Here are the latest developments in global markets:

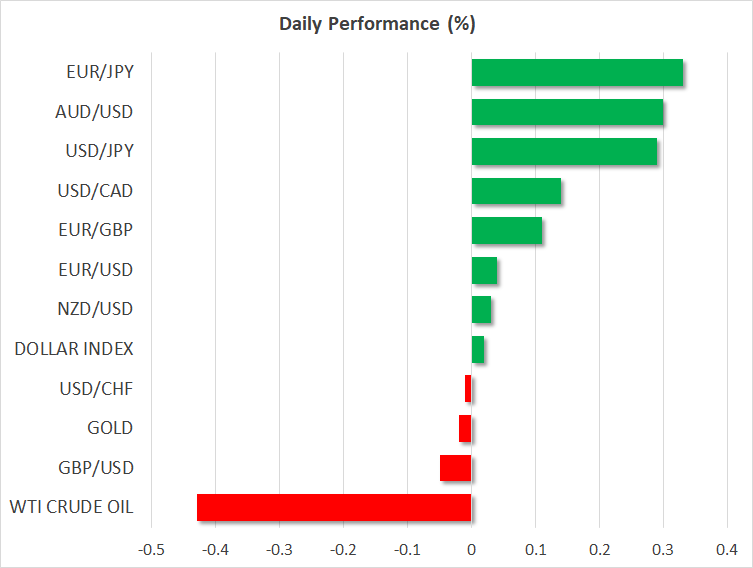

FOREX: The US dollar index is practically unchanged on Tuesday, after it posted considerable losses in the previous session. The yen, meanwhile, fell across the board after the BoJ delivered only minor tweaks to its policy framework, disappointing those looking for a major hawkish turn (see below). The loonie also had a rather volatile time, amid conflicting NAFTA headlines.

STOCKS: Wall Street closed lower yesterday, as a notable selloff in tech stocks dragged the broader equity indices down. The tech-heavy Nasdaq Composite (-1.39%) declined for the third straight session, while the S&P 500 (-0.58%) and the Dow Jones (-0.57%) did not escape unscathed either. Some of the biggest underperformers were Twitter (-8.03%), Netflix (-5.70%), and Facebook (-2.19%). That said, futures point to a slightly higher open for the S&P, Dow, and Nasdaq 100 today. Asia was mixed on Tuesday, with Japan’s Topix falling by 0.84%, while the Nikkei 225 rose a marginal 0.039%. The BoJ announced that it will increase the ratio of ETFs it purchases linked to the Topix moving forward. In Hong Kong, the Hang Seng dropped 0.53%. In Europe, futures were pointing to a mixed open today.

COMMODITIES: Oil prices rose on Monday, as the US dollar – in which the precious liquid is denominated – declined. A weaker greenback increases the appeal of oil for investors using foreign currencies. That said, both WTI and Brent are lower by 0.43% and 0.47% respectively on Tuesday, giving back some of their gains following a Reuters survey suggesting OPEC raised its production by around 70,000 barrels per day in July. In precious metals, gold continues to show “no signs of life”, with price action being contained in an extremely narrow range over the past few days. The dollar-denominated metal is currently hovering around $1,220 per ounce, flirting with its lows for the year at $1,211, and unable to draw any support from the recent pullback in the greenback.

Major movers: Yen drops after “no smoking gun” from BoJ; euro regains ground

The Bank of Japan (BoJ) kept its policy rate unchanged at -0.1% earlier today, while it also made some tweaks to its policy, albeit relatively minor ones. It decided to allow the yields on longer-term Japanese Government Bonds (JGBs) more flexibility to move to the upside or the downside, but that it would keep the yield target unchanged near zero percent. In other words, it will widen the range around which the 10-year JGB yield can fluctuate, but the center of that range would remain unchanged. It also introduced forward guidance stating that interest rates will remain at very low levels for an extended period of time. Inflation forecasts were revised lower.

