{kind=link}

Risk appetite returned as DOW staged the a 200 points swing in the biggest intraday comeback in near nine months overnight. Major indices ended higher with DOW gained 0.26%, S&P 500 rose 0.08% and NASDAQ added 0.30%. 10 year yield dived to as low as 2.091 but pared back much losses to close down -0.023 at 2.136. Dollar also stabilized and recovered after intraday selloff. Some analysts attributed the rebound to the lack of escalation out of US regarding North Korea’s firing of missile over Japan. US President just said that all options are on the table, without any follow up. Nikkei follows by gaining near to 100 pts in Asia at the time of writing. Gold also retreated from intraday high at 1331.9 and is back below 1320.

UNSC condemned North Korea for its outrageous actions

The United Nations Security Council issued a condemned Presidential Statement and condemned North Korea for its "outrageous actions. This is in response to the ballistic missile launch yesterday over Japan and a series of launches on August 25. UNSC demanded that the North-East Asia country "immediately cease all such actions." UNSC warned that the actions were "not just a threat to the region" but to "all UN Member States". And such actions "deliberately undermining regional peace and stability and have caused grave security concerns around the world." UNSC also demanded North Korea to "abandon all nuclear weapons and existing nuclear programs in a "in a complete, verifiable and irreversible manner, and immediately cease all related activities".

Fed fund futures pricing in Fed cut again

After the destruction by hurricane Harvey in US and the sudden intensification of geopolitical tensions, markets are starting to price in Fed cut again. Current fed fund futures are pricing 2.7% chance of a cut in September FOMC meeting, and 97.3% chance of standing pat. There is 0% chance priced in for a hike. For December FOMC meeting, there is 1.7% chance for a cut, 61.9% chance of standing pat, and 36.4% chance of a high. Fed is still widely expected to continue with its plan to announce unwinding of balance sheet in September. But low inflation and uncertainty over growth could keep Fed’s hands tied. And some interprets fed fund futures pricing as Fed won’t move until end at least June. And between now and the end of 2018, there could be just one more rate hike.

No constructive news from Brexit negotiation yet

As the third round of Brexit negotiation carries on in Brussels, there is so far no constructive news out of the meeting yet. It’s reported that UK’s Brexit Secretary David Davis is demanding legal clarification on the principles EU uses to calculate the divorce bill. And UK is determined not to table a figure as it’s perceived as a poor negotiation tactic. UK Prime Minister Theresa May’s spokeswoman Alison Donnelly reiterated that May would like to move on to "future relationship" as there are lots of issues that "you can’t separate between withdrawal and future relationship." And she reiterated that "our desire is to discuss both at the same time: we’ve repeatedly said that, and that’s what we’re working towards."

On the other hand, European Commission President Jean-Claude Juncker criticized that "none" of UK’s positions papers on Brexit is "satisfactory. He complained that "the UK government is hesitant in showing all its cards." EU is also clear that there will be no talks on trade agreement before settling some key issues, including the divorce bill. Juncker emphasized again that "first of all we settle the past before we look forward to the future."

There are only two more rounds of talks scheduled before EU summit in October. EU officials would then decide whether significant progress is made to move on to trade agreements. But based on the current lack of progress, it’s highly unlikely to for the negotiations to meet the deadline. It’s reported that UK wants to squeeze in more sessions to pick up the pace.

China hit back on IMF criticism on debt

Earlier in the month, IMF criticized China for boosting growth with cost of "further large and continuous increases in private and public debt" that increases downside risks in the medium term. And IMF warned that China’s credit growth was on a "dangerous trajectory". But said Yu Yongding, an economist of the Chinese Academy of Social Sciences, hit back and said that IMF’s conclusion was "out of line with China’s real situation." Yu urged China not to adopt IMF;s suggests on reforms to cut the debt levels. Yu pointed out that China has been resilient in coping with the debt problem. And, a government debt-to-GDP ratio at 36.7% is already lower than most major industrialized and emerging-market economies. On the other hand, rushing to solve the debt problem in hasty manner could risk dampening growth.

Staying in China, the two key phenomena, tightening in liquidity condition and renminbi strength, in the Chinese market have persisted. Last week, PBOC auctioned RMB 80B of 3-month Treasury deposits at 4.51%, the highest since December 2014. This came in after another auction of 3-month Treasury deposits on August 18, at 4.46%. Higher interest rates signaled that the government is trying to increase the borrowing cost, tightening money supply. Indeed, liquidity conditions have remained tight in China, with both interbank rates and bond yields higher. Renminbi firmed, thanks to the broad-based weakness in the greenback and the Chinese government’s capital control measures. USDCNY fixing has fallen to 6.6293, lowest level since August 2016, on Tuesday. The current liquidity environment and renminbi strength are in line with PBOC’s "prudent and neutral" monetary policy stance, with the main goal of "deleveraging". More in China’s Monetary Conditions Remain Tight as Deleveraging in Progress.

