Live Comments

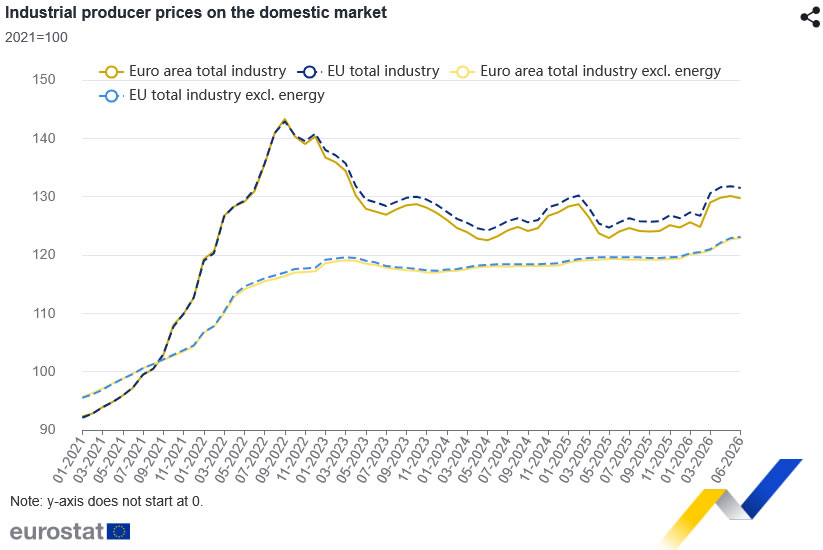

Eurozone PPI Falls -0.3% M/M on Cheaper Energy, Core Producer Prices Still Rise

Eurozone producer prices fell in June as lower energy costs outweighed continued increases across most other industrial sectors, suggesting pipeline inflation eased but remained far from disappearing. Industrial producer prices declined -0.3% m/m, matching expectations and reversing May's 0.2% increase, while the annual rate slowed from 5.9% to 4.6%. The figures largely reflected the period of lower oil prices during June before renewed volatility in energy markets emerged in July.

The decline was driven almost entirely by the energy sector, where producer prices dropped -1.5% m/m. By contrast, underlying price pressures remained positive across much of the industrial economy. Intermediate goods prices rose 0.3%, while capital goods and durable consumer goods each increased 0.2%. Excluding energy, producer prices actually rose 0.2%, indicating that manufacturing cost pressures continued to build despite the headline decline.

The data broadly reinforce the message from this week's PMI surveys that inflation pressures are moderating. Slower producer price growth should offer some reassurance for the ECB, but the persistence of positive ex-energy inflation suggests underlying pricing power remains intact. With oil prices having rebounded after June before easing again this week on renewed hopes of a Strait of Hormuz agreement, policymakers are likely to view the report as evidence of gradual disinflation rather than a decisive turning point.

Data Summary

| Indicator | June 2026 | May 2026 | Trend |

|---|---|---|---|

| PPI M/M | -0.3% | +0.2% | ▼ First monthly decline since February |

| PPI Y/Y | 4.6% | 5.9% | ▼ Annual inflation eased |

| PPI Ex-Energy M/M | +0.2% | +0.7% | ▲ Underlying prices still rising |

| Intermediate Goods M/M | +0.3% | +1.4% | ▲ Positive but slower |

| Energy M/M | -1.5% | -1.0% | ▼ Main drag on headline |

| Capital Goods M/M | +0.2% | +0.3% | ▲ Continued increase |

| Durable Consumer Goods M/M | +0.2% | +0.3% | ▲ Continued increase |

| Non-Durable Consumer Goods M/M | 0.0% | -0.1% | ► Stable |

Key Takeaways

- Eurozone producer prices fell 0.3% m/m in June, exactly in line with expectations, while annual producer inflation slowed to 4.6% from 5.9%.

- The decline was almost entirely driven by a 1.5% fall in energy prices, reflecting the period of lower oil prices during June.

- Underlying pipeline inflation remained intact. Producer prices excluding energy rose 0.2%, while intermediate goods, capital goods and durable consumer goods all recorded monthly increases.

- The report reinforces this week's PMI surveys, which also showed easing—but not disappearing—cost pressures across the Eurozone.

- As the data predate July's renewed volatility in oil markets, policymakers are likely to treat the report as backward-looking while continuing to monitor the impact of recent geopolitical developments on energy prices.

- Overall, the release supports the view of gradual disinflation rather than a collapse in producer price pressures, leaving the ECB room to remain patient.

