Live Comments

UK PMI Composite Returns to Expansion at 52.1 as Manufacturing Leads Strongest Growth in Nearly Two Years

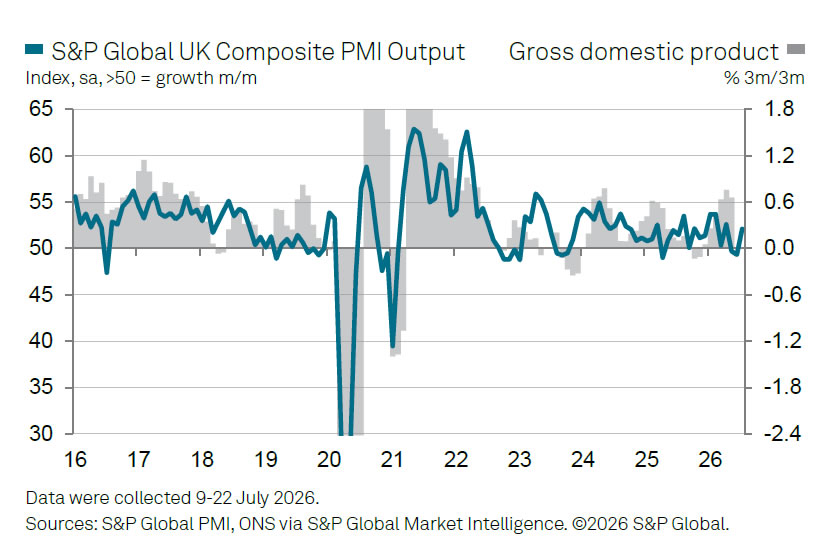

UK private-sector activity returned to expansion in July, with the Flash Composite PMI rising to 52.1 from 49.3, its highest level in three months. Both manufacturing and services improved, marking the first expansion in overall business activity since April. The survey points to a firmer start to the third quarter, supported by stronger domestic demand and resilient export activity.

Manufacturing remained the standout performer. The Manufacturing Output Index climbed to 53.6 from 52.6, its highest level in 22 months, while the Manufacturing PMI edged up to 52.8 from 52.5. Services also returned to growth, with the Business Activity Index rising to 51.8 from 48.8, helped by warm weather, the FIFA World Cup and stronger domestic tourism. However, S&P Global noted that services growth remained relatively subdued as cost-of-living pressures continued to weigh on household spending, while part of the manufacturing strength reflected precautionary inventory building linked to Middle East-related supply chain disruptions.

The survey also pointed to easing price pressures as lower oil prices during the first half of July helped moderate input costs, reducing immediate pressure on Bank of England to tighten policy further. Nevertheless, inflation remained elevated due to the broader energy shock and supply constraints, while businesses continued to reduce headcount as higher costs weighed on hiring.

Business confidence improved during the survey period as geopolitical tensions temporarily eased, but renewed instability in the Middle East and rising oil prices could yet challenge both the inflation outlook and the durability of the recovery.

Economic Data

| Component | Current | Previous | Trend |

|---|---|---|---|

| Composite PMI Output | 52.1 | 49.3 | ▲ 3-month high |

| Services PMI Business Activity | 51.8 | 48.8 | ▲ 3-month high |

| Manufacturing Output Index | 53.6 | 52.6 | ▲ 22-month high |

| Manufacturing PMI | 52.8 | 52.5 | ▲ 2-month high |

Key Takeaways

- UK Composite PMI rose from 49.3 to 52.1, moving back into expansion territory for the first time since April and signaling a stronger start to Q3.

- Manufacturing continued to outperform services, with the Manufacturing Output Index climbing to 53.6, its highest level in 22 months.

- Manufacturing PMI edged up from 52.5 to 52.8, indicating factory activity remained firmly in expansion.

- Services returned to growth, with the Business Activity Index rising from 48.8 to 51.8, supported by warm weather, the FIFA World Cup and stronger domestic holiday spending.

- Manufacturing growth was also supported by precautionary inventory building, as firms sought to mitigate supply chain risks linked to the Middle East conflict, raising questions about the sustainability of the recent factory rebound.

- Input cost inflation eased during the first half of July as oil prices softened, reducing immediate pressure on the Bank of England to tighten policy further.

- However, businesses continued to report elevated cost pressures, ongoing job losses and uncertainty related to energy markets and geopolitical tensions.

- Business optimism improved to its highest level in several months, though renewed increases in oil prices and shipping disruptions could quickly reverse recent gains.

