Sterling’s free fall extends into Asian session today, even against the weak Euro which is pressured against all other major currencies. Dollar is currently the strongest one and would likely remain so for now. Yen, Swiss Franc and Canadian Dollar are also firm. Australian and New Zealand Dollar are mixed for now, but both are vulnerable to renewed selling in risk markets.

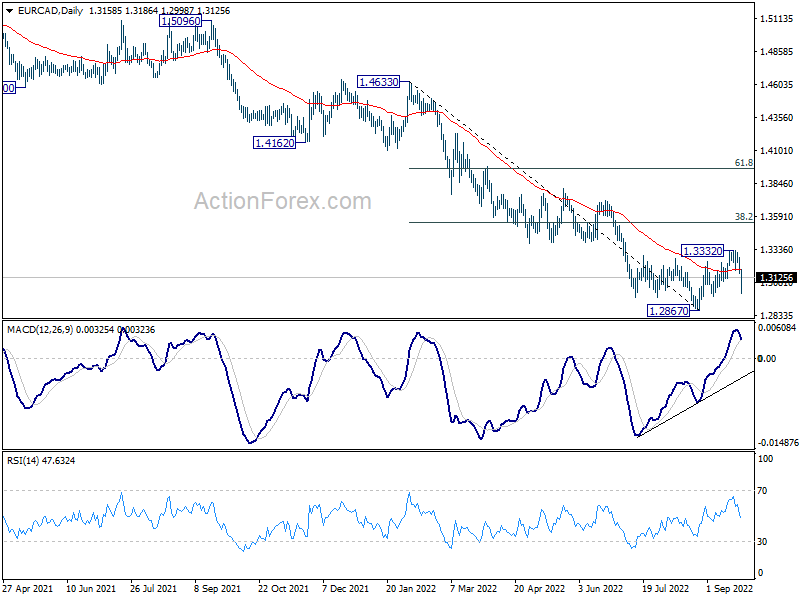

Technically, other than the decline in the Pound, some attention in on whether Euro’s selloff would intensify. EUR/CHF has already broken through 0.9464 support to resume recent down trend. EUR/CAD’s corrective recovery from 1.2867 might have completed at 1.3332 with today’s steep fall. There is no follow through decline yet. But retest of 1.2867 low is now in favor, and break will confirm down trend resumption.

In Asia, at the time of writing, Nikkei is down -2.58%. Hong Kong HSI is up 0.17%. China Shanghai SSE is down -0.08%. Singapore Strait Times is down -1.04%. Japan 10-year JGB yield is up 0.0094 at 0.254.

Fed Bostic: Economy can slow in a relatively orderly way

Atlanta Federal Reserve President Raphael Bostic said on CBS’s “Face the Nation” program, “Inflation is high. It is too high. And we need to do all we can to make it come down.”

He added the US need to have a “slowdown”, but “we are going to do all that we can at the Federal Reserve to avoid deep, deep pain.”

“We’re still creating lots of jobs on a monthly basis, and so I actually think that there is some ability for the economy to absorb our actions and slow in a relatively orderly way,” he said.

Japan FM Suzuki: Will take action against speculations on Yen if needed

Japanese Finance Minister Shunichi Suzuki reiterated that the government is “strongly concerned” about one-sided, rapid yen moves.

“We took appropriate action against excessive volatility driven by speculators. The intervention has had a certain effect,” he said, referring to last week’s intervention to support Yen. “There is no change in our stance that we will take (further) action if needed.”

“Governor Kuroda expressed Thursday in his remarks his strong concerns about the rapid depreciation of the yen. We have a shared view on this with the BOJ,” Suzuki added.

Former top currency diplomat Naoyuki Shinohara, however, said, “it’s unlikely Japan will continue intervening to defend a certain line, such as 145 yen to the dollar… It’s impossible to reverse the market’s broad trend with intervention alone.” Shinohara oversaw Japan’s currency policy during the global financial crisis in 2008.

