Here are the latest developments in global markets:

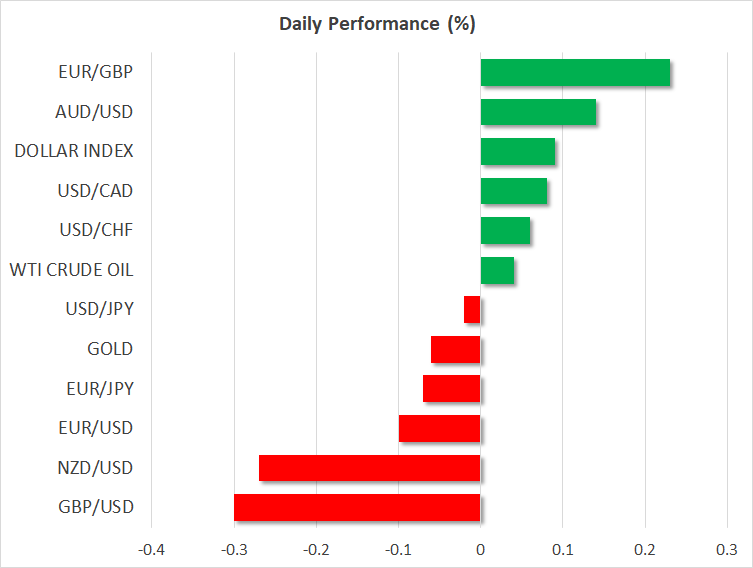

FOREX: The US dollar index is up by almost 0.1% on Friday, building on the gains it posted in the previous session. The yen, meanwhile, is losing ground against all its major counterparts amid an absence of any worrisome news on the trade front, touching a fresh six-month low against the dollar.

STOCKS :US markets closed higher on Thursday, buoyed by the absence of an immediate retaliation from China against the latest US tariff salvo, as well as comments from Treasury Secretary Mnuchin highlighting willingness for negotiations. The tech-heavy Nasdaq Composite soared by 1.39%, posting a new all-time high, while the Dow Jones and S&P 500 advanced by 0.91% and 0.87% respectively. Note the S&P touched its highest level since early February. The positive sentiment seems to have lingered, as futures tracking the S&P, Dow, and Nasdaq 100 are all pointing to a higher open today. Asia was a sea of green as well, with Japan’s Nikkei 225 and Topix surging by 1.81% and 1.19% correspondingly, buoyed by yen weakness as well. In Hong Kong, the Hang Seng rose by 0.22%. Europe looks set to follow suit, as futures suggest all major indices are due to open much higher.

COMMODITIES: Oil prices continued to struggle, remaining close to their lows for the week amid concerns of Libyan output returning to the market soon, as supply disruptions appear to have been resolved. WTI is up today, albeit by less than 0.05%, while Brent is down by 0.53%. In precious metals, gold is down marginally (-0.06%), currently trading near the $1,245 per ounce mark, not far above its lows for the year. Buyers remain in short supply, with a lack of any worrisome news on the geopolitical front combined with a broadly strong US dollar, curbing demand for the yellow metal.

Major movers: Markets cheer lack of escalation in trade standoff; yen retreat in full swing

Risk appetite remained firm on Thursday, with concerns regarding trade tensions taking a back seat as China refrained from retaliating to the $200bn tariffs the US threatened earlier in the week. Playing into the narrative that things are calming down, US Treasury Secretary Mnuchin told lawmakers in Congress yesterday that he is “available” for negotiations with China, reviving hopes that the situation may be finally resolved through a deal.

US stock markets closed notably higher, with the tech-heavy Nasdaq Composite reaching a fresh record high, while most Asian indices also advanced on Friday. Meanwhile, the Japanese yen, which has so far acted as a barometer for trade tensions, continued its recent plunge as investors rotated out of safer assets and into riskier ones. Dollar/yen touched a fresh six-month high of 112.75, with the yen also posting a two-month low against the euro. Focus now shifts to whether the two sides will head back to the negotiating table, something that seems probable considering recent remarks from Chinese officials suggesting they would be open to talks.

The dollar was marching higher early on Thursday but gave back most of its gains following the US CPI data for June, to close the day more or less unchanged against most of its major peers – though it advanced notably versus the yen. While both the headline and the core CPI rates were in line with annual estimates, it seems markets expected something better following the strong PPI prints earlier, hence triggering a knee-jerk reaction lower in the dollar on the news.

In the UK, the pound reacted little to the release of the detailed 100-page Brexit plan by Theresa May’s administration. As advertised, the plan seeks frictionless access to the single market for goods, but not for services; it repeatedly highlighted service firms would probably have less access to the EU market than they do now. All in all, this plan is unlikely to be accepted by the EU in its current form, which implies that further negotiations (and potentially concessions) may lie ahead. Pound/dollar is down by 0.3% today though, following some comments overnight from US President Trump that PM May’s latest Brexit plan “will probably kill” a future trade deal with the US.

Day ahead: University of Michigan consumer sentiment survey due; Trump’s UK visit also eyed

Friday’s calendar is rather light, with the most important release being the University of Michigan’s survey on US consumer sentiment. In the meantime, Trump’s visit in the UK will also be monitored for any market sensitive comments.

At 1230 GMT, data on June’s import and export prices will be made public out of the US, while the University of Michigan’s preliminary survey gauging consumer morale during July is due at 1400 GMT – the relevant index is anticipated to weaken, though not to a significant extent. Beyond the headline number out of the U of M’s survey, other information, such as the sub-indexes gauging inflation expectations, will also be attracting interest.

On the trade front, worries appear to have eased a bit after China did not opt to retaliate to threatened US tariff increases on its products. However, things remain fluid and a tit-for-tat response by China cannot be ruled out.

