- Middle East conflict to remain primary driver amid peace efforts.

- US payrolls report in focus as Fed rate cut hopes fade.

- Other US data, including ISM PMIs, to shed further light on US economy.

- Eurozone and Japanese inflation also on tap ahead of Easter break.

Iran turmoil clouds outlook

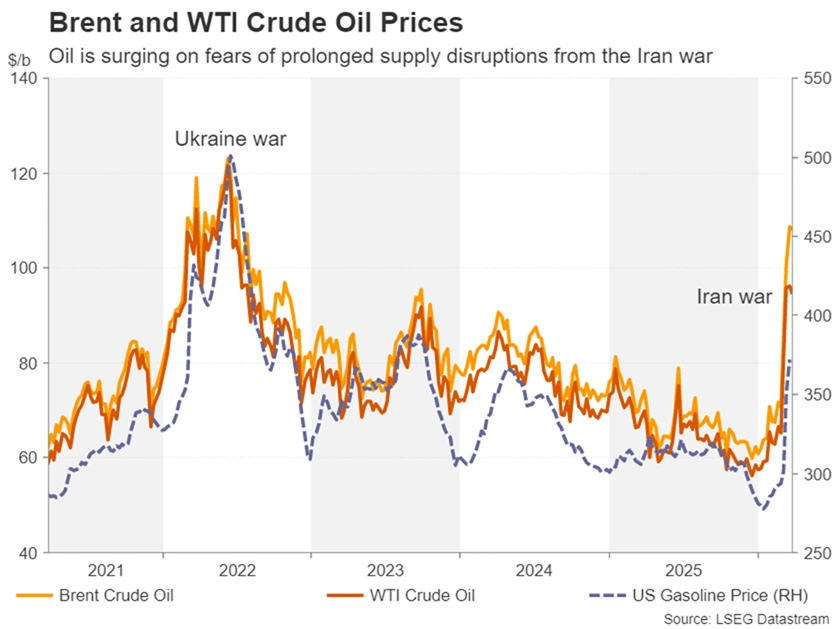

Despite contradictory reports, a quick resolution to the Iran war doesn’t appear to be on the near-term horizon, heightening the uncertainty over the global economic outlook. Most importantly, oil and gas prices remain elevated, even if they haven’t been scaling new highs lately.

Thus, for central banks, the inflation threat has far from receded and the growing realisation of this is being reflected across all asset classes, with equities and bonds being sold off and the US dollar standing tall. The latter’s popularity coupled with gold’s unusual lack of safe-haven appeal indicates that investors have preferred to hold cash during this conflict.

That’s not to say that there is no prospect of the US and Iran agreeing to hold face-to-face talks aimed at ending the hostilities. After all, President Trump’s repeated insistence that America is winning the war and that Tehran is desperate to make a deal suggests he is seeking a way out.

With the US midterm elections approaching, it does not bode well for the Republican party for gasoline prices to be this high, as both the party’s and Trump’s popularity have plummeted since the start of the US-Israeli strikes.

However, markets are becoming increasingly wary of the peace efforts, as Iran has repeatedly rejected the White House’s 15-point plan and especially as there are equally strong signals of an escalation, amid the buildup of US troops in the region.

Nevertheless, any meaningful progress to begin ceasefire talks would boost risk appetite as well as divert more attention towards economic events.

From rate cuts to rate hikes

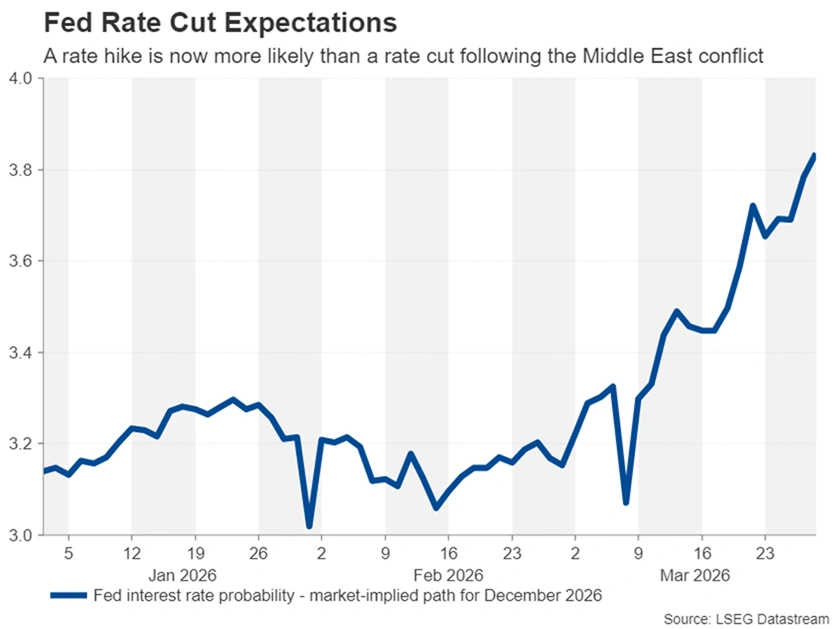

The highlight on the economic front will be the nonfarm payrolls in the United States. Most Fed policymakers continue to downplay the risks to the labour market while highlighting the inflation risks. Moreover, markets are now on board with the Fed’s hawkish stance. Investors have not only priced out any rate cuts for the foreseeable future, but they’ve also priced in around 18 basis points of rate increases by year-end.

