Markets are rather quiet as they start the pre-holiday week. Dollar attempts to rally on news of the tax bill, but there is little momentum seen. Yen trade broadly softer despite positive trade data. Weakness in Swiss Franc and Yen suggest that markets are in mild risk seeking mode. Aussie and Kiwi are generally firmer, followed by Euro. But overall, the forex markets are generally staying in Friday’s range, without a clear direction.

House and Senate to vote on final tax bill this week

The Republicans have finally finalized the reconciliation of the tax plans last Friday. A summary could be found in the Tax Cuts and Jobs Act policy highlights. The most significant development was that Sens. Marco Rubio of Florida and Bob Corker of Tennessee both changed their minds and expressed the support for the bill. Even though John McCain could miss the vote due to health reason, its now looks like there will be enough vote in the Senate for passing the bill. Treasury Secretary Steven Mnuchin said on Sunday that he has "no doubt" that the bill will be passed this week. And President Donald Trump is expected to sign it next week.

Japan trade surplus widened

Japan adjusted trade surplus widened to JPY 364b in November, above expectation of JPY 270b. Exports rose 14.7% yoy while import rose 17.2% yoy. Increase in exports were broad based. Exports to China rose 25% yoy, to US rose 13% yoy, to EU also rose 13% yoy. The data adds to the case that the export-led Japanese economy is on track for gradual recovery.

Looking ahead

BoJ meeting will be a major focus of the week. With core CPI standing at 0.8%, there is little room for BoJ to talk about exiting stimulus. The central bank will maintain policies unchanged and pledge to drive inflation back to 2% target. RBA minutes for December meeting will likely reveal policymakers’ concern over subdued wage growth. While trading would likely be subdued in pre-holiday week, some data might trigger volatility in the markets. German Ifo, New Zealand trade balance and GDP, Canada CPI, retail sales and GDP, US durable goods and PCE will be watched.

Here are some highlights for the week ahead

- Monday: Eurozone CPI final, UK CBI trends total orders; Canada foreign securities transactions; US NAHB housing index

- Tuesday: RBA minutes; German Ifo business climate: US housing starts and building permits, current account

- Wednesday: New Zealand trade balance; Japan all industry index; German PPI; Eurozone current account; UK CBI realized sales; Canada wholesale sales; US existing home sales

- Thursday: New Zealand GDP; BoJ rate decision; Swiss trade balance; UK public sector net borrowing; Canada CPI, retail sales; US Q3 GDP final, jobless claims, Philly Fed survey, house price index, leading indicator

- Friday: German Gfk consumer sentiment; Swiss KOF economic barometer; UK current account, Q3 GDP final; Canada GDP; US durable goods orders, personal income and spending, new home sales

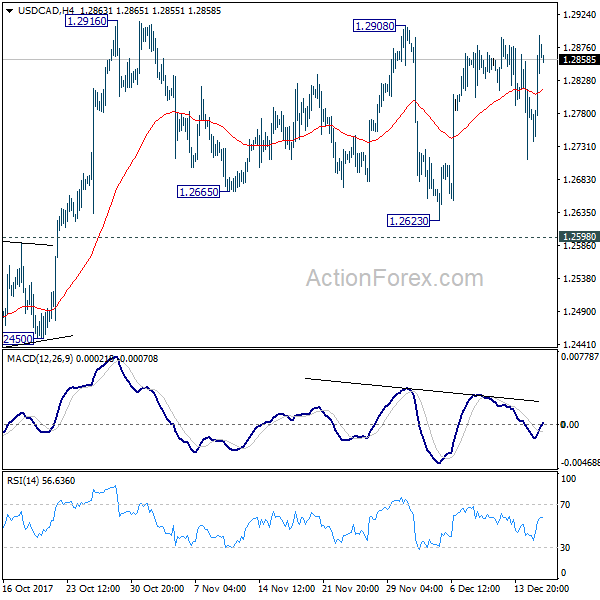

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2774; (P) 1.2834; (R1) 1.2929; More….

Intraday bias in USD/CAD remains neutral as sideway consolidation from 1.2916 might extend further. But after all, with 1.2598 resistance turned support intact, outlook remains bullish and further rally is expected. On the upside, break of 1.2916 will resume the rise from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2885). Near term outlook will be turned bearish in this case.

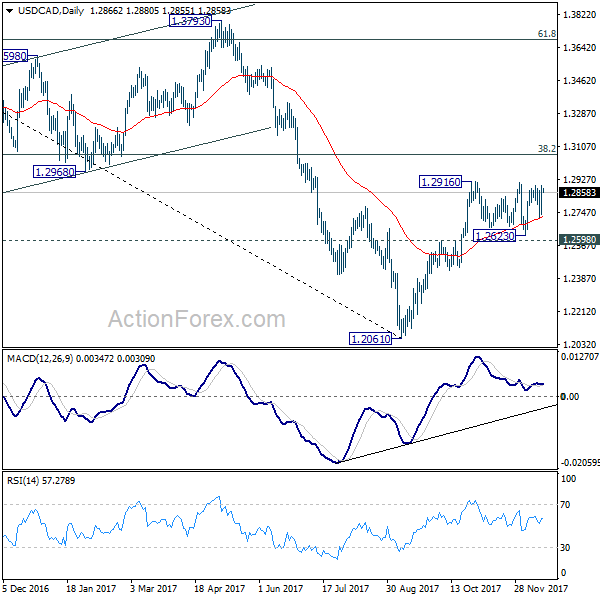

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we’d favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We’ll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance Nov | 0.36T | 0.27T | 0.32T | 0.35T |

| 10:00 | EUR | Eurozone CPI M/M Nov | 0.10% | 0.10% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | 1.50% | 1.50% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov F | 0.90% | 0.90% | ||

| 11:00 | GBP | CBI Trends Total Orders Dec | 15 | 17 | ||

| 13:30 | CAD | International Securities Transactions (CAD) Oct | 16.81B | |||

| 15:00 | USD | NAHB Housing Market Index Dec | 70 | 70 |