- Gold traders appear confused amid the Middle East conflict.

- Fed rate hike bets prevail, increasing the metal’s opportunity cost.

- Strong central bank demand is keeping losses limited.

- Heightened inflation fears could push gold below the key $4,500 zone.

Inflation Concerns Eliminate Gold’s Haven Appeal

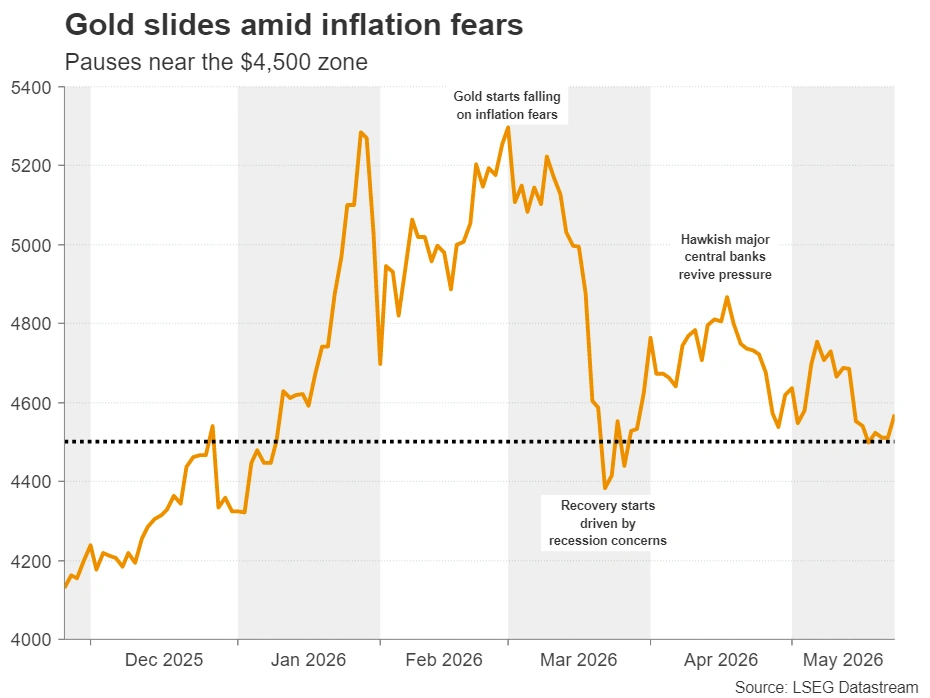

It has been a very confusing period for gold traders lately, as they have been trying to figure out whether selling it or buying it is the appropriate strategy amid tensions in the Middle East.

The conflict began on February 28, and the initial reaction of the precious metal was to spike higher amid safe-haven demand. But as soon as investors started realizing that the closure of the Strait of Hormuz could result in accelerating inflation, they started liquidating their positions, feeling the pressure of rising yields around the globe and increasing bets that the Fed is unlikely to cut interest rates further. The metal hit a high of $5,420 and then sold off to hit a low of $4,345 on March 23.

A recovery followed as soft data sparked some recession fears, allowing the metal to reclaim its safe-haven status. That said, this did not last long, as the continued closure of the Hormuz Strait prompted major central banks to sound even more hawkish, with the RBA raising interest rates three times already, the ECB seen raising interest rates twice by the end of the year, and a strong chance being assigned to a Fed rate increase by December.

Following the recovery, the metal hit resistance at $4,890 and pulled back to settle near the $4,500 zone. Even with a ceasefire in place and headlines hitting the wires every now and then, traders appear unwilling to scale back their rate hike bets, which is required for reducing the opportunity cost of holding gold and thereby allowing a stronger recovery. Perhaps this is because every time a headline hits the wire about a potential peace deal, it is quickly refuted by an exchange of hostile rhetoric between US and Iranian officials, or by new attacks.

Central Bank Demand Increases in Q1 2026

But gold did not extend its losses either. One would have expected that further advances in Treasury yields and increasing rate hike bets would exert more pressure on the metal. But it didn’t.

Maybe a major supportive force is the continued demand by major central banks. According to the World Gold Council, central bank demand increased by 17% in Q1 compared to Q4 2025. This could mean that the de-dollarization scheme continues as several nations want to loosen their dependency on the US economy, and that banks may still be following an inflation-hedging strategy.