If the incoming data reinforces the view of a resilient economy and sticky inflation, then it won’t take much for a full 25-bps hike to be baked in.

And there’s plenty of releases on the agenda that could shape those expectations, starting with the Chicago PMI and consumer confidence index for March, and the JOLTS job openings for February on Tuesday. February retail sales and the ISM manufacturing PMI for March will grab the spotlight on Wednesday, together with the ADP employment numbers. There will be more labour market indicators on Thursday with the Challenger Layoffs for March.

Will there be a jobs bounce in March?

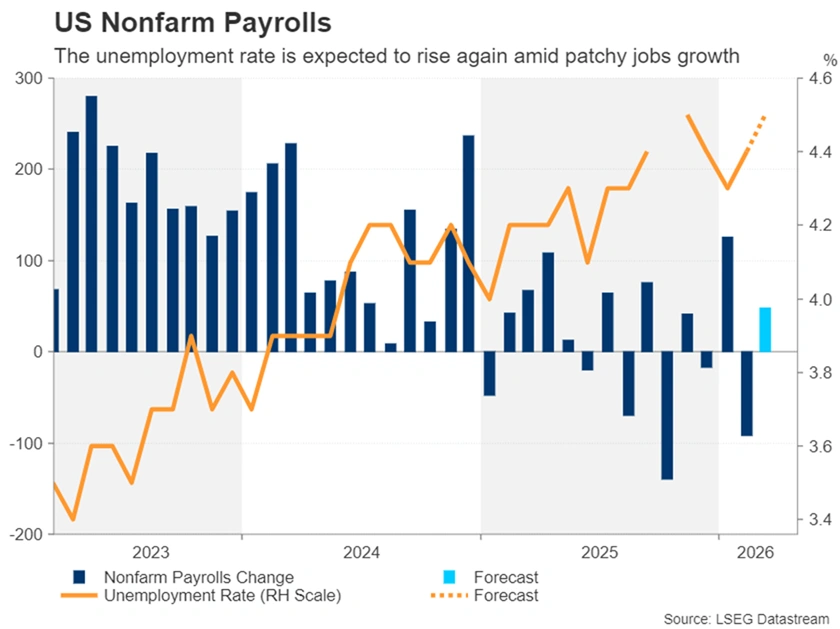

But the main highlight as always will be Friday’s official NFP figures and the ISM services PMI. The US economy unexpectedly shed 92k jobs in February so the focus in the March data will not only be whether there was a rebound, but also if the prior month’s print will be revised higher.

The consensus estimate for March is a gain of 48k, but the unemployment rate is forecast to have edged up from 4.4% to 4.5%.

The ISM’s services activity gauge will be watched too, particularly the employment and prices paid components.

Any signs that the US jobs market is not in as good a shape as the Fed currently thinks it is, could revive rate cut expectations, but probably only mildly, unless there’s a massive drop in payrolls for the second straight month. The US dollar is likely to take a knock in such a scenario. But stocks would be in greater danger if a worsening economic picture is only partially offset by a very modest boost to rate cut bets.