Full Eurozone PPI release here.

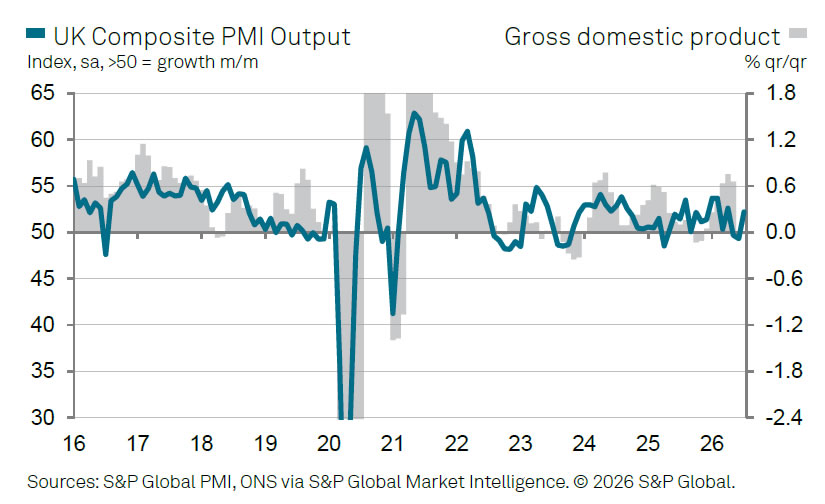

UK Services PMI Returns to Growth, but Record Job Losses Cast Shadow

The UK's private sector returned to growth in July as the services sector rebounded after two months of contraction. The S&P Global UK Services PMI rose to 52.1 from 48.8 in June, while the Composite PMI climbed to 52.2 from 49.3, marking the first expansion in overall business activity since April. Higher consumer spending and robust demand for technology services helped lift activity, while manufacturing output also recorded its strongest increase since September 2024.

The recovery extended beyond output. New business increased for the first time in five months, reflecting gradually improving market conditions, although the pace of growth remained modest by historical standards. Survey respondents continued to cite geopolitical uncertainty and the conflict in the Middle East as constraints on demand, despite signs that clients had become less risk-averse. Encouragingly, business confidence improved for a second consecutive month, reaching its highest level since February as firms looked for further easing in inflation pressures and geopolitical tensions.

One area that continues to lag is the labour market. Employment declined for a 22nd consecutive month, matching the longest stretch of job losses in the survey's three-decade history, previously seen during the global financial crisis and after the dotcom bust. At the same time, input cost inflation slowed to a five-month low, providing some relief for businesses. The latest survey therefore suggests the UK economy is regaining momentum, but the recovery remains uneven, with stronger demand yet to translate into sustained hiring.

Data Summary

| Component | July 2026 | June 2026 | Trend |

|---|---|---|---|

| Services PMI | 52.1 | 48.8 | ▲ Back in expansion; highest since April |

| Composite PMI | 52.2 | 49.3 | ▲ Returned to expansion |

| Business activity | Expanded | Contracted | Recovery resumed |

| New business | Expanded | Contracted | First rise in five months |

| Business expectations | Highest since February | Improved | ▲ Confidence strengthened |

| Employment | Declined | Declined | ▼ 22nd consecutive monthly fall |

| Input cost inflation | Increased | Increased | ▼ Slowest pace in five months |

| Manufacturing output | Strongest since Sep 2024 | Expanded | ▲ Accelerated |

Key Takeaways

- The UK Services PMI rose to 52.1 and the Composite PMI to 52.2, returning both sectors to expansion for the first time since April.

- Higher consumer spending and solid demand for technology services helped drive the rebound, while manufacturing production recorded its strongest growth since September 2024.

- New orders increased for the first time in five months, suggesting domestic demand is beginning to recover despite ongoing geopolitical uncertainty.

- Business confidence improved for a second consecutive month, reaching its highest level since February on hopes of easing inflation and reduced Middle East tensions.

- The labour market remained the weakest part of the survey, with employment falling for a 22nd straight month, matching the longest period of job losses in the survey's 30-year history.

- Input cost inflation slowed to a five-month low, providing further evidence that price pressures are gradually easing even as logistics challenges persist.