Elevated Inflation Increases Fed Rate Hike Chances

Moving ahead, despite gold’s support from major central banks, it is hard to envision a strong and robust recovery toward record highs any time soon. Even if the US and Iran agree on further negotiations and peace talks, as long as the Strait of Hormuz remains closed, rising oil prices could result in stickier headline inflation that feeds through into underlying price pressures.

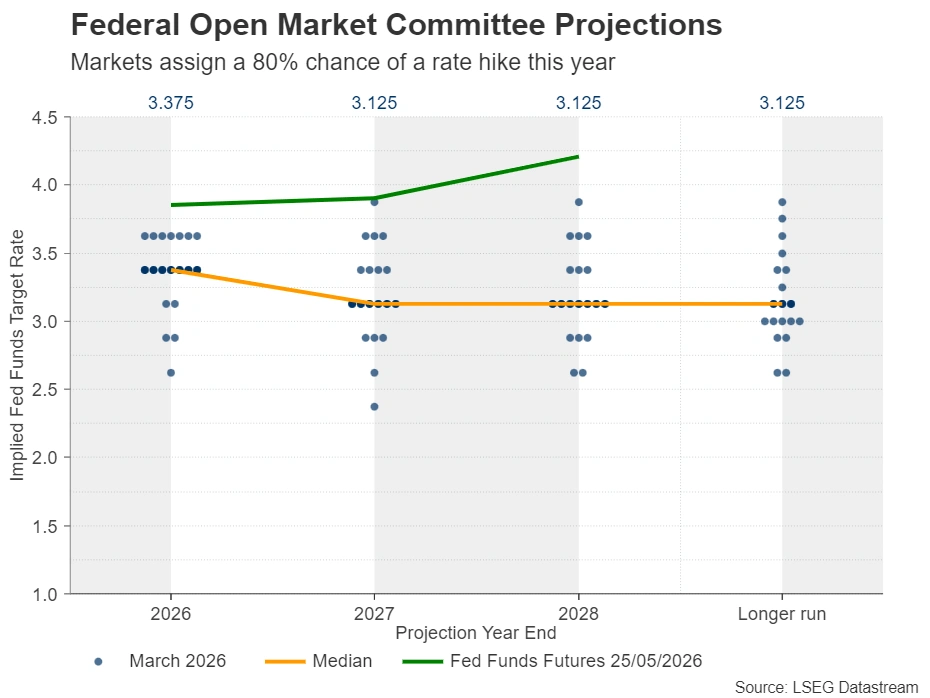

This could keep rate hike bets, and thereby Treasury yields, elevated, perhaps helping the US dollar recover some of its recently lost ground. According to Fed funds futures, a 25bps rate hike by the Fed is more than fully priced in for March 2027, while there is a strong 80% chance that this could happen by the end of this year.