Overall, the BoJ made only minor adjustments aimed at enhancing its policy flexibility, and was not perceived as taking its foot off the accelerator – as had been speculated. Hence, yields on 10-year JGBs dropped immediately on the decision while the yen retreated, giving back some of the gains it had posted in recent days on speculation for a hawkish twist. Moving forward, although there remain some key questions to be answered – such as how high the Bank will allow yields to go before intervening – the bigger narrative of monetary policy divergence between Japan and other economies remains largely intact. This implies that interest rate differentials could continue to work against the yen moving forward.

The euro, meanwhile, advanced across the board yesterday, even despite preliminary CPIs out of Germany being a touch softer than expected. A fresh slew of Eurozone data today – including the bloc’s preliminary inflation figures – will likely guide price action in euro pairs.

Elsewhere, the Canadian dollar had a volatile ride. The currency initially surged on Monday after US Commerce Secretary Ross said that the trade deal closest to its completion is NAFTA. The move was short-lived though, with the loonie giving back all its Ross-related gains to trade even lower following reports overnight that US officials rejected Canada’s bid to take part in NAFTA talks between the US and Mexico this week.

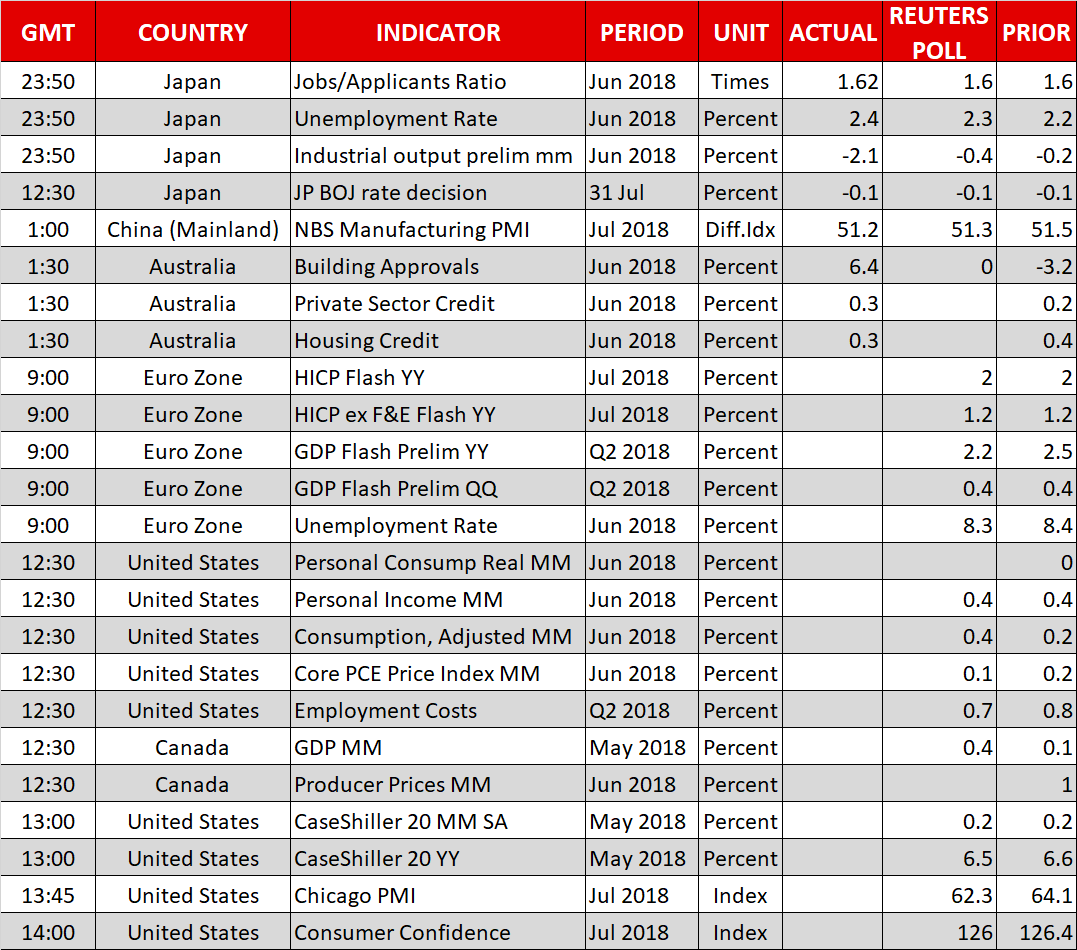

Day ahead: Eurozone inflation and GDP on the horizon; US core PCE price index and Canadian GDP also out

Eurozone flash inflation figures for July, as well as preliminary Q2 GDP estimates and data on unemployment out of the bloc are on the agenda on Tuesday. Meanwhile, the core PCE price index and numbers on personal income & consumption are due out of the US, while Canada will be seeing the release of monthly GDP data.

Projections are pointing to mostly unchanged inflationary pressures and economic activity in the eurozone during July and Q2 respectively. Specifically, the Harmonised Index of Consumer Prices (HICP), that uses a common methodology across EU countries, is anticipated to grow by 2.0% in yearly terms, the same as in June. The core HICP rate that excludes food and energy items is forecast to expand by 1.2%, again the same as in June.