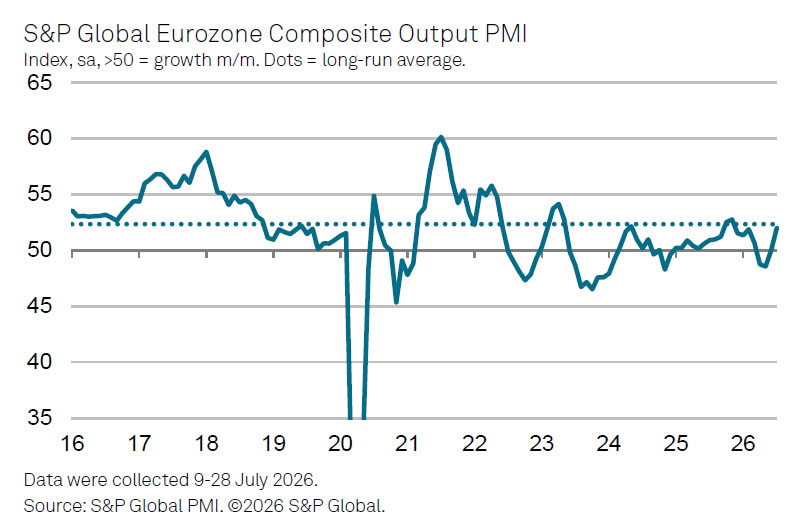

Eurozone Composite PMI Climbs to Eight-Month High, Indicates 0.3% Quarterly GDP Growth

The Eurozone economy gathered momentum at the start of the third quarter, with business activity expanding at its fastest pace in eight months as the services sector returned to growth. The final S&P Global Composite PMI rose to 52.0 in July from 50.0 in June, while the Services PMI climbed to 51.7 from 49.4, its highest level in five months. The survey pointed to the strongest increases in output and new orders since November, suggesting demand is recovering despite continued geopolitical uncertainty.

The improvement was broad-based across the region. Germany led the recovery, with its Composite PMI returning to expansion territory at 51.3 after three months of contraction, supported by a near-stabilization in services activity. France remained a laggard, but conditions improved noticeably as both services and overall private-sector activity moved closer to the 50 threshold, indicating the downturn is steadily easing. The divergence between the Eurozone's two largest economies therefore narrowed further during July.

The survey also offered encouraging news on inflation. Business optimism rose to its highest level since January as demand strengthened and input cost inflation slowed to its weakest pace since February. That combination points to a healthier growth environment without a renewed surge in price pressures. According to S&P Global, the PMI is consistent with around 0.3% quarterly GDP growth, reflecting a recovery that is becoming increasingly broad-based.

However, the outlook remains closely tied to developments in the Middle East. Much of July's improvement followed the temporary easing in oil prices and geopolitical tensions during June. With the conflict having intensified again since then, risks to both growth and inflation have resurfaced. While the moderation in PMI price gauges could give the ECB room to delay further policy tightening until the inflation outlook becomes clearer, policymakers are unlikely to become complacent given the renewed uncertainty surrounding energy markets.

Data Summary

| Component | July 2026 | June 2026 | Trend |

|---|---|---|---|

| Eurozone Composite PMI | 52.0 | 50.0 | ▲ 8-month high |

| Eurozone Services PMI | 51.7 | 49.4 | ▲ 5-month high |

| Output | Expanded | Expanded | Strongest since November |

| New Orders | Expanded | Expanded | Strongest since November |

| Business Optimism | Highest since January | Improved | ▲ Stronger confidence |

| Input Cost Inflation | Slowed | Faster | ▼ Slowest since February |

Major Economies

| Economy | Services PMI | June | Composite PMI | June | Assessment |

|---|---|---|---|---|---|

| Germany | 49.8 | 48.6 | 51.3 | 49.5 | Composite returned to expansion |

| France | 49.6 | 46.8 | 49.4 | 47.2 | Contraction eased markedly |

Key Takeaways

- The Eurozone Composite PMI climbed to 52.0, its highest level in eight months, while the Services PMI returned to expansion at 51.7, the strongest reading in five months.

- Output and new orders recorded their fastest growth since November, pointing to improving demand at the start of the third quarter.

- Germany led the recovery, with its Composite PMI returning above 50 for the first time since March, while France remained in contraction but showed a notable improvement.

- Business confidence strengthened to its highest level since January, supported by improving demand and easing cost pressures.

- Input cost inflation slowed to its weakest pace since February, providing some relief after months of elevated price pressures.

- S&P Global estimates the survey is consistent with around 0.3% q/q GDP growth, although renewed Middle East tensions and higher oil prices have reintroduced downside risks to growth and upside risks to inflation.