When the European Central Bank (ECB) announces its rate decision on Thursday at 1145 GMT and President Draghi holds his press conference at 1230 GMT, policymakers will have a delicate job on their hands of signaling that the end of QE is drawing closer. Markets are speculating the Bank may announce a firm end-date to its asset purchases, implying that if officials choose to postpone that decision until July instead, then the euro could come under renewed selling interest on the decision.

Preparing markets for the end of ultra-easy money at a period of slowing momentum in Eurozone’s economy is no easy feat, but if anyone can succeed, it is the “maestro” himself – ECB President Mario Draghi. The Bank has long signaled its asset purchase program (QE) was heading to an end towards the end of this year, with a potential announcement coming in the summer. Recent developments, though, have likely made policymakers more hesitant to move towards the stimulus-exit door.

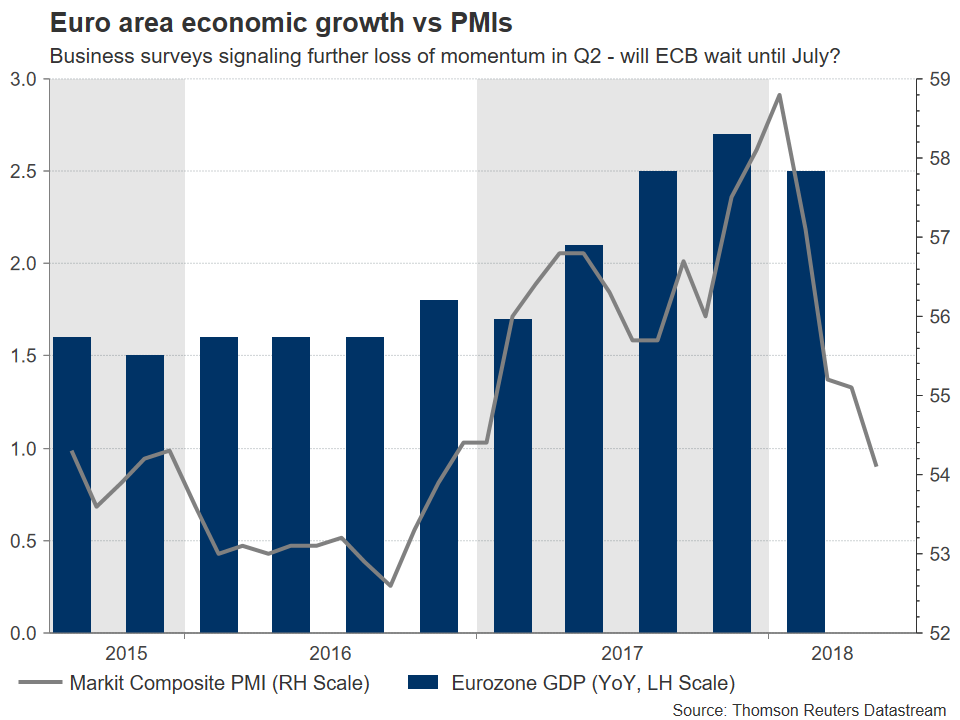

While the bloc’s economy is still expanding at a decent pace, it has lost considerable speed since the start of the year, and forward-looking surveys like the Markit PMIs suggest the slowdown has continued in Q2. While this is discouraging, the Bank still has some reasons to be optimistic. As ECB chief economist Peter Praet recently pointed out, there are signs wages are finally picking up, something considered a prelude to higher inflation. Speaking of Praet, in a rather uncharacteristic move last week, he spearheaded an effort by ECB officials to signal that they will be debating whether and when to end QE when they meet this week. Coming on top of media reports suggesting the Bank could announce a timeline on ending QE completely in June, these helped the euro recover in recent days.

Investors appear to be split on whether a concrete QE end-date will come now, or at the July gathering. Short-term price action in the euro is likely to be dictated by whether the Bank will indeed commit to a timeline, or not. If it does, that would signal policymakers are resolute about normalizing even despite short-term woes, propelling the euro higher. On the contrary, since the currency has been bid up on expectations for such an announcement, a postponement could come as a disappointment and hence push the euro lower.

What is more likely? A middle-of-the-road solution appears the most realistic outcome. Policymakers may express confidence around improving wages and signal that a discussion on a QE-exit did occur, but that nothing has been set in stone yet, keeping some flexibility in case the outlook deteriorates. Essentially, officials could use this meeting as a stepping stone, laying the groundwork for a formal announcement in July, and buying themselves extra time to monitor the economy’s performance. After all, neither Draghi nor the ECB as a whole are keen on pre-committing. A failure to follow through on a policy commitment, for any reason, could cause unwarranted market volatility and damage the Bank’s credibility in the process.

Another area markets will focus on are any signals on how the tapering will occur, meaning at what pace the Bank may reduce its purchases and over what timeframe. The ECB is currently committed to buying assets worth €30 billion/month “until the end of September 2018, or beyond, if necessary” – a much slower pace compared to the €60 billion/month it was buying up until December last year. There are multiple approaches the Bank could employ to end purchases completely, with market chatter suggesting the most likely one is halving them again to €15 billion/month from October to December, and then reducing them to zero.

