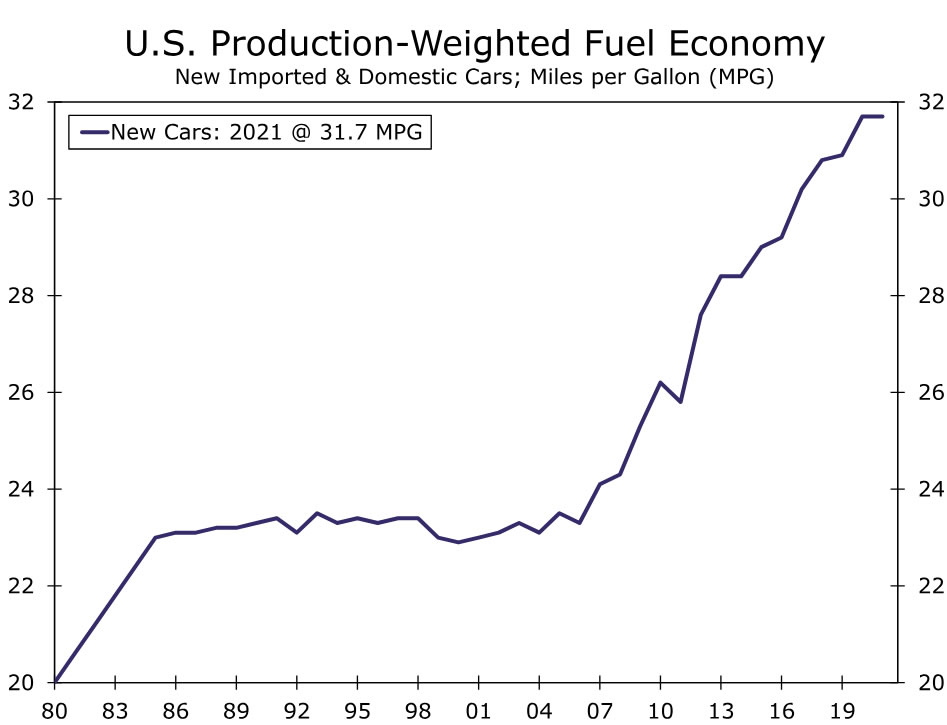

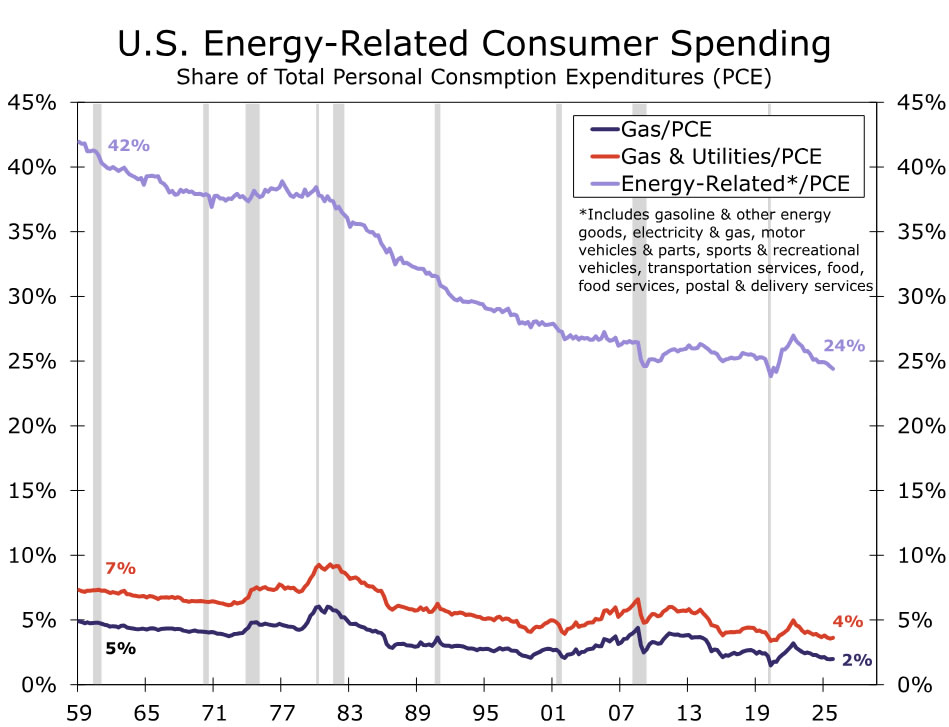

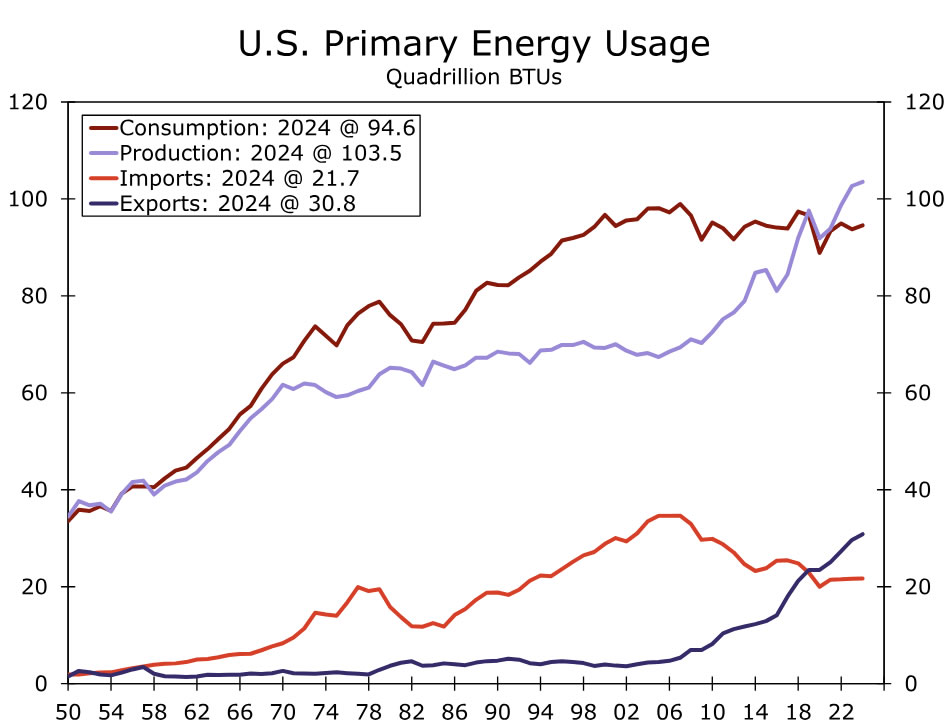

Things are different today. For starters, we are far more energy efficient. Back in the 1980s new cars averaged about 20mpg compared to today’s 32mpg (Figure 1). Second, Households are earning more too; gasoline and even broader energy-related purchases make up a smaller share of household spending today then they once did (Figure 2). And third, the U.S. also produces more domestically meaning it is less reliant on foreign supply (Figure 3).

The bottom line is that improvements in energy efficiency, a smaller energy footprint (relative to output) and the broader U.S. transition from being a net energy importer to a net energy exporter have together reduced the direct drag on growth and particularly consumption from oil and gas price shocks.

That does not mean higher prices today are painless. Energy demand remains relatively inelastic in the short run, and lower-income households remain disproportionately exposed. We’ve marked down our real PCE growth forecast as a result of the recent move higher in prices.

It seems prudent to again state the obvious here that this still remains an incredibly fluid situation, but at the aggregate level, the effect of higher energy prices is more likely to show up as slower consumption growth, rather than the abrupt retrenchment that characterized past oil shocks. But let’s see where this goes.

by around one percentage point. But consider this. We estimate that same 50% sustained rise in prices would have had about twice the effect back in the 1980s, lopping off around two percentage points off PCE growth. In other words, back then, talk of recession would already be gathering steam, all else equal.){kind=link}