Japan PMI manufacturing dipped to 51.0, services rose to 51.9

Japan PMI Manufacturing dropped slightly from 51.5 to 51.0 in September, below expectation of 51.1. That’s the lowest reading since January 2021. Manufacturing Output Index dropped from 49.2 to 48.9. PMI Services, on the other hand, rose from 49.5 to 51.9. PMI Composite rose from 49.4 to 50.9.

Joe Hayes, Senior Economist at S&P Global Market Intelligence, said: “Business are reporting concerns around the economic outlook amid steep cost pressures and the rising likelihood of a global economic downturn. The remarkable weakness we’ve seen in the year-to-date in the yen continues to push up price pressures, with companies struggling to fully pass on these higher costs burdens to clients. Subsequently business confidence slumped to a 13-month low”.

US consumer confidence and Eurozone CPI to highlight the week

Economic should be back on center stage in this last week of the quarter. US consumer confidence, personal income and spending, could trigger most volatility. But durables goods orders will also be watched. Germany Ifo business climate and Gfk consumer confidence and Eurozone CPI flash will also catch much attention. Other data include Japan PMI manufacturing, Japan industrial production and retail sales, Canada GDP, Australia retail sales, New Zealand ANZ business confidence, and China PMIs.

Here are some highlights for the week:

- Monday: Japan PMI manufacturing; Germany Ifo business climate.

- Tuesday: Japan corporate service prices; Eurozone M3 money supply; US durable goods orders, house price index, consumer confidence, new home sales.

- Wednesday: BOJ minutes; New Zealand ANZ business confidence; Australia retail sales; Germany Gfk consumer climate; US goods trade balance, pending home sales.

- Thursday: Germany CPI flash; Canada GDP; US GDP final, jobless claims.

- Friday: New Zealand building permits, Japan industrial production, retail sales, unemployment rate, consumer confidence, housing starts; China PMIs; UK GDP final, M4 money supply, mortgage approvals; Swiss retail sales, KOF economic barometer; Germany unemployment; Eurozone CPI flash, unemployment rate; US personal income and spending, with PCE inflation, U of Michigan consumer sentiment.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8784; (P) 0.8860; (R1) 0.9008; More…