Eurozone PMI Composite Rebounds to 51.6 as Manufacturing Powers Strongest Growth Since 2022

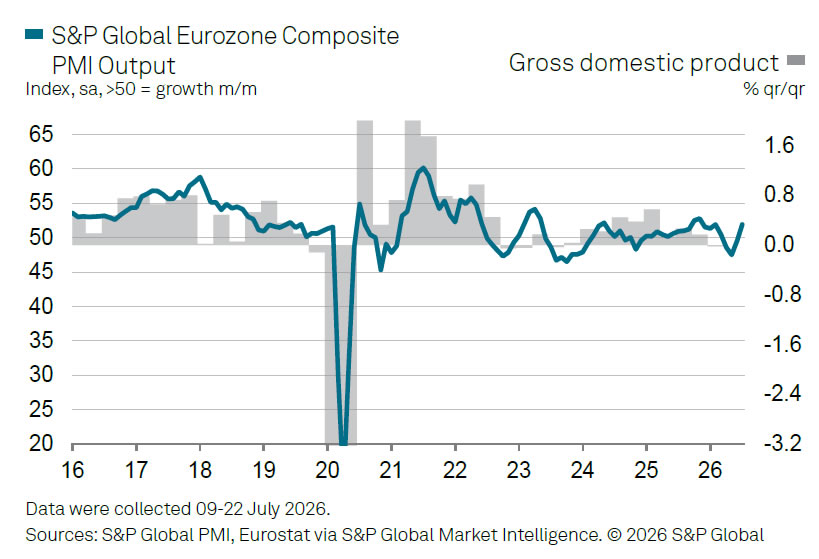

Eurozone business activity returned to expansion in July, with the Flash Composite PMI rising to 51.9 from 50.0, its highest level in five months and signaling the first increase in private-sector output in four months. The improvement was broad-based, driven by a rebound in services and a further acceleration in manufacturing, suggesting the economy has entered the third quarter on firmer footing after stagnating through much of Q2.

Manufacturing was the standout performer. The Manufacturing PMI rose to 52.0 from 51.4, while the Manufacturing Output Index climbed to 53.0 from 51.7, marking the strongest production growth since March 2022. Services also returned to expansion, with the Services PMI Business Activity Index rising to 51.6 from 49.4 after three consecutive months of contraction. According to S&P Global, stronger demand lifted activity across sectors and was accompanied by the first increase in employment this year, while business confidence improved to its highest level since February.

Regional performance also became more encouraging. Germany returned to growth for the first time in four months, with its Composite PMI rising to 51.2 from 49.5, supported by a surge in manufacturing where the output index jumped to 54.7, the highest in more than four years. France remained the weakest of the major economies, but its Composite PMI improved to 49.6 from 47.2, indicating that the downturn moderated considerably. Meanwhile, the rest of the Eurozone recorded its strongest expansion in eight months, pointing to a broader improvement beyond the region's two largest economies.

The survey also offered encouraging news on inflation. Input cost pressures eased to their lowest level since the outbreak of the Middle East conflict, helping moderate selling price inflation across both manufacturing and services. That should reduce immediate pressure on ECB to tighten policy further. Nevertheless, the outlook remains closely tied to developments in the Middle East. Renewed increases in oil prices and rising shipping disruptions could quickly revive inflationary pressures and disrupt supply chains, threatening what is still a fragile recovery.

Economic Data

Eurozone Flash PMI (July)

| Component | Current | Previous | Trend |

|---|---|---|---|

| Composite PMI Output | 51.9 | 50.0 | ▲ 5-month high |

| Services PMI Business Activity | 51.6 | 49.4 | ▲ 5-month high |

| Manufacturing Output Index | 53.0 | 51.7 | ▲ 52-month high |

| Manufacturing PMI | 52.0 | 51.4 | ▲ 3-month high |

Germany Flash PMI (July)

| Component | Current | Previous | Trend |

|---|---|---|---|

| Composite PMI Output | 51.2 | 49.5 | ▲ 4-month high |

| Services PMI Business Activity | 49.6 | 48.6 | ▲ 4-month high |

| Manufacturing Output Index | 54.7 | 51.6 | ▲ 53-month high |

| Manufacturing PMI | 52.2 | 50.3 | ▲ 4-month high |

France Flash PMI (July)

| Component | Current | Previous | Trend |

|---|---|---|---|

| Composite PMI Output | 49.6 | 47.2 | ▲ 5-month high |

| Services PMI Business Activity | 49.8 | 46.8 | ▲ 7-month high |

| Manufacturing Output Index | 48.8 | 49.1 | ▼ 2-month low |

| Manufacturing PMI | 50.0 | 51.2 | ▼ 2-month low |

Key Takeaways

- Eurozone Composite PMI rose from 50.0 to 51.9, the highest in five months, signaling the first expansion in business activity in four months.

- Manufacturing remained the main growth engine, with the Manufacturing Output Index climbing to 53.0, the strongest reading since March 2022.

- Services also returned to expansion, with the Business Activity Index rising from 49.4 to 51.6 after three months of contraction.

- Germany returned to expansion for the first time in four months, driven by a sharp acceleration in manufacturing output to a 53-month high.

- France remained just below the 50 threshold, but the pace of contraction eased significantly as services stabilized.

- The broader euro area outside Germany and France recorded its strongest expansion in eight months, suggesting the recovery is becoming more widespread.

- Firms reported the first increase in employment this year, supported by stronger demand and improved business confidence.

- Input cost inflation eased to its lowest level since the Middle East conflict began, helping moderate selling price inflation and reducing immediate pressure on the ECB to tighten policy further.

