Risk appetite continued in the market as US equities extended record run. DJIA finally took out 20000 handle to close at 20068.52, up 155.80 pts or 0.78%. S&P 500 closed up 18.3 pts, or 0.80%, at 2298.37. NASDAQ ended at 5656.34, up 55.38 pts or 0.99%. All three indices closed at new historical highs. Positive sentiments carried on in Asian session with Nikkei up 1.8% to above 19400 Notable strength was also seen in treasury yields. 10 year yield gained 0.052 to close at 2.523 while 30 year yield rose 0.052 to 3.108. However, the greenback continued to lag behind with Dollar index dipping through 100 handle to as low as 99.79. The index is trying to regain 100 handle at the time of writing but lacks momentum so far. In the currency markets, dollar remains the weakest major currency this week while Sterling is the strongest.

Stock markets up trend resumed on expectation that US president Donald Trump would gradually implement the pro-growth policies he promised. Sentiment was also lifted by encouraging earnings reports. As soon as he has been sworn in, Trump signed a series of executive orders with the latest one on Keystone and Dakota pipelines. The action aims at facilitating TransCanada to build the Keystone XL pipeline and for Energy Transfer Partners to build the final uncompleted portion of the Dakota Access pipeline. A report by McClatchy revealed that the President and his team has compiled a list of about 50 infrastructure projects nationwide, totaling at least USD 137.5b. According to the preliminary list provided to the National Governor’s Association, the projects include to renewal of the country’s highways, airports, dams and bridges. A similar list was revealed by the Star. The market was thrilled by the news with DJIA’s material sector index gaining over 2%.

Some economists attributed the breakdown in correlation between treasury yield and Dollar to concerns over Trump’s protectionism. Some pointed to the US-Japan trade conflicts back in 1990s when Dollar was weak despite higher US interest rates. But at this point, it’s still too early to confirm the divergence in yield and Dollar. Technically, the benchmark 10 year yield is held below key near term resistance at 2.621. Dollar index is holding above key structural support at 99.43. Technically, both can be seen as staying in consolidative mode. As stocks are gathering bullish momentum, the picture will likely be cleared soon.

On the data front, New Zealand CPI rose 0.4% qoq, 1.3% yoy in Q4. Japan corporate service price rose 0.4% yoy in December. Swiss trade surplus narrowed to CHF 2.72b in December. German Gfk consumer sentiment rose to 10.2 in February. UK Q4 GDP will be the main focus in European session. UK BBA mortgage approval and CBI reported sales will also be featured. From US, jobless claims, wholesale inventories, new home sales and leading indicators will be released.

GBP/USD Daily Outlook

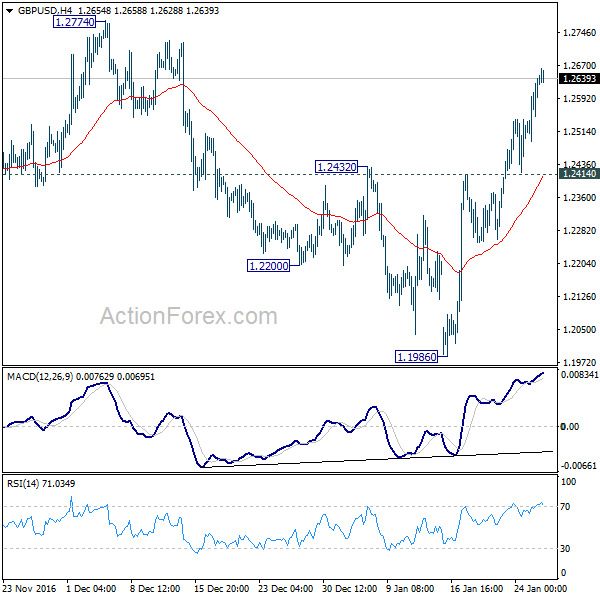

Daily Pivots: (S1) 1.2535; (P) 1.2586; (R1) 1.2683; More…

GBP/USD reaches as high as 1.2662 so far as rebound from 1.1986 extends. Intraday bias stays on the upside for 1.2774 resistance. Again, rise from 1.1986 is seen as the third leg of the consolidation pattern from 1.1946. We’d expect strong resistance at 1.2774 to limit upside and bring down trend resumption eventually. On the downside, below 1.2414 minor support will turn bias to the downside for retesting 1.1946 low.

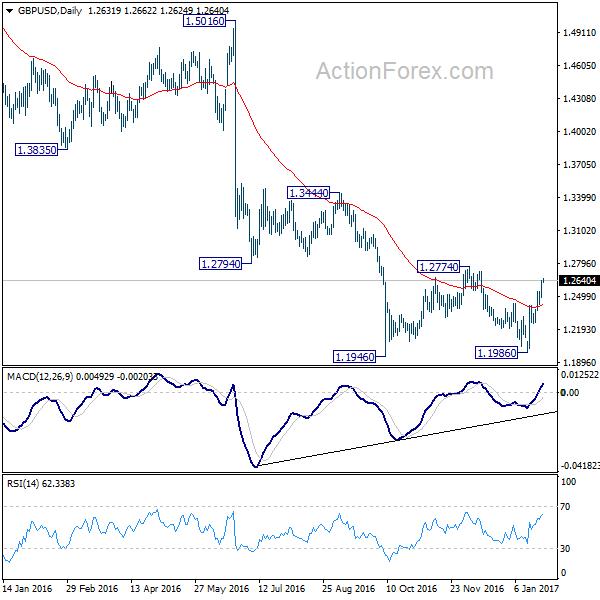

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.40% | 0.30% | 0.30% | |

| 21:45 | NZD | CPI Y/Y Q4 | 1.30% | 1.20% | 0.40% | |

| 23:50 | JPY | Corporate Service Price Y/Y Dec | 0.40% | 0.40% | 0.30% | |

| 7:00 | CHF | Trade Balance (CHF) Dec | 2.72B | 2.81B | 3.64B | 3.50B |

| 7:00 | EUR | German GfK Consumer Confidence Feb | 10.2 | 10 | 9.9 | |

| 9:30 | GBP | BBA Mortgage Approvals Dec | 41000 | 40659 | ||

| 9:30 | GBP | GDP Q/Q Q4 A | 0.50% | 0.60% | ||

| 9:30 | GBP | GDP Y/Y Q4 A | 2.10% | 2.20% | ||

| 9:30 | GBP | Index of Services 3M/3M Nov | 0.90% | 1.00% | ||

| 11:00 | GBP | CBI Retailing Reported Sales Jan | 27 | 35 | ||

| 13:30 | USD | Advance Goods Trade Balance Dec | -64.5B | -66.6B | ||

| 13:30 | USD | Wholesale Inventories Dec P | 0.10% | 1.00% | ||

| 13:30 | USD | Initial Jobless Claims (JAN 21) | 245k | 234k | ||

| 15:00 | USD | New Home Sales Dec | 585k | 592k | ||

| 15:00 | USD | Leading Indicators Dec | 0.50% | 0.00% | ||

| 15:30 | USD | Natural Gas Storage | -243B |

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

{kind=link}