Eurozone CPI eyed as ECB ponders rate hike

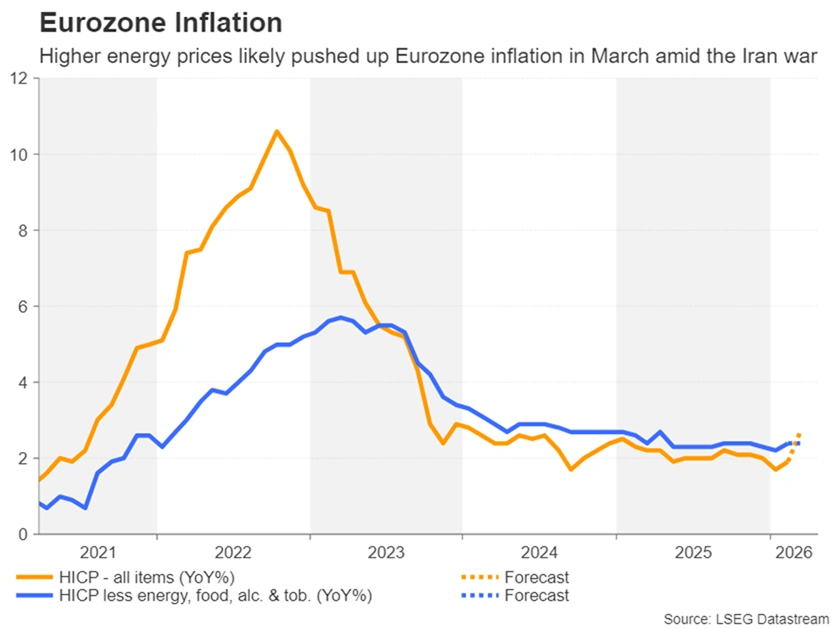

Across the pond, there’s been an even sharper repricing for rate expectations. Both the European Central Bank and Bank of England are seen to be raising interest rates at least twice this year, probably three times. Europe is much more reliant on oil and gas imports from the Middle East, unlike the US, which is far less energy dependent, and so the ECB and BoE have little option but to contain the fallout from the energy price shock that the Iran crisis has unleashed.

Revised estimates of Q4 GDP growth out of the UK on Tuesday are unlikely to have much bearing on BoE rate hike expectations as it’s now outdated, but the Eurozone’s flash inflation readings on the same day will be monitored quite closely.

There was a small uptick in all Eurozone CPI measures in February, including the two core rates. A further acceleration in March could make policymakers more inclined to vote for a rate hike sooner rather than later.

Investors see around a two-thirds probability of a 25-bps increase at the April meeting, but it’s unclear if a majority of Governing Council members are ready to back an early move. Still, if the March CPI numbers are hotter than expected, those odds would likely increase, lifting the euro somewhat.

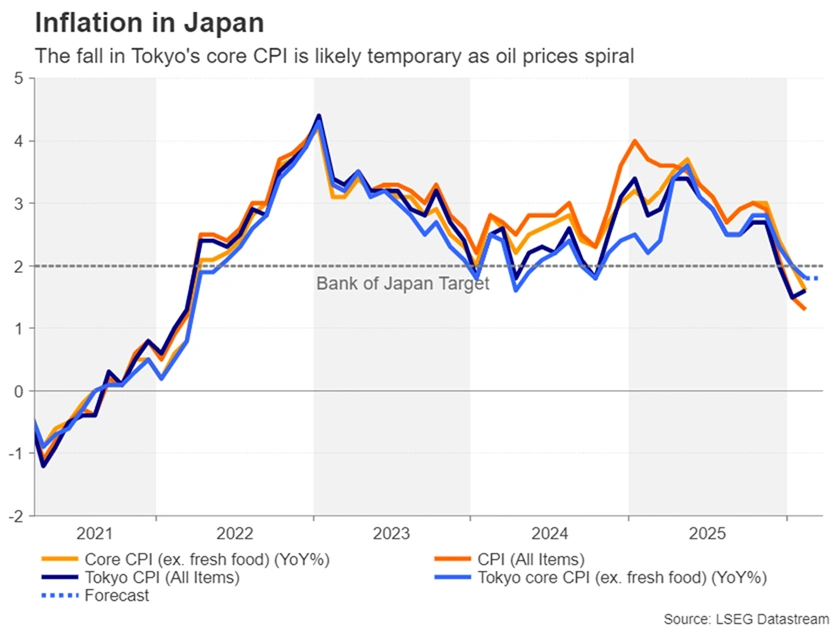

Can Tokyo CPI shift BoJ hike expectations?

Interestingly, tightening expectations for the Bank of Japan have been less dramatic, despite the significant upside risk to Japanese inflation from the Iran conflict. Japan imports almost 90% of its oil from the Middle East and faces potential energy shortages if the blockage of the Strait of Hormuz doesn’t end soon.

The government has resorted to releasing some of its strategic oil reserves and there’s even reports it is thinking about buying Iranian oil in Chinese yuan, to evade US sanctions.

For Japan, the jump in crude oil prices poses a dual risk to inflation – first directly via higher fuel costs and indirectly via the weaker yen, which itself is coming under pressure due to the strain of the oil crisis on the country’s current account balance.

Yet, markets continue to price in just two 25-bps rate rises for 2026. Worries about the impact of higher energy costs on growth are likely dampening the more hawkish bets. But the Bank of Japan doesn’t seem too phased just yet, keeping the option of an April rate hike firmly on the table.

If preliminary March CPI numbers for the Tokyo district out on Tuesday show inflation heading back above the BoJ’s 2.0% target, tightening odds for April could climb higher from around 62% currently, offering some support to the beleaguered yen, as it inches ever closer to the critical 160.00 intervention mark.

Also out on Tuesday are industrial production and retail sales figures for February, followed by the BoJ’s quarterly Tankan business survey on Wednesday.

{kind=link}