Trading activities in the forex markets are rather subdued today. Dollar weakens mildly as traders are staying cautious ahead of FOMC rate decision later on Wednesday. Sterling is also soft as markets eye today’s inflation data. On the other hand, New Zealand Dollar remains the strongest one this week and commodity currencies are generally firm. But there is no confirmed signs of a trend there yet. In other markets, US indices gained some ground overnight but DOW and S&P 500 are kept below the historical highs made last week. Treasury yields were mixed with 10 year yield gained a little by 0.002 to 2.385. Asian markets are also mixed with Nikkei trading nearly flat at the time of writing.

Australia business conditions dropped sharply

Australia NAB business conditions dropped sharply by -9 to 12 in November, down from 21. Business confidence dropped -2 to 6, down from 8. NAB chief economist Alan Oster noted that "we expected to see last month’s spike in business conditions unwound fairly quickly as it both came as a bit of a surprise, and was also out of sorts with what we were seeing in some of the other leading indicators from the survey, such as forward orders." Also, "we are paying close attention to what now appears to be a downward trend in business confidence as that could naturally have some implications for decisions around hiring and investment."

For Australia, sluggish wage growth is a key concern for keeping inflation low. But Oster noted that "we saw some tentative signs of higher wages in the survey, although that does appear to be weighing on the confidence of some firms as well." However, "prices are rising the most in mining, while retail and personal services prices are the softest – a reflection of the cautious spending behavior by consumers."

Also from Australia house price index dropped -0.2% qoq in Q3, below expectation of 1.5% qoq.

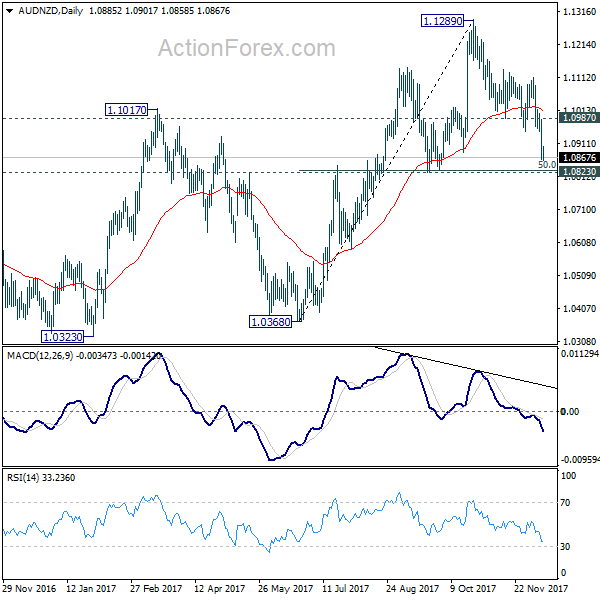

AUD/NZD in steep pull back this week

AUD/NZD dives sharply this week. Kiwi was boosted by positive reactions to appointment of Superannuation Fund chief Adrian Orr as the next RBNZ Governor. That’s is seen as guaranteeing a practical approach in RBNZ reform. AUD/NZD’s recent fall from 1.1289 is so far seen as a corrective move. While more downside could be seen, we’d expect strong support at 1.0823 (50% retracement of 1.0368 to 1.1289 at 1.0829) to contain downside and bring rebound. Above 1.0987 resistance will turn bias to the upside for retesting 1.1289.

Merkel to react in concrete way to Macron’s EU proposals

German Chancellor Angela Merkel said she wanted to complete the coalition talks with the Social Democrats quickly. And to her, a "stable" government is the basis Germany can work best with France and Europe. In her view, it’s a "historical necessity" to reform Europe. And Germany would be able to "react in a concrete way" to French President Emmanuel Macron’s proposals. She emphasized that "Europe does not only need a stronger economic and monetary union but we must also have a Europe of security and the rule of law, internally and externally."

Looking ahead

UK inflation data will take center stage in European session. CPI is expected to be unchanged at 3.0% yoy in November. RPI is expected to unchanged at 4.0% yoy. PPI will also be released too. German will also release ZEW economic sentiment. Later in the day, US will release PPI, but traders will likely look beyond that to tomorrow’s CPI and FOMC rate decision.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7503; (P) 0.7524; (R1) 0.7546; More…

Intraday bias in AUD/USD remains neutral for consolidation above 0.7500 temporary low. Upside of recovery should be limited below 0.7652 resistance to bring fall resumption. Break of 0.7500 will extend the fall from 0.8124 and target 0.7322/8 cluster support next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8029). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI M/M Nov | 0.40% | 0.20% | 0.30% | |

| 23:50 | JPY | Domestic CGPI Y/Y Nov | 3.50% | 3.30% | 3.40% | |

| 00:30 | AUD | NAB Business Conditions Nov | 12 | 21 | ||

| 00:30 | AUD | NAB Business Confidence Nov | 6 | 8 | ||

| 00:30 | AUD | House Price Index Q/Q Q3 | -0.20% | 0.50% | 1.90% | |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 0.20% | -0.20% | ||

| 09:30 | GBP | CPI M/M Nov | 0.20% | 0.10% | ||

| 09:30 | GBP | CPI Y/Y Nov | 3.00% | 3.00% | ||

| 09:30 | GBP | Core CPI Y/Y Nov | 2.70% | 2.70% | ||

| 09:30 | GBP | RPI M/M Nov | 0.30% | 0.10% | ||

| 09:30 | GBP | RPI Y/Y Nov | 4.00% | 4.00% | ||

| 09:30 | GBP | PPI Input M/M Nov | 1.50% | 1.00% | ||

| 09:30 | GBP | PPI Input Y/Y Nov | 6.70% | 4.60% | ||

| 09:30 | GBP | PPI Output M/M Nov | 0.30% | 0.20% | ||

| 09:30 | GBP | PPI Output Y/Y Nov | 3.00% | 2.80% | ||

| 09:30 | GBP | PPI Output Core M/M Nov | 0.20% | 0.10% | ||

| 09:30 | GBP | PPI Output Core Y/Y Nov | 2.20% | 2.10% | ||

| 09:30 | GBP | House Price Index Y/Y Oct | 5.20% | 5.40% | ||

| 10:00 | EUR | German ZEW Economic Sentiment Dec | 17.9 | 18.7 | ||

| 10:00 | EUR | German ZEW Current Situation Dec | 88.7 | 88.8 | ||

| 10:00 | EUR | German ZEW Expectations Dec | 18 | 18.7 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 30.2 | 30.9 | ||

| 11:00 | USD | NFIB Small Business Optimism Nov | 104 | 103.8 | ||

| 13:30 | USD | PPI M/M Nov | 0.40% | 0.40% | ||

| 13:30 | USD | PPI Y/Y Nov | 3.00% | 2.80% | ||

| 13:30 | USD | PPI Core M/M Nov | 0.20% | 0.40% | ||

| 13:30 | USD | PPI Core Y/Y Nov | 2.40% | 2.40% | ||

| 19:00 | USD | Monthly Budget Statement Nov | -135.2B | -63.2B |