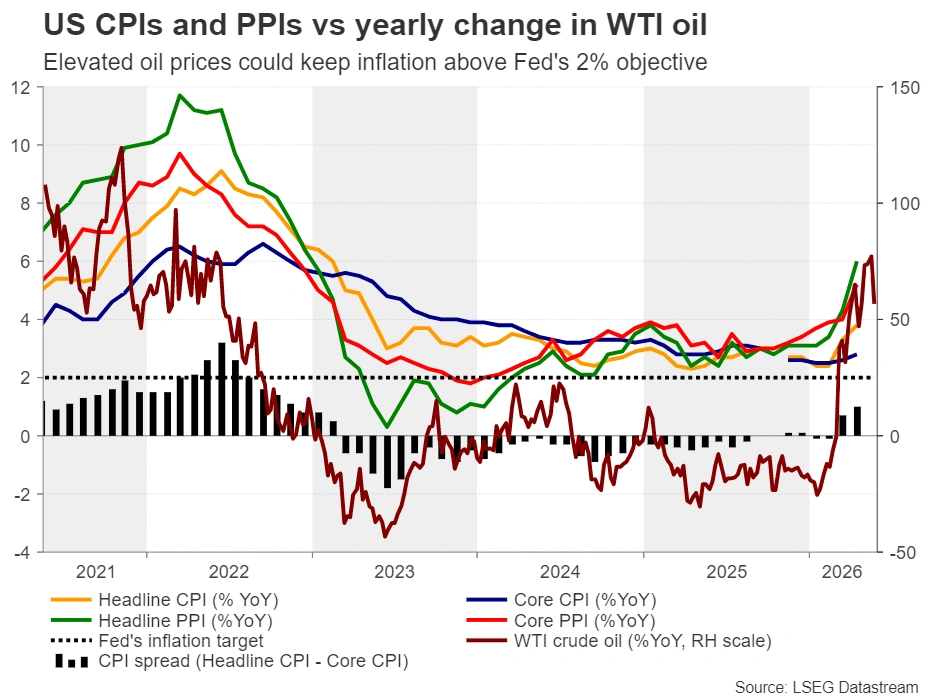

The hawkish narrative was boosted by the latest inflation data, with both the CPI and PPI figures revealing hotter-than-expected inflation for April. With the headline PPI rate surging at 6%, it seems that CPI inflation could remain elevated in the months to come, as producer prices could translate into higher consumer prices for products arriving on store shelves a few months after production. What also argues for a prolonged period of high inflation is the elevated oil prices. Despite the latest pullback, oil prices remain well above the levels seen a year ago, keeping the year-on-year rate high, meaning that it may take some time before annual inflation rates retreat to the Fed’s 2% objective.

Thus, US data corroborating that view may allow investors to bring the rate-hike timing closer. A reasonable timing for the Fed to press the hike button may be September. June or July may be too soon, as those would be the first meetings under the leadership of Kevin Warsh. Let’s not forget that Kevin Warsh was appointed by US President Trump on the basis that he will be more dovish than his predecessor, Jerome Powell. So beginning his term with a rate hike may not be the best strategy. Having said that, a major dovish shift is unlikely as well amid all these inflationary threats. Also, Jerome Powell is expected to remain within the Federal Reserve as a governor, and his more hawkish views could translate into rate-hike votes.

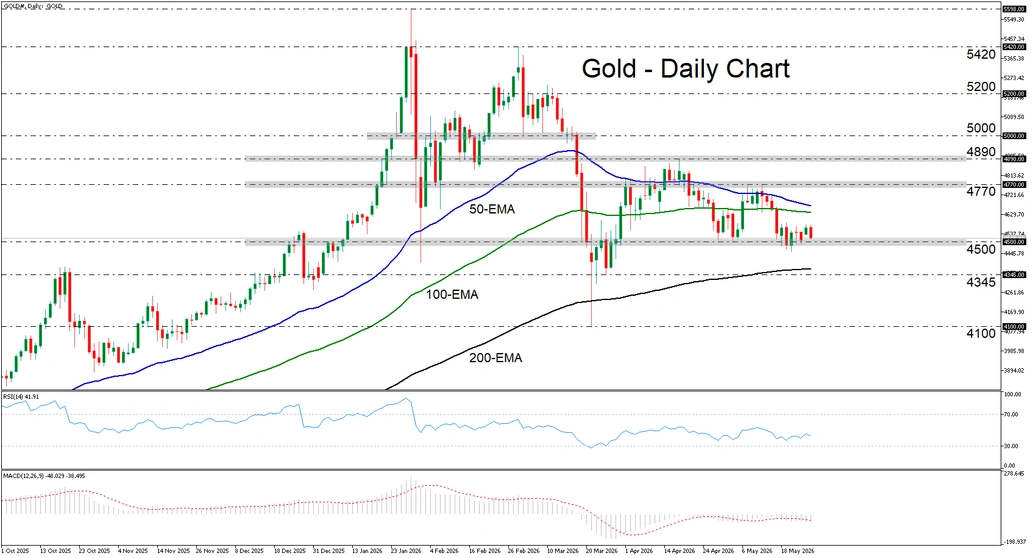

How Long Will the $4,500 Region Hold?

From a technical standpoint, the risks from a more hawkish Fed could translate into downside risks for gold. A decisive dip below $4,500 could invite more bears into the game and perhaps see scope for declines toward the 200-day exponential moving average, or the $4,345 zone. A break lower could carry more bearish implications, perhaps targeting the low of March 23 at $4,100.

On the upside, the move signaling a brighter future may be a break above $4,770. This could initially target the $4,890 zone, marked by the high of April 17, a break of which could set the stage for advances toward the $5,200 area.

{kind=link}