- Rising oil prices and shipping disruptions linked to Middle East tensions remain the principal downside risk to the recovery, with renewed energy inflation capable of derailing the nascent rebound.

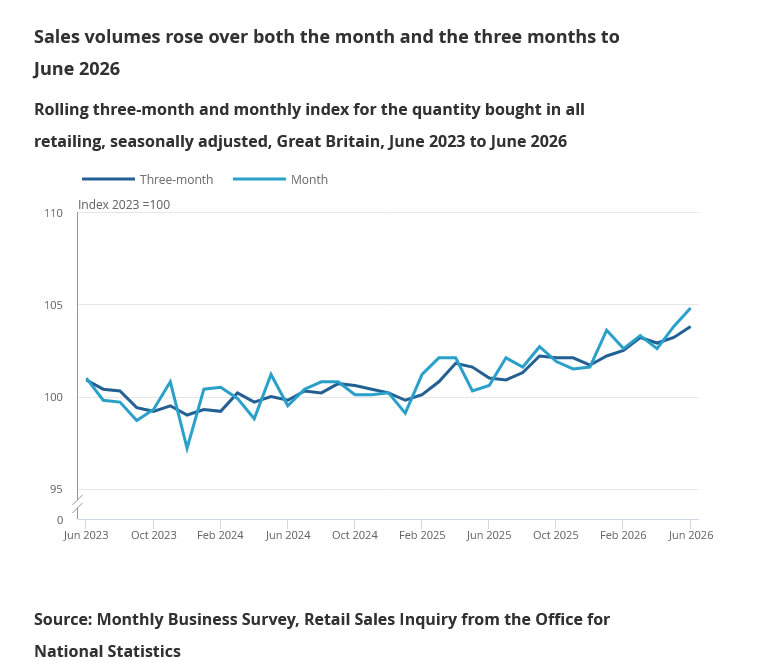

UK Retail Sales Surge 1.0% mom as Online Spending Leads Broad-Based June Rebound

UK retail sales volumes jumped 1.0% mom in June, far exceeding expectations for a -0.3% mom decline, following an unrevised 1.2% mom increase in May. The stronger-than-expected performance points to resilient consumer demand despite elevated borrowing costs and persistent cost-of-living pressures. Retailers credited sales promotions and warm weather for boosting spending, particularly at online and clothing retailers.

The gains extended beyond the headline figure. Excluding automotive fuel, retail sales rose 1.1% mom, while volumes increased 1.2% qoq in Q2. Non-store retailing was the standout performer, with sales surging 4.4% mom and 3.8% qoq, reflecting strong online demand. Other non-food stores also posted solid gains, while clothing retailers rebounded 1.9% mom after recent weakness. Food sales edged higher, suggesting spending strength was relatively broad-based across consumer categories.

Fuel sales was the notable weak spot, falling -0.8% mom and 6.0% qoq as higher pump prices continued to weigh on demand following the Middle East-related stockpiling seen in March. Overall, the report suggests UK consumers remain willing to spend selectively when supported by discounts and seasonal factors, reinforcing the view that household consumption continues to provide a cushion for the economy.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Retail Sales mom (Jun) | 1.0% | -0.3% | 1.2% |

| Retail Sales ex-Fuel mom (Jun) | 1.1% | — | — |

| Retail Sales qoq (Q2 vs Q1) | 0.6% | — | — |

| Retail Sales ex-Fuel qoq (Q2 vs Q1) | 1.2% | — | — |

Category Breakdown

| Component | June mom | Q2 vs Q1 | Trend |

|---|---|---|---|

| Non-store Retailing | 4.4% | 3.8% | ▲ Strong |

| Textile, Clothing & Footwear | 1.9% | -0.1% | ▲ Rebounded |

| Other Non-food Stores | 1.8% | 1.2% | ▲ Strong |

| Food Stores | 0.3% | 0.3% | ▲ Modest |

| Household Goods Stores | -0.6% | 2.9% | Mixed |

| Department Stores | -1.7% | 1.6% | Mixed |

| Automotive Fuel | -0.8% | -6.0% | ▼ Weak |

Key Takeaways

- UK retail sales rose 1.0% mom in June, sharply beating expectations for a -0.3% decline.

- May's 1.2% mom gain was unrevised, while April was revised up to -0.7% mom from -1.0% mom.

- Excluding automotive fuel, retail sales increased 1.1% mom, indicating that the strength was broad-based rather than driven by volatile fuel sales.

- Retail sales volumes rose 0.6% in Q2 from Q1, or 1.2% excluding fuel, pointing to resilient household spending through the quarter.

- Online retailers were the standout performer, with non-store sales jumping 4.4% mom and 3.8% qoq, helped by sales promotions and warm weather.

- Clothing retailers rebounded 1.9% mom, while other non-food stores also posted solid gains.

- Fuel sales remained the weakest segment, falling -0.8% mom and -6.0% qoq after motorists cut back following March's conflict-driven stockpiling and subsequent rise in pump prices.

- The report suggests UK consumers continue to spend selectively despite high interest rates, reinforcing the resilience of domestic demand.