In terms of policymakers’ appearances, Bank of England Monetary Policy Committee member Jon Cunliffe will be giving a speech at 1100 GMT, while Atlanta Fed President Raphael Bostic (voting FOMC member in 2018) will be participating in a discussion at 1430 GMT. Meanwhile, US President Donald Trump is in the UK, where political uncertainty is on the rise on the back of disagreements within the Conservative party over Brexit. It is also noteworthy that Trump warned PM Theresa May that her Brexit proposal could “kill” any future trade deal with the US.

Also of interest, especially in light of ongoing NAFTA negotiations, is a visit to Mexico by US Secretary of State Mike Pompeo; he will be meeting officials, as well as president-elect Andres Manuel Lopez Obrador.

In equities, JPMorgan Chase, Citigroup, Well Fargo and PNC Financial Services Group are notable names releasing quarterly earnings today; their results will be made public before Wall Street’s opening bell.

In energy markets, the Baker Hughes count of US active oil rigs is due at 1700 GMT.

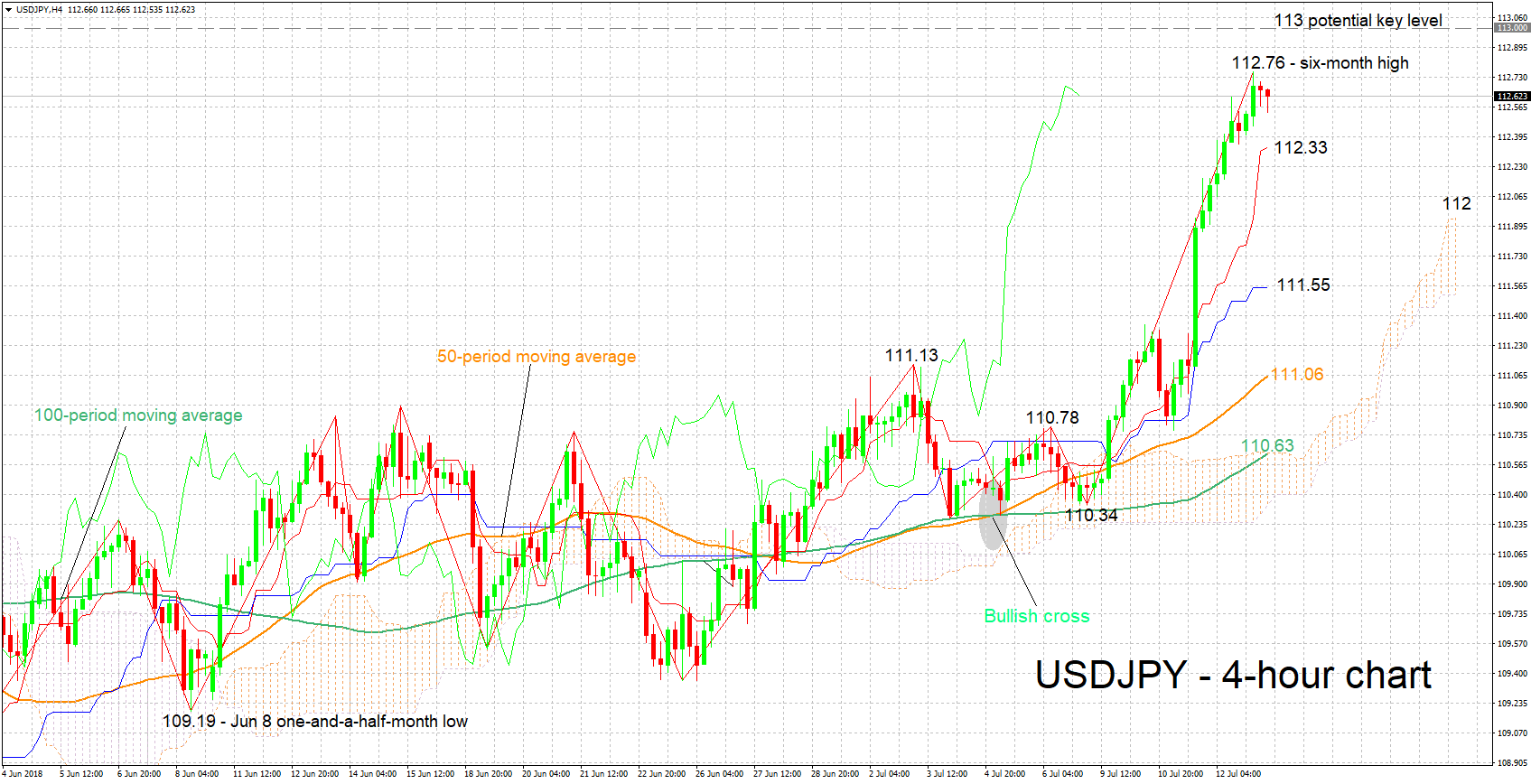

Technical Analysis: USDJPY touches 6-month high; looks overbought

USDJPY has risen to a six-month high of 112.76 earlier on Friday, while it is currently trading not far below this zenith. The positively aligned Tenkan- and Kijun-sen lines are projecting a bullish picture in the short-term, though the flattening Kijun-sen may constitute an early sign of easing positive momentum. Moreover, the Chikou Span is signaling an overbought market, the implication being that a near-term reversal is not to be ruled out.

Abating risks over global trade may push the pair higher, with resistance potentially taking place around the 113 round figure.

On the downside and in case of rising trade tensions that divert safe-haven flows into the yen, support could come around the current level of the Tenkan-sen at 112.33, before the attention next turns to the 112 handle.

Some movement in USDJPY may occur upon the release of the University of Michigan’s survey as well.

{kind=link}