Here the latest developments in global markets:

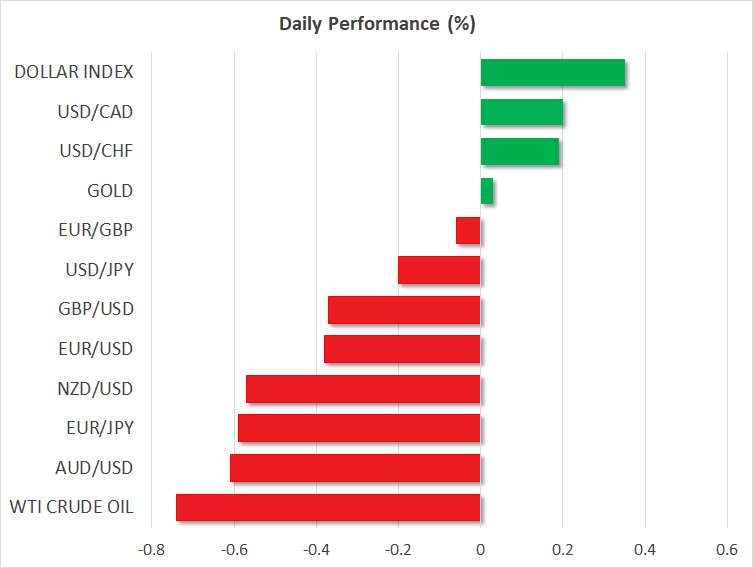

FOREX: The US dollar index, which measures the greenback against a basket of six currencies, advanced by 0.39% and touched a two-week high near 95.00 on Thursday. Dollar/yen was weaker on Thursday at 111.49 (-0.20%) despite the Fed reiterating that the US economic growth has been rising strongly and the job market has continued to strengthen. Yesterday the 10-year Japanese government bond yields reached a fresh one-and-a-half-year high, following the Bank of Japan’s decision to allow more flexibility in yields movements earlier in the week. Euro/dollar and pound/dollar declined by 0.41% and 0.39% respectively, despite that the UK’s construction PMI ticked surprisingly up to 55.8 in July from 53.1 before. The spotlight event of the day is the Bank of England’s monetary policy decision which is highly expected to deliver the second rate hike since the global financial crisis. In the antipodean sphere, aussie/dollar fell by 0.62% to 0.7357 and kiwi/dollar dropped by 0.57% to 0.6749. Meanwhile, dollar/loonie erased some losses of the previous day, adding 0.21%. Dollar/lira jumped to a record high once again, rising by 1.86% as the US imposed sanctions on its NATO ally over the imprisonment of an American pastor. The offshore yuan retreated to a 14-month low on the back of growing trade tensions between the US and China.

STOCKS: European equities edged aggressively lower on Thursday with significant losses. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 declined by 0.86% and 1.31% respectively at 1030 GMT and are set to complete the second red day in a row. The German DAX 30 dived by 1.77%, the French CAC 40 tumbled by 0.87%, while the Italian FTSE MIB dipped by 0.87%. UK’s FTSE saw a strong sell-off as well, retreating by 0.87%. Futures tracking US stock indices were all in the red, pointing to a negative open after the FOMC monetary policy decision.

COMMODITIES: Oil prices moved lower today after a surprise gain in U.S. crude inventories exacerbated supply concerns. WTI crude stood near a six-week low of $67.13/barrel, losing 0.78% from its performance, while Brent fell by 0.36% to $72.13. In precious metals, gold was higher by 0.07% at $1215.30/ounce.

Day ahead: Bank England rate announcement in the center stage with trade developments eyed

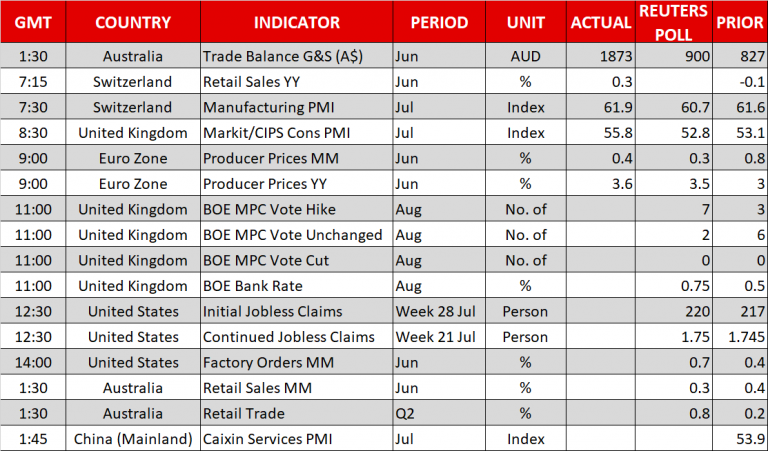

The Bank of England (BoE) will be deciding on monetary policy later today. Markets are expecting the Bank to raise benchmark rates by a quarter percentage point to 0.75% (1100 GMT) with the probability for such an action standing at around 91% according to UK OIS. Since a rate increase has been already mostly priced in, the focus will turn to the voting structure, with investors eagerly awaiting to see whether continuing Brexit and trade uncertainties, as well as some recent weakness in British wage growth, is pushing some policymakers to the dovish side in terms of the rate outlook.

In the previous meeting, six policymakers backed no change in interest rates, while the remaining three voted in favor of a rate rise. Expectations now are for a 7-2 rate hike vote and should this come surprisingly different, the pound could see some fluctuation. In other words, in case a larger number of MPC policymakers support that rates should remain steady, the pound is likely to move south and vice versa. Still, a “dovish” rate hike is not unlikely as the lack of clarity on the Brexit front and growing whispers of a no-Brexit deal not long before Britain’s exit from the EU bloc could turn policymakers cautious on future rate increases. Moreover, risks around the US trade policy which threatens the state of global trade could further complicate matters for policymakers. Commentary on Brexit and trade topics – especially the former – are expected by the BoE chief, Mark Carney, who will be holding a press conference at 1130 GMT. Investors will be also be carefully monitoring the Bank’s inflation forecast report delivered today alongside the rate announcement.

Meanwhile in the US, the economic calendar will feature initial jobless claims for the week ending July 28 at 1230 GMT and June’s factory goods orders at 1400 GMT. The numbers are expected to show that initial jobless claims have increased to 220,000 in the aforementioned period compared to 217,000 seen in the previously tracked week, while new orders by manufacturers are projected to grow by 0.7% m/m, above May’s 0.4%.

Updates on the US-China trade dispute, though, could be of greater importance to the dollar as tensions are not near to ease yet, with sources stating that the US president demands a 25% import tariff on $200 billion Chinese goods compared to 10% previously proposed. While the headlines weighed in Chinese financial markets, the Chinese deputy director of the Foreign Ministry Information Department said in return that “unilateral threats and pressure from the US will only backfire”, adding that door for dialogue is open from China’s side.

The NAFTA story will come under the spotlight too as Mexican negotiators are heading to Washington this week to restart talks with their US counterparts amid optimism that both countries could reach an agreement on the auto part which have been dragging on talks so far.

Elsewhere, retail sales for the month of June will be closely reviewed in Australia at 0130 GMT on Friday with forecasts supporting a stronger growth of 0.8% q/q in the second quarter, compared to 0.2% rise seen previously. Month-on-month, however, the measure is said to come slightly weaker, inching down by 0.1 percentage points to 0.3%. A beat in data could help the aussie, which is currently trading at 2-week lows versus the greenback, to pare losses. Chinese Caixin services PMI delivered a few minutes later at 0145 GMT could be supportive as well if the numbers prove encouraging.