While the lack of a June action could spell trouble for the common currency on the decision, it may have only limited implications for its broader direction – especially if Draghi and Co set the stage for a July move. In other words, it may not matter much if the announcement comes in June or July – so long as it does come. In the big picture, the coming months are likely to bring a lot of volatility, not least due to trade frictions and potential tensions between Brussels and Rome over EU fiscal rules. That said, the fact that the ECB is set to phase out unconventional measures suggests the longer-term outlook for the euro remains positive on the back of relative interest rates, particularly against the currencies of nations whose central banks aren’t likely to normalize anytime soon, like the yen and Swiss franc.

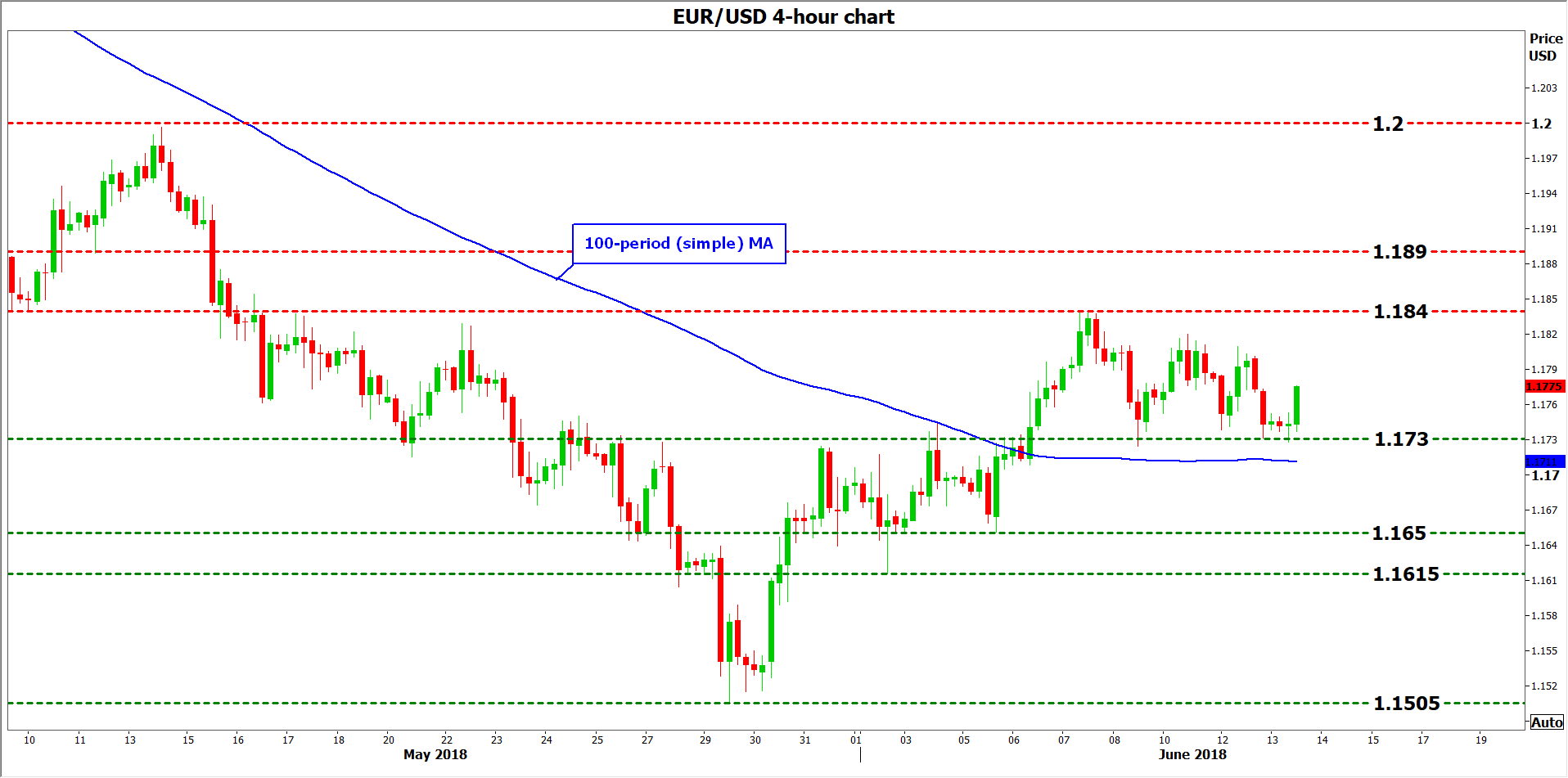

Technically, looking at euro/dollar, support to declines may come around the 1.1730 hurdle, identified by the low of June 12. A downside break would bring into view the 1.1650 level initially and the 1.1615 barrier thereafter, marked by the lows on June 5 and June 3 respectively.

On the other hand, and in case the Bank does provide a timeline for ending QE on Thursday, immediate resistance to advances could be found near the June 7 peak of 1.1840. If the bulls manage to power through it, that could open the way for 1.1890, the May 11 trough, before the attention shifts to the psychological territory of 1.2000.

Finally, it should be noted that the Fed policy decision on Wednesday could impact price action in euro/dollar ahead of the ECB’s own decision on Thursday.