Turning to eurozone GDP growth, it’s rate of expansion is expected to match Q1’s 0.4% in quarterly terms, something which would drag the annual pace of growth to 2.2%, from 2.5% previously. Lastly, the bloc’s unemployment rate for June is also due out and is projected to tick down to its lowest since late 2008 of 8.3%, from 8.4% in May. All numbers are due at 0900 GMT, while it is of note that Germany, the eurozone’s largest economy, will be seeing the release of unemployment data for July at 0755 GMT.

Out of the US, figures on personal income are expected to reflect a growth rate of 0.4% m/m in June, the same as in May. In the meantime, consumption is also expected to expand by 0.4% m/m, accelerating from the 0.2% rate seen in May. Most interest though might fall on the core PCE price index, this being the Fed’s preferred inflation gauge. The indicator of price pressures is anticipated to ease to 0.1% on a monthly basis in June, from 0.2% in May, though still post an annual growth rate of 2.0% after hitting the milestone – the US central bank’s inflation target – in May for the first time in six years. A better-than-forecasted inflation print can more conclusively put on the table two more rate hikes by the Fed in 2018, consequently boosting the greenback. The figures will be made public at 1230 GMT, alongside the reading on Q2’s employment costs.

Other US releases are May’s CaseShiller indices gauging house prices (1300 GMT), July’s Chicago PMI (1345 GMT) and the Conference Board’s consumer confidence index for the same month (1400 GMT) – the relevant index is expected at 126.0, only slightly weaker compared to June’s 126.4.

Canadian GDP data will be hitting the markets at 1230 GMT and are expected to show activity accelerating by 0.4% m/m in May, from 0.1% in April. June’s print on producer prices is due at the same time.

In equities, tech giant Apple will be releasing quarterly earnings after the US market close on Tuesday.

In energy markets, weekly API data on US crude stocks are due at 2030 GMT.

