Here are the latest developments in global markets:

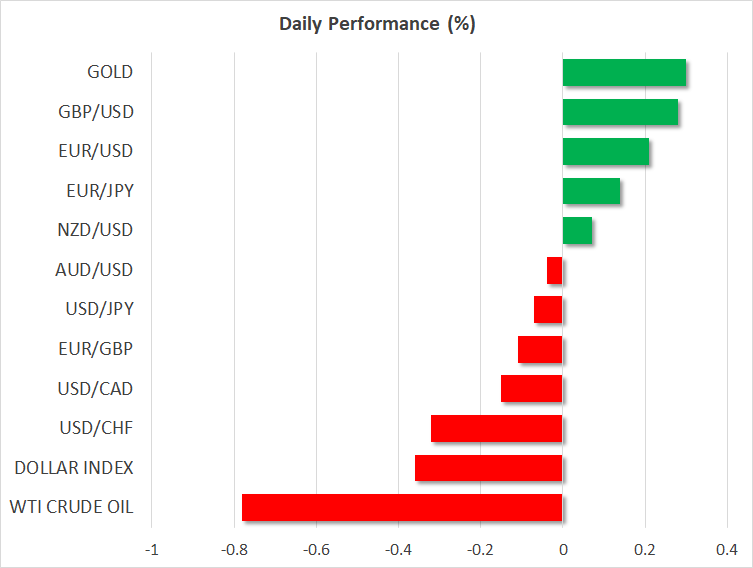

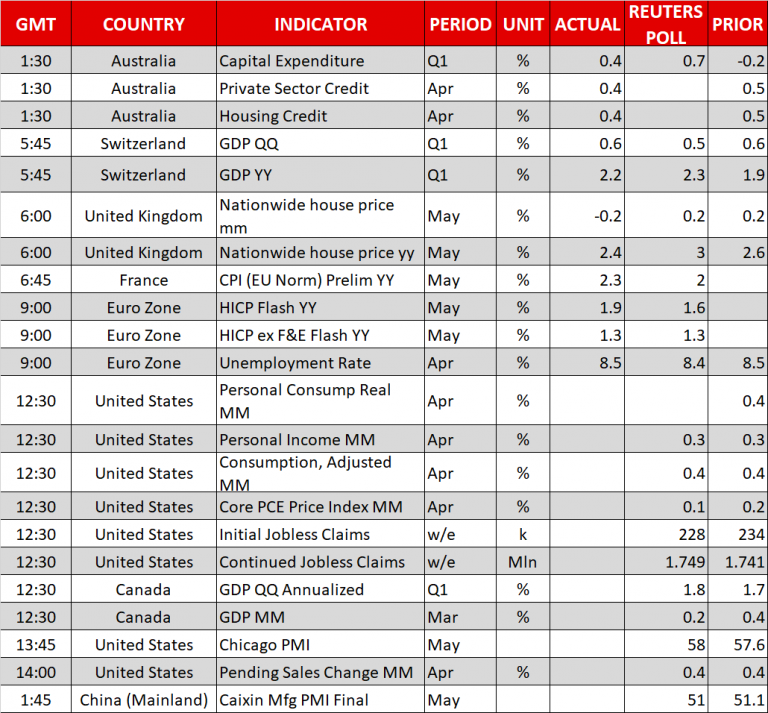

FOREX: The euro extended its gains on Thursday by 0.33% against the US dollar as Italian bond yields fell amid signs that Italy is trying to form a government, potentially avoiding an early election. In terms of data, the Eurozone CPI rose by 1.9% y/y in May above April’s growth mark of 1.2%, while the unemployment rate decreased to 8.5% in April, following an upwardly revised 8.6% in March, compared with the forecast of 8.4%. Dollar/yen moved lower by 0.06% at 1100 GMT, while the US dollar index is set to post the second red day in a row (-0.34%). Pound/dollar advanced by 0.33% and jumped above the 1.3300 handle following the rebound from a 6-month low on Tuesday. The antipodean currencies traded mixed with aussie/dollar down at 0.7574 (-0.03%) and kiwi/dollar slightly up, near the 3-week high of 0.7003 (+0.07%). Dollar/loonie recorded one of the biggest sell-off days in two weeks yesterday after the BoC’s more-hawkish-than-expected rate statement. Today, the pair dipped by 0.21% to 1.2841.