On the data front

Japan retail sales rose 1.9% yoy in July. Australia construction work done rose 9.3% in Q2, building approvals dropped -1.8% mom in July. New Zealand building permits dropped -0.7% mom in July. UK BRC shop price index dropped -0.3% yoy in August. Swiss UB consumption indicator and KOF leading indicator will be featured in European session. UK will release mortgage approvals and M4 money supply. Eurozone will release confidence indicators. German will release August CPI flash. From US, main focus will be on ADP employment and GDP revision.

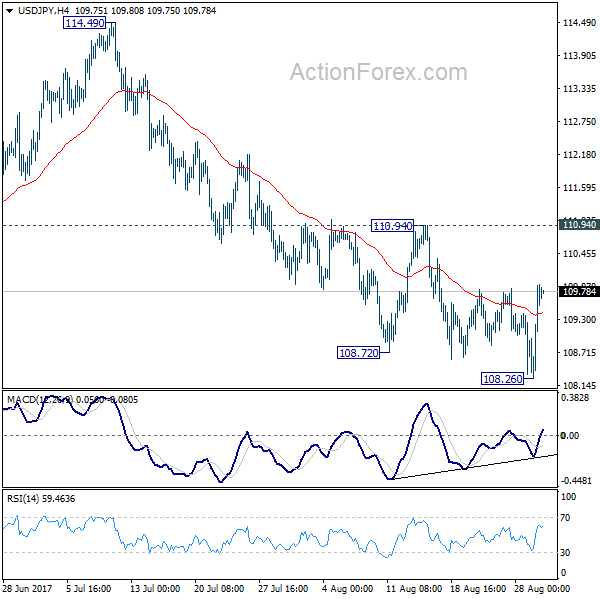

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.69; (P) 109.30; (R1) 110.34; More…

USD/JPY staged a strong rebound after dipping to 108.26 and intraday bias is turned neutral first. Near term stays bearish as long as 110.94 resistance holds and deeper fall is expected. Firm break of 108.12 will resume the whole corrective decline from 118.65. In that case, USD/JPY will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, considering bullish convergence condition in 4 hour MACD, break of 110.94 will indicate near term reversal and bring stronger rebound back towards 114.49 resistance.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it’s uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it’s a leg in the consolidation from 125.85. Hence, we’ll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jul | -0.70% | -1.00% | -1.30% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Aug | -0.30% | -0.40% | ||

| 23:50 | JPY | Retail Trade Y/Y Jul | 1.90% | 1.00% | 2.10% | 2.20% |

| 1:30 | AUD | Construction Work Done Q2 | 9.30% | 1.00% | -0.70% | 0.90% |

| 1:30 | AUD | Building Approvals M/M Jul | -1.70% | -5.00% | 10.90% | 11.70% |

| 6:00 | CHF | UBS Consumption Indicator Jul | 1.38 | |||

| 7:00 | CHF | KOF Leading Indicator Aug | 107 | 106.8 | ||

| 8:30 | GBP | Mortgage Approvals Jul | 65.5k | 64.7k | ||

| 8:30 | GBP | M4 Money Supply M/M Jul | 0.40% | -0.20% | ||

| 9:00 | EUR | Eurozone Business Climate Indicator Aug | 1.05 | 1.05 | ||

| 9:00 | EUR | Eurozone Economic Confidence Aug | 111.3 | 111.2 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Aug | 4.7 | 4.5 | ||

| 9:00 | EUR | Eurozone Services Confidence Aug | 13.9 | 14.1 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Aug F | -1.5 | -1.5 | ||

| 12:00 | EUR | German CPI M/M Aug P | 0.10% | 0.40% | ||

| 12:00 | EUR | German CPI Y/Y Aug P | 1.80% | 1.70% | ||

| 12:15 | USD | ADP Employment Change Aug | 188K | 178K | ||

| 12:30 | USD | GDP (Annualized) Q2 S | 2.70% | 2.60% | ||

| 12:30 | USD | GDP Price Index Q2 S | 1.00% | 1.00% | ||

| 14:30 | USD | Crude Oil Inventories | -3.3M |