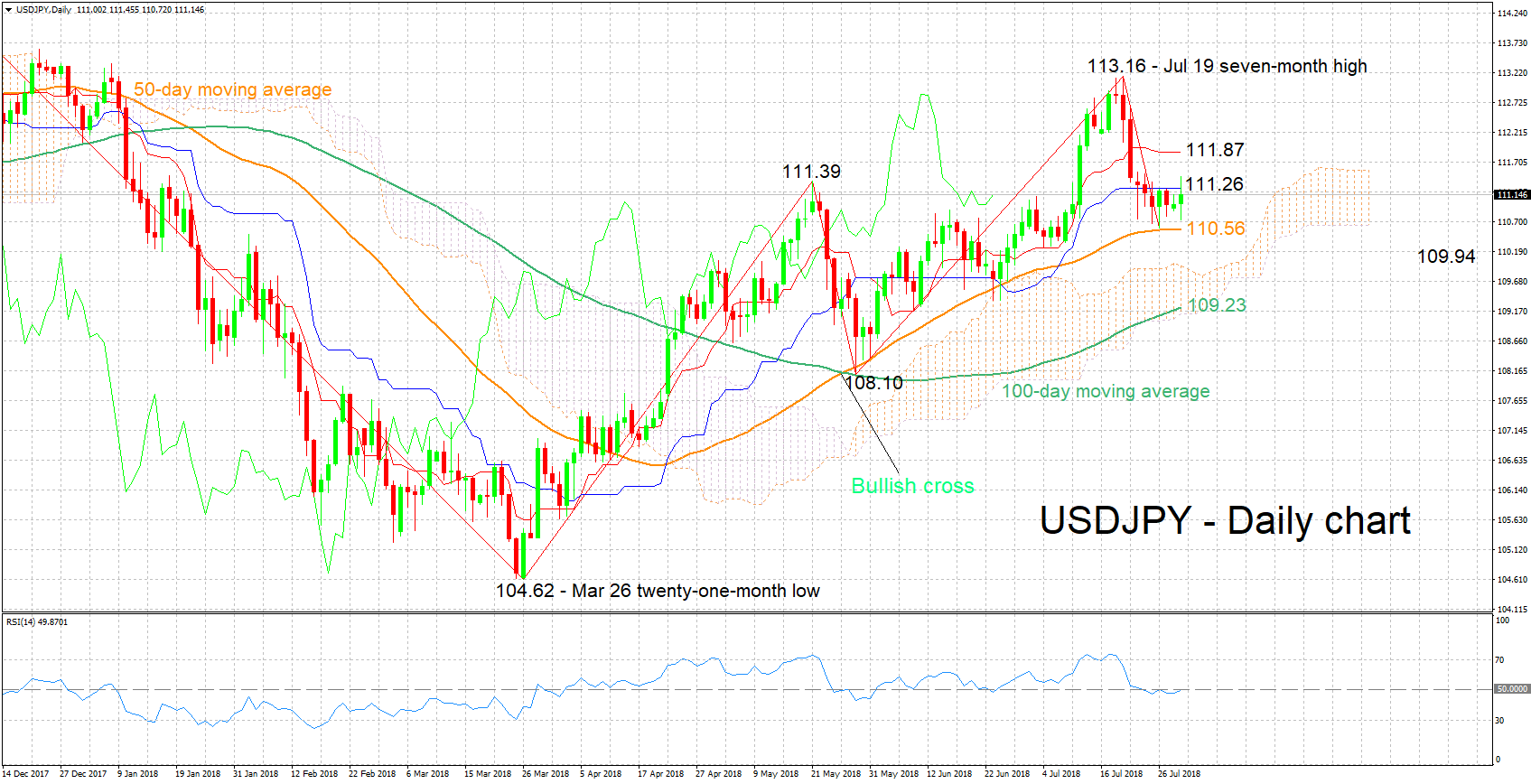

Technical Analysis: USDJPY predominantly neutral in the short-term

USDJPY has been largely moving sideways in recent days. The Tenkan- and the Kijun-sen lines are positively aligned, though they’ve both flatlined, on balance projecting a neutral picture in the short-term. This is also supported by the RSI, which is moving sideways on its 50 neutral level.

Stronger-than-anticipated core PCE price data are likely to boost the pair. Immediate resistance seems to be taking place around the current level of the Kijun-sen at 111.26, with the focus in case of an upside break falling to the region around the Tenkan-sen at 111.87 which also encapsulates the 112 round figure.

A weaker-than-expected inflation reading on the other hand, is likely to weigh on USDJPY. Given a fall below the 111 handle, support may come around the current level of the 50-day moving average line at 110.56, and then from the area around the Ichimoku cloud top at 109.94, including the 110 mark.

{kind=link}