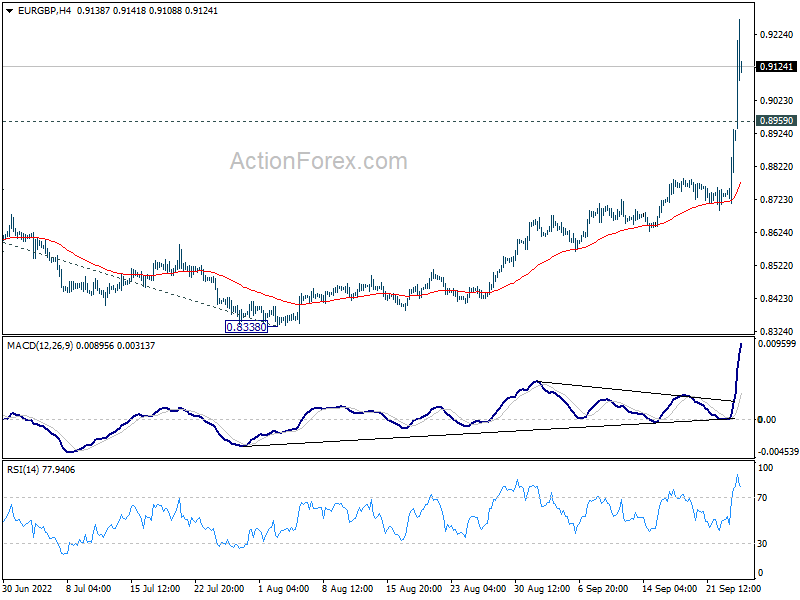

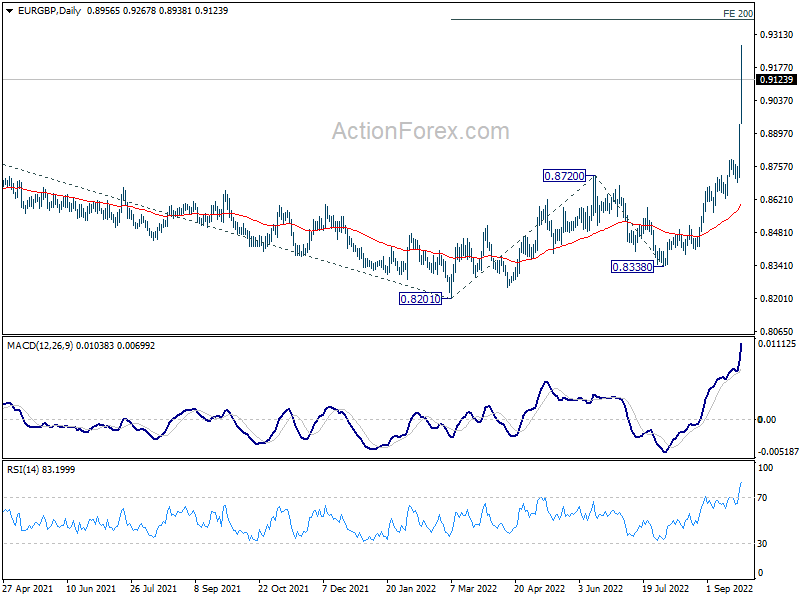

EUR/GBP’s rally accelerates further to as high as 0.9267 so far. There is no sign of topping yet. Intraday bias stays on the upside for 200% projection of 0.8201 to 0.8720 from 0.8338 at 0.9376. Firm break there will target 0.9499 long term resistance. On the downside, below 0.8959 minor support will turn bias neutral and bring consolidations first, before staging another rally.

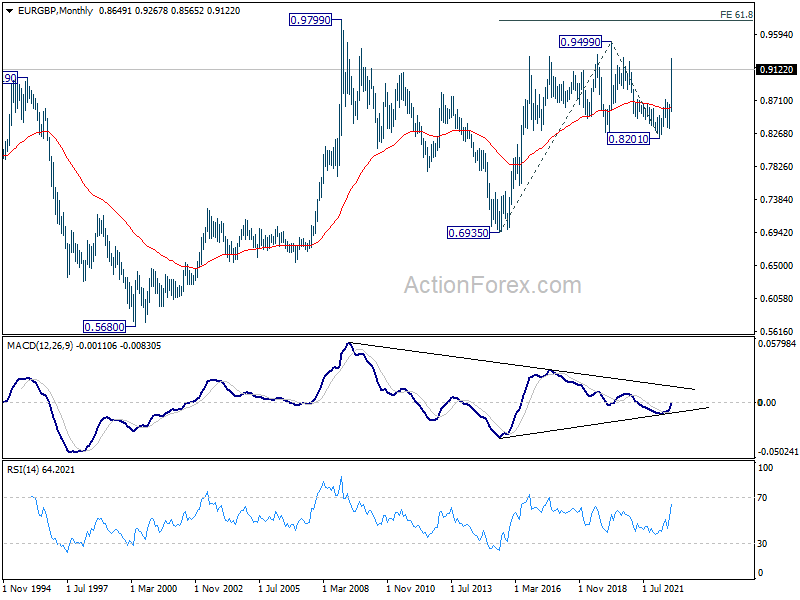

In the bigger picture, rise from 0.8201 is in progress targeting 0.9499 (2020 high) next. Based on current momentum, such rally should be resuming the up trend from 0.6935 (2015 low). Firm break of 0.9499 will target 61.8% projection of 0.6935 to 0.9499 from 0.8201 at 0.9786, which is close to 0.9799 (2008 high). This will now remain the favored case as long as 0.8720 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Sep P | 51 | 51.1 | 51.5 | |

| 08:00 | EUR | Germany IFO Business Climate Sep | 87.1 | 88.5 | ||

| 08:00 | EUR | Germany IFO Current Assessment Sep | 96 | 97.5 | ||

| 08:00 | EUR | Germany IFO Expectations Sep | 78.6 | 80.3 |

{kind=link}