Here are the latest developments in global markets:

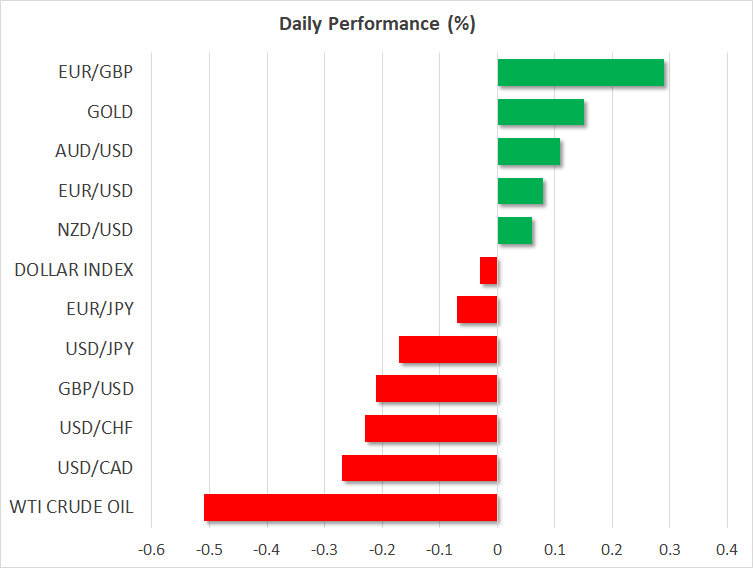

FOREX: A trade war between the US and China, which could harm global trade, got nasty on Friday when China decided to apply a 25% tariff on several US imports (taking effect on July 6) as a response to an extra 25% tariff imposed by Washington on Chinese imports on the same day. Investors turned more cautious thereafter, pushing dollar/yen down to 110.45 (-0.19%) on Monday, while the dollar index which gauges the dollar’s strength against six major currencies stood flat at 94.78 as the euro and the pound remained on the back foot. Euro/dollar was unable to recover after the ECB announced the end of its asset purchase program this year but said that interest rates will remain steady until well into 2019. German political developments were also a concern on Monday, with the German Chancellor, Angela Merkel, facing opposition from her coalition partners, the CSU, over migration ahead of the EU summit this month. Euro/dollar was testing the 1.1600 level (+0.04%). Pound/dollar slipped to 1.3245 (-0.30%), a few days before the Bank of England starts its policy meeting, where policymakers are expected to stand pat on rates. Brexit developments, though, are still holding the largest share of uncertainty as the withdrawal bill has returned to the House of Lords today for a vote, with pro-EU peers expected to reject amendments approved by the House of Commons last week. Euro/pound climbed to 0.8765 (+0.34%) In antipodean currencies, aussie/dollar and kiwi dollar were marginally up at 0.7447 (+0.09%) and 0.6951 (+0.03%) respectively. Dollar/loonie was weaker at 1.3162 (-0.27%) and dollar/swiss franc was lower at 0.9958 (-0.17%) ahead of the SNB rate decision on Thursday.

STOCKS: The risk-off sentiment attributed to trade fears continued to pressure European equities, with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 losing 0.97% and 1.07% respectively at 1150 GMT. The German DAX 30 was down by 1.36%, the French CAC 40 was lower by 1.19%, while the Italian FTSE MIB was falling by 0.69%. Spain’s IBEX 35 retreated by 1.02%, whereas the UK’s FTSE 100 managed to post smoother losses, fell by 0.34% as gains in telecommunications capped steeper downside corrections. Asian stocks closed in bearish territory and futures tracking US stock indices were in the red as well, pointing to a negative open. Markets in China and Hong Kong are shut for a public holiday.

COMMODITIES: Oil prices were mixed early in the European afternoon as traders were weighing a potential increase in supply from Saudi Arabia and Russia, which markets now believe will be smaller than initially expected. The prospect of demand shortages due to the tariff war between the US and China also weighed on prices. Note that China fought back US import tariffs announced on Friday, targeting US export products, including crude oil. Rising tensions in the Libyan oil ports, where rival factions are in a dispute over the control of the Ras Lanuf oil port and ES Sider, provided some support to the market after an oil tank was set on fire. WTI crude was last seen at $64.79/barrel (-0.42%) and Brent at $74.11 (+0.91%). In precious metals, gold remained on the upside on Monday after a sharp fall on Friday, trading at $1,279/ounce (+0.04%).

Day Ahead: Light economic releases ahead of numerous speeches

The calendar will be light of data later on Monday, turning the attention to the rest of the week as the SNB and BOE will announce their interest rate decisions. Also, on Friday OPEC and Russia will have a discussion on whether to relax the oil output cap.

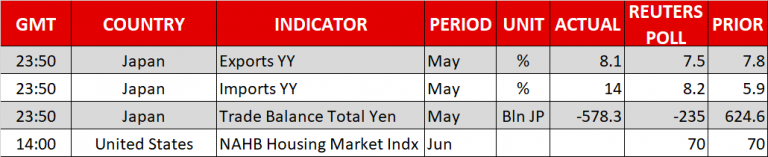

The only notable release today is the US National Association Home Business (NAHB) housing market index for June, which is expected to remain unchanged at 70 at 1400 GMT.

On the political front, German Chancellor Angela Merkel’s Bavarian allies, the Christin Social Union, will decide later today whether to restrict migrants that have already registered in another EU state from entering Germany. Such a move would be against Merkel’s open-door policy and would put the coalition at risk.

In terms of public appearances, retiring Federal Reserve Bank of New York President William Dudley will be participating in a discussion at 1300 GMT. Incoming Federal Reserve Bank of New York President John Williams will be giving a speech at 2000 GMT. Out of Canada, the Bank of Canada Deputy Governor Lynn Patterson will participate at Investment Industry Association of Canada and Institute of International Finance. Investors will also have a close eye on ECB President Mario Draghi’s speech at the ECB Forum on Central Banking in Sintra, Portugal at 1900 GMT.

Overnight at 0130 GMT, the Reserve Bank of Australia (RBA) will release the minutes of June’s Monetary Policy Meeting that left interest rates steady at 1.5%, while earlier in the neighboring country, in New Zealand, the Westpac Banking Corporation will publish Q2 figures on consumer sentiment.