STOCKS: European stocks were moving up at 1100 GMT except the German DAX 30 as the Italian political environment calmed due to new plans for a coalition government. The benchmark European STOXX 600 and the blue-chip Euro STOXX 50 inched up by 0.14% and 0.05% respectively. The German DAX 30 dived by 0.47%, weighed by consumer cyclicals and utilities, while the French CAC 40 gained 0.18%. The Spanish IBEX 35 increased by 0.45% and the British FTSE 100 edged up by 0.16%. Futures tracking US stock indices were flashing green, pointing to a positive open after a strong bullish day.

COMMODITIES: West Texas Intermediate (WTI) and Brent crude oils dropped on Thursday, after the aggressive rally in the previous session, weighed on by a surprise increase in US API crude oil inventories. There is a possibility that OPEC and other producers may increase output at the June 22 OPEC meeting. WTI plunged by 0.79% to $67.67 and Brent dipped by 0.53% to $77.09. In precious metals, gold prices traded higher by 0.31%, jumping above $1,300 again.

Day ahead: US personal spending, personal income and core PCE index in the spotlight; Canadian GDP growth pending

US personal income and personal spending figures as well as the Fed’s favorite inflation measure, the core Personal Consumption Expenditure index (PCE), will take center stage in the remainder of the day. April’s stats due at 1230 GMT, are expected to show no change in personal spending and income, with the former rising by 0.4% m/m and the latter by 0.3%, as in March. Forecasts for the core PCE index though, suggest a moderate slowdown to a growth of 1.8%y/y compared to a rise of 1.9% in March, the highest mark recorded since July 2012. In case the data surprise to the upside – especially on the consumption front – the dollar could benefit on speculation that the Fed would be more prepared to raise interest rates at least two more times this year. Investors will also take a look at the US Chicago PMI and pending home sales at 1345 GMT and 1400 GMT respectively.

However, gains on the dollar could prove short-lived if uncertainties around US trade protectionism heighten ahead of Friday’s deadline for a waiver from US import tariffs on steel and aluminum. The US had temporarily exempted Canada, Mexico, and the EU from metal import tariffs a month ago, postponing the imposition until June 1. But yesterday a report by the Wall Street Journal stated that Washington was not planning to give away a permanent exemption to its EU counterparts. The announcement on the matter is expected to come later today at a time when the US Commerce Secretary, Wilbur Ross, is preparing to hold a second round of trade talks with Beijing this weekend. Tensions with China intensified yesterday as well, after China responded to US trade threats, saying that it will fight back if the US is looking to start a trade war. On Tuesday, Trump signaled he would move on with new import tariffs on China as a step to protect US intellectual property rights.

Meanwhile regarding the North Korean story, US and North Korean officials are meeting in New York to discuss the future of Pyongyang’s nuclear program as well as a potential summit between the US President, Donald Trump, and the North Korean leader, Kim Jong Un which was canceled by Trump last week. The two-day meeting will conclude today.

In Canada, the focus will turn to GDP growth readings due at 1230 GMT after the Bank of Canada left interest rates unchanged at 1.25% as expected but surprisingly appeared more hawkish on the path of future rate hikes, dropping some cautious wordings from the rate statement. Analysts believe that the economy expanded by 1.8% q/q on an annualized basis in the first quarter of the year, faster than in the previous quarter when it grew by 1.7%. Month-on-month, though, they anticipate GDP growth to ease from 0.4% to 0.3% in March. In case the numbers overcome forecasts, the loonie could extend its rally.

In Italy, political updates will continue to affect the euro as the markets await the League’s leader, Matteo Salvini, to announce whether he is willing to renew efforts to form a new government with the Five-Star Movement, a proposal made on Wednesday by the leader of the Five Star Movement party, Luigi Di Maio. Spain’s political drama is another headwind to the euro. On Friday, the Spanish Prime Minister, Mariano Rajoy will face a no-confidence vote against him, with the parliamentary debate starting from today.

In oil markets, the Energy Information Administration will deliver its weekly report on US oil inventories at 1500 GMT. Projections are for US crude oil inventories to post a decline in the week ending May 25.

As of today’s public appearances, BoC Deputy Governor Sylvain Leduc will be speaking about the Economic Progress Report at 1635 GMT, while at 1700 GMT, Fed Board Governor Lael Brainard, will be commenting at the Forecaster’s Club of New York luncheon. A G7 meeting between finance ministers and central bankers with a theme “Investing in Growth that Works for Everyone” will be also in focus. The meeting is scheduled to conclude on June 2.

Early on Friday at 0130 GMT, Asian traders will see the release of the Chinese Caixin Manufacturing PMIs.

{kind=link}