Sterling and Dollar remain the two strongest currencies today. The Pound surges further as boosted by comments from European Parliament’s chief Brexit negotiator Guy Verhofstadt that there is a 50/50 chance of making "sufficient progress" today. Dollar, on the other hand, is firmly supported by optimism on getting the tax bill done before end of the year. Swiss Franc and Yen are trading broadly lower as risk appetites return. At the time of writing, DAX is trading up 1.4%, CAC up 1.0%. US futures point to sharply higher over as DOW will likely extend the record run.

Republicans dismissed Trump’s idea of 22% corporate tax

With Senate and House passed their respective tax bill, work will now move on to reconciling the plans. Some Republicans like Senator David Perdue of Georgia was optimistic that the differences could be hammered out quickly and the bill could be on President Donald Trump’s desk within 10 days. Talking about Trump, he said on Saturday that the final corporate tax rate "could be 22 (percent)", which is estimated to raise USD 200b over 10 years, comparing to 20% rate. But the idea is generally dismissed by other Republicans as they’re committed to 20% figure.

Eurozone Sentix dipped on 2018

Eurozone Sentix investor confidence dropped to 31.1 in December, down from 34.0 and missed expectation of 32.7. Sentix noted that "investors are asking whether 2018 can be even better, and are hedging their bets on the future by placing their expectations below those of September 2017." Nonetheless, it played down the fall as there’s nothing for concern when it just hit a 10 year high in November. Also from Eurozone, PPI rose 0.4% mom, 2.5% yoy in October.

UK PM May to seek progress on Brexit negotiation

UK Prime Minister Theresa May will have lunch with European Commission President Jean-Claude Juncker in Brussels today. Juncker has set today as the deadline for May to revise her offer on Brexit. But UK government played down today’s significance and pointed to the EU summit on December 14/15 as the crucial one. In a statement, UK said that "with plenty of discussions still to go, Monday will be an important staging post on the road to the crucial December council." European Parliament’s Brexit negotiator Guy Verhofstadt said that agreements on the Irish border, the UK "divorce bill" and citizens rights were "possible". And there is 50/50 chance of giving the green-light for trade talks today.

UK PMI construction rose to 53.1 in November, up from 50.8 and beat expectation of 51.0. Markit said that "UK construction companies experienced a solid yet uneven improvement in business conditions during November." It pointed out that "the latest survey revealed sustained reductions in commercial building and civil engineering, with the latter now experiencing its longest period of decline since the first half of 2013".

Elsewhere

Japan consumer confidence rose to 44.9 in November, up from 44.5 and met expectation. Monetary base rose 13.2% yoy in November, slowed from 14.5% yoy. Australia TD securities inflation rose 0.2% mom in November.

BIS warned of global risk taking

The Bank for International Settlements warned in its quarterly financial review that "the vulnerabilities that have built around the globe during the long period of unusually low interest rates have not gone away." And, "high debt levels, in both domestic and foreign currency, are still there. And so are frothy valuations." Adding to that "the longer the risk-taking continues, the higher the underlying balance sheet exposures may become."

The reported noted that the situation was similar to pre-2008 global financial crisis era. While global central banks are generally on tightening path, BIS head Claudio Borio was uncertain if the tightening is effective. He pointed out that "even as the Fed has proceeded with its tightening, overall financial conditions have eased. If financial conditions are the main transmission channel for tighter policy, has policy, in effect, been tightened at all?"

RBA to stand pat

RBA rate decision is a key focus in the upcoming Asian session. The central bank is widely expected to keep its cash rate unchanged at record low of 1.50% on Tuesday. Considering weak wage growth and lack of inflationary pressure, there is little push for a hike at the moment. On the other hand, there were even talks that RBA is in "cut" territory due to sluggish house price growth. According to CoreLogic data back in November, annual price growth mere stood at 5.2%, half of the peak of 10.4% back in May 2017. More importantly, the six month price growth stood at 0.7%. And in the past 30 years, 7 out of 9 times RBA cut interest rates as 6-month house price growth weakened to zero or turned negative. But of course, considering RBA’s high alertness on household debts, the central bank is also nowhere near a cut.

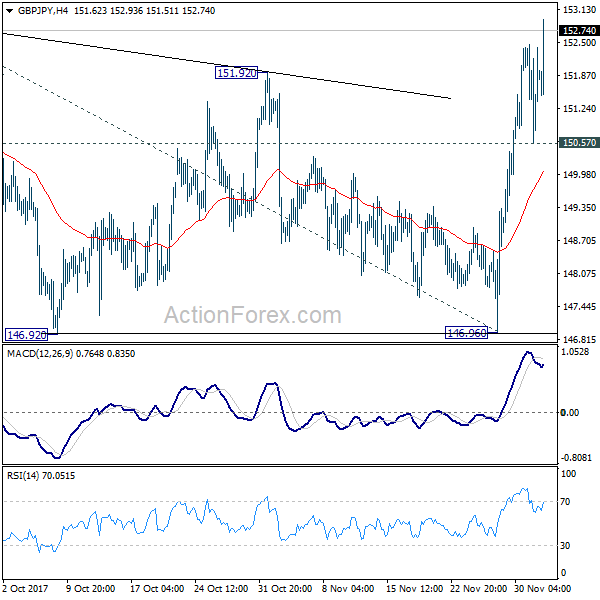

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.23; (P) 151.35; (R1) 152.16; More…

GBP/JPY surges to as high as 152.93 so far today. Breach of 152.82 resistance argues that medium term rally is resuming. Intraday bias is back on the upside. Sustained trading above 152.93 will pave the way to 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. On the downside, though, break of 150.57 minor support will dampen the bullish view and turn bias neutral first.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after consolidation from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 46.96 support will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Nov | 13.20% | 13.20% | 14.50% | |

| 0:00 | AUD | TD Securities Inflation M/M Nov | 0.20% | 0.30% | ||

| 5:00 | JPY | Consumer Confidence Index Nov | 44.9 | 44.9 | 44.5 | |

| 9:30 | GBP | Construction PMI Nov | 53.1 | 51 | 50.8 | |

| 9:30 | EUR | Eurozone Sentix Investor Confidence Dec | 31.1 | 32.7 | 34 | |

| 10:00 | EUR | Eurozone PPI M/M Oct | 0.40% | 0.30% | 0.60% | 0.50% |

| 10:00 | EUR | Eurozone PPI Y/Y Oct | 2.50% | 2.60% | 2.90% | |

| 15:00 | USD | Factory Orders Oct | -0